David Bassanese

7 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the player below:

Global week in review: inching to a deal

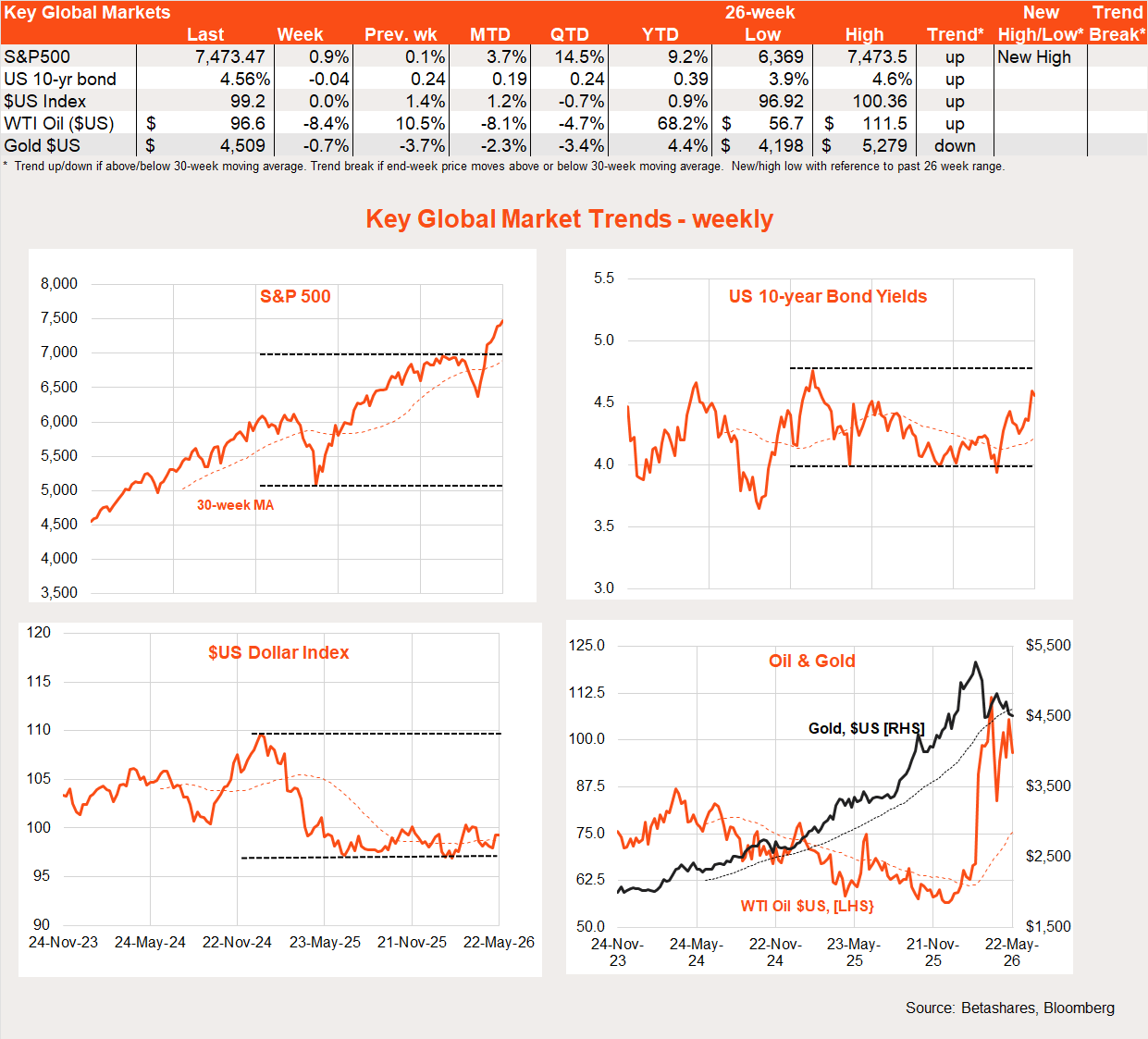

US equities continued their move into record territory last week with on-again off-again reports of an imminent US-Iran peace deal. At the time of writing late Monday morning, reports suggest both sides were still inching toward a deal.

The actual details of the deal remain to be seen. But whether US President Trump strikes a deal better than the one he tore up in 2018 does not seem to bother markets too much in the short-term – the focus is simply on ending hostilities and re-opening the Strait of Hormuz.

While Trump may say he’s in no hurry to strike a deal, the economic reality suggests otherwise. As I’ve noted here regularly, we’re likely only weeks away from the ongoing closure of the Strait leading to supply shortages and much higher oil prices. That would be ugly for both bond and equity markets.

Indeed, in other news last week, minutes of the latest Fed meeting suggested more voting members being open to the idea of raising rates “if inflation were to continue to run persistently above 2 per cent”. Most members seemed to feel economic growth and the labour market were still holding up, and so were mostly concerned about continued above-target inflation.

Of note also in markets in recent weeks has been a sharp rise in long-term bond yields, along with the moderate rebound in oil prices. US 10-year yields rose 0.23% to 4.6% two weeks ago and peaked at 4.67% last Tuesday – the day Brent crude oil futures hit US $108/barrel. But by Friday, peace-talk hopes had pushed oil futures back to US $95 and US 10-year yields back to 4.56%.

Global week ahead: Iran and PCED

As has been the case for several months, the market’s focus will remain on progress in US-Iran peace talks.

The Fed’s preferred inflation measure – the consumption deflator or PCED – is also released mid-week, with expectations that annual core inflation will inch up to 3.3% from 3.2%. That’s still well above the Fed’s 2% target.

Global equity trends: non-US bounce back

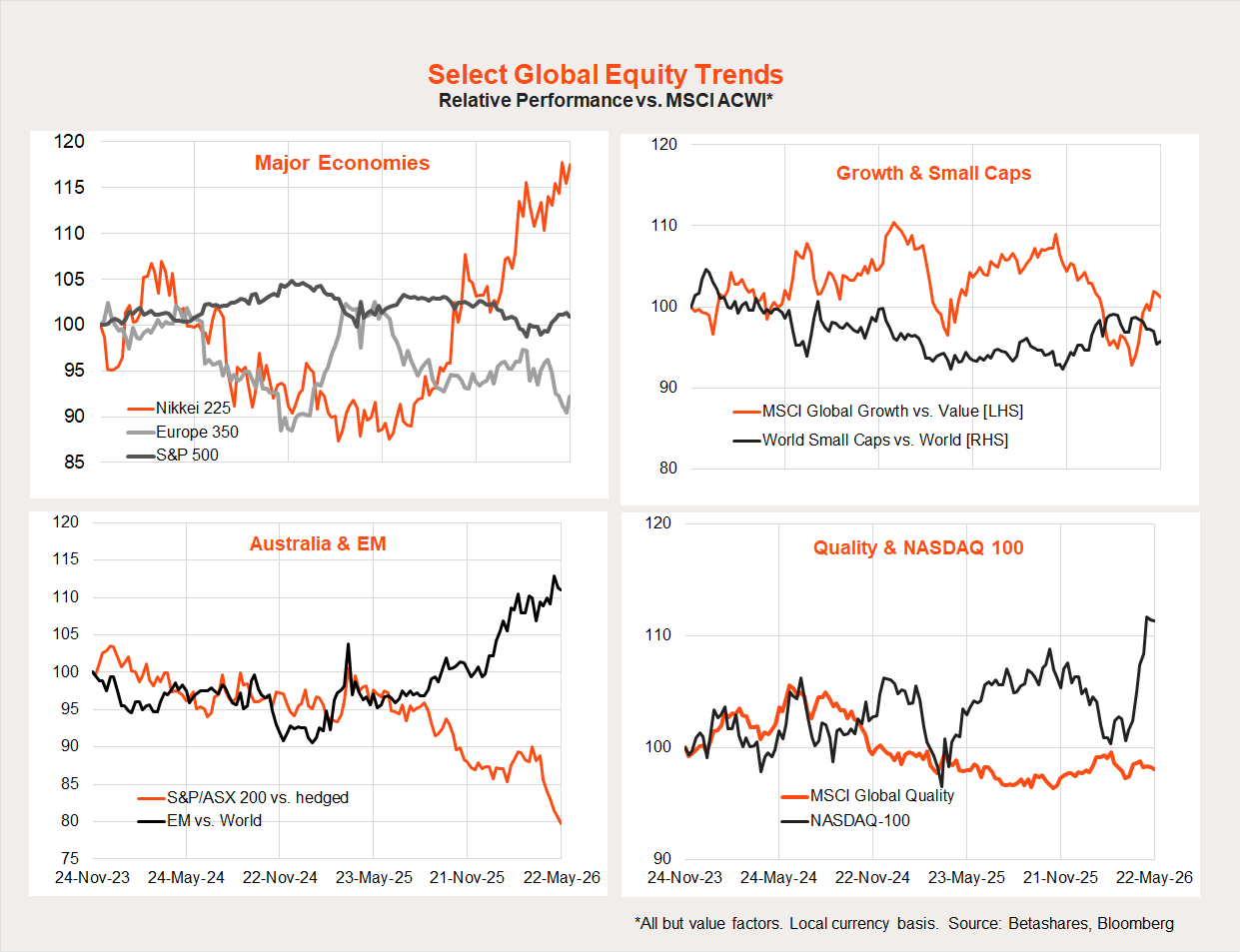

Non-US markets enjoyed the biggest gains last week, with both Europe and Japan up 3.1%. Among sectors, energy and materials fared worst, reflecting an easing in oil prices. The Nasdaq-100 gained a reasonable 1.2% while the downtrodden S&P/ASX 200 eked out a 0.4% gain.

All up, the US, Japan and emerging markets continue to do best in the rebound so far, whereas Europe, Australia and small caps have not. The Nasdaq-100 has continued to shoot the lights out.

Australia review: Sleepwalking into recession?

Local stocks rode the coattails of global optimism last week even though local news is collectively as depressing as I’ve seen it in a long while. I’ve just lost confidence in the ability of this economy to do much anytime soon. Most of this is policy driven – with a hawkish RBA and growth-zapping Federal Budget.

The blowback from the Federal Government remained intense last week, with a number of potential “unintended consequences” emerging in light of the Government’s 11th hour decision to extend changes in capital gains taxation from residential property to all assets.

The Government has signalled that it may tweak its policy to avoid an effective “death tax” arising from plans to tax certain trusts at a minimum 30%. There are also signs it will carve out the technology/start-up sector from the onerous capital gains changes.

Yet this still leaves the reality that Australia will have one of the highest capital gains taxes on high-growth investments in the world – even while surrounded by countries such as New Zealand and Singapore that don’t tax capital gains at all! Plans to only carve out the tech sector will also enrage every small business start-up around the country, who still face the prospect of losing up to 47% in tax on any business sale.

But yet another potential “unintended consequence” emerged last week, namely that the way in which losses on share trading are treated will greatly increase the effective capital gains tax on portfolios of individual shares. Of course, it would be a big win for pooled investments such as ETFs (which can more tax effectively offset share trading losses against gains) but the policy seems so devastating and nonsensical that I can’t believe it won’t also be tweaked.

It’s sad to say, but it’s been many years since I’ve seen a bunch of Budget proposals so ill considered. The Budget’s proposals on residential property have faced the least criticism – but, even if accepted, they’re likely to see falling property prices for a time (and a dent to household wealth) as properties get cheaper for first-home buyers to afford. But rents may also rise as investors desert the market.

Given the weakening property market, rising rents, the RBA’s ongoing tightening bias and the confidence destroying non-property changes in the Federal Budget, recession risks have no doubt increased. March quarter GDP growth was already likely to be weak, and a negative Q2 outcome is now at least a 50-50 chance.

The big worry is a collapse in consumer confidence takes down consumer spending, which is 50% of the economy. The Westpac measure of consumer confidence did bounce 3.5% in May – likely thanks to easing petrol prices – but it’s still wallowing at very low levels.

Another risk is a fall in business confidence and hiring intentions. Pre-budget, hiring indicators were weakening but still at reasonable levels, and it will be a nervous few weeks and months to see if this remains the case. Although likely distorted by seasonal quirks around Easter, last week’s April employment report revealed a 19K drop in employment and rise in the unemployment rate from 4.3% to 4.5%.

One bright spot may be a US-Iran peace deal – which could lower oil prices. But if oil prices instead push higher in coming months if no deal is struck, a local recession could become the base case.

Local equity market trends: Technology/small caps bottoming out?

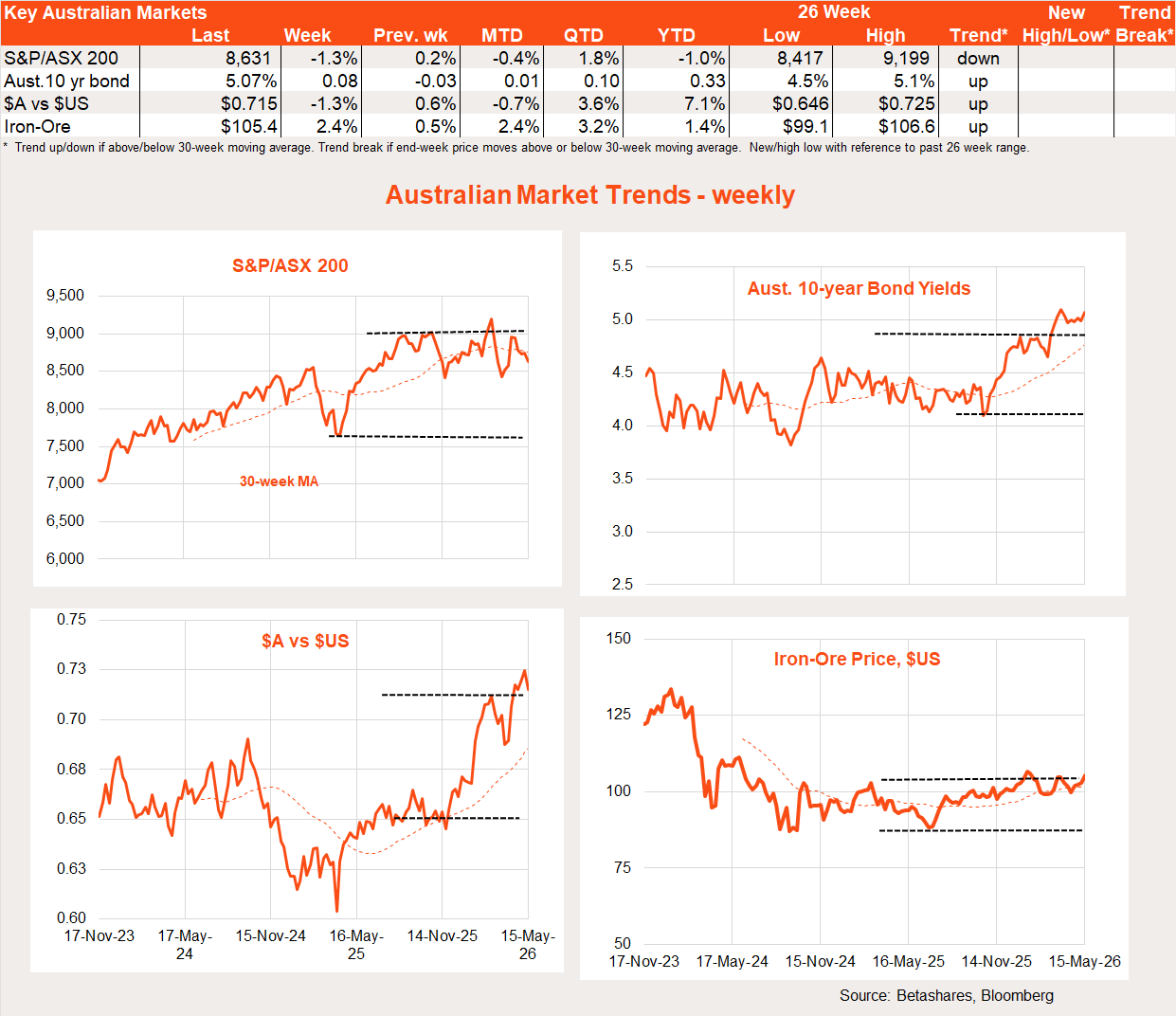

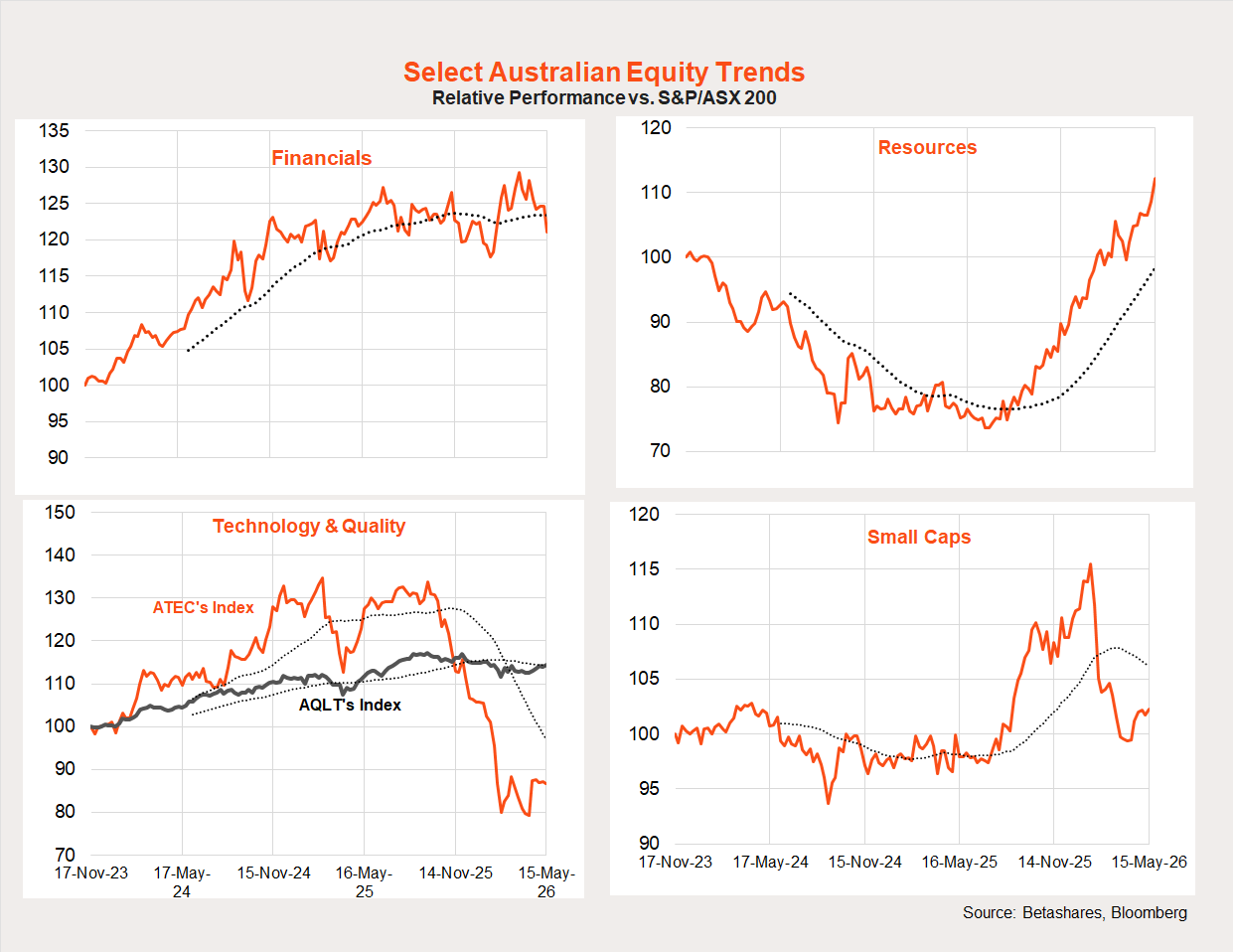

Energy, financials and consumer staples held up best in the local market last week but otherwise it was a sea of red.

Among major sectors, the trend remains of resources beating financials. After a significant sell-off over earlier months, the relative performance of high-beta technology and small cap stocks still appears to be bottoming out, though it has slipped back a little in recent weeks. The RBA/Budget double act is likely to see stocks exposed to the local economy struggle relative to globally exposed resource stocks.

Australia week ahead: April CPI

The April monthly CPI report will be the major local economic highlight this week. While easing petrol prices – thanks to the reduced fuel excise – will take the sting out of the headline inflation result, the indirect effect of higher energy costs is likely to be felt across travel and even groceries.

Headline inflation is expected to rise 0.5%, with annual inflation easing from 4.6% to 4.4%. Trimmed mean inflation is expected to rise 0.3% in the month, with annual inflation edging up to 3.3% from 3.2%.

We also get the early building blocks to Q1 GDP, with likely firm readings on private capital spending and building construction. As noted above, the risk for Q1 GDP is consumer related.

Have a great week!