Chamath De Silva

6 minutes reading time

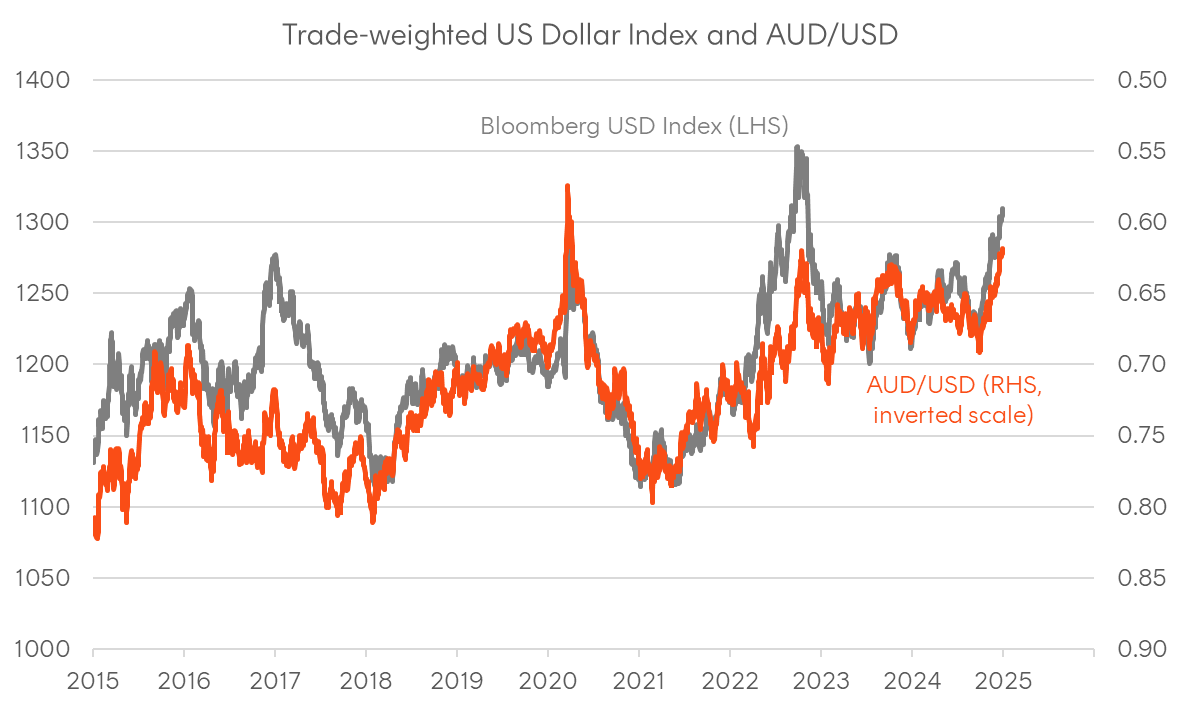

One of the strongest indicators of US exceptionalism has been evident in FX markets, where the broad US dollar index surged to its highest level on a trade weighted basis since 2022, gaining 8% in 2024.

The resilience has been surprising, given it coincided with the start of a cutting cycle from the Fed, and the index is back around levels last seen when the Fed was raising rates. Because of the broad USD strength and weakness in selected industrial commodities, the AUD/USD rate tumbled in the latter half of the year to fresh post-pandemic lows.

Even at the start of 2024, the USD was considered overvalued based on most fundamental currency metrics, like purchasing power parity. The greenback’s strength in the second half of the year was underpinned by the US economy’s continued outperformance relative to other major economies, expectations of tariffs from the new US administration, as well as widening nominal and real interest rate differentials against the euro, yen and Chinese renminbi.

In contrast, the economic malaise in China has reinforced the US’s role as the primary engine of global growth, which weighed on commodity sensitive currencies such as the Australian dollar. The rally in the US dollar has also been amplified by the US-centric nature of the bull market in technology stocks and AI-related themes, attracting significant global financial flows into the US, a reprisal of the “new vs old economy” narrative from 25 years ago.

Source: Bloomberg. As at 31 December 2024.

What’s next for the dollar?

Looking ahead, the trade policies of the new Trump administration will add a layer of complexity to the US dollar outlook. Objectives such as reducing the trade deficit and promoting onshoring may conflict with sustained dollar strength.

In the lead up to the inauguration, expectations of broad-based tariffs supported the US dollar. Since the inauguration, the imposition of new tariffs on China, the announcement and then delay of tariffs on Mexico and Canada, and the unveiling of separate tariffs on steel and aluminium imports have injected fresh uncertainty to currency markets. However, further dollar appreciation and FX volatility could weigh on corporate earnings from US multinationals, as many derive a significant portion of their revenues from abroad. While the new Treasury Secretary has declared the US won’t be shifting from the long-standing “strong dollar” policy, encouragement of key trading partners like the euro area and Japan to strengthen their currencies to make the US dollar more competitive should not come as a surprise.

Fundamentally, the USD remains overvalued, with the real effective exchange rate around its highest levels (i.e. least competitive) over the past 30 years, and a softening of the US economy, the re-emergence of rate cut expectations, or a shift in government policy could produce a dramatic mean reversion.

Historical parallels can also provide further insight. During President Trump’s first term, the dollar initially rallied into the inauguration, only to reverse sharply during 2017. Additionally, we can’t ignore the historical precedent set by the Plaza Accord of 1985, where global leaders convened to engineer a weaker USD and stronger Japanese yen following a period of large US trade deficits against the main export economies at the time (Japan and West Germany). Incidentally, this meeting took place at the Plaza Hotel in New York, which Donald Trump would famously purchase three years later.

A significant reversal in the USD would carry profound investment implications, particularly for global equities, where around 75% of the developed market benchmark is comprised of US stocks – up from around 60% during the pre-pandemic period and 50% immediately following the global financial crisis.

Source: Citi, real effective exchange rate against trade weighted basket of currencies; 1 January 1994 to 10 February 2025. For illustrative purposes.

Source: Bloomberg. 31 December 1979 to 31 December 1989. For illustrative purposes only.

Is it time to currency hedge portfolios?

The weakness in the AUD/USD exchange rate has supported unhedged global share market returns for over a decade. However, with the pair at the lower end of the historical range, investors are naturally revisiting the question of FX hedging. While the AUD has its own unique factors – and the RBA is likely to join the global easing cycle soon – broader USD dynamics will likely remain the primary driver of the direction in the AUD/USD exchange rate over the remainder of the year. As a result, considering FX hedging and raising FX hedging ratios may be a prudent move. With the combination of potential policy shifts from the new administration, a fundamental overvaluation of the USD and a Fed that is likely to maintain an easing bias, “King Dollar’s” reign may not be as unassailable as it currently appears.

Currency hedged ETFs seek to substantially offset a fund’s exposure to movements in the value of foreign currency. Historically, we have observed an exchange rate below 65 US cents being a key level for investors considering whether to start investing into currency hedged ETFs.

With the Australian dollar currently trading close around 63 US cents a normalisation to the long-term average of 75 US cents would see investors in unhedged US dollar exposures suffer substantial losses due to currency movements.

Betashares offers a range of currency hedged international ETFs including on the HNDQ Nasdaq 100 Currency Hedged ETF , HQUS S&P 500 Equal Weight Currency Hedged ETF , and HQLT Global Quality Leaders Currency Hedged ETF .

Betashares has also adopted TOFA treatment for efficient tax outcomes from hedging in these ETFs. Learn more about TOFA here.

You can find more information on currency hedging and Betashares’ currency hedged funds, including sector and regional funds, here.

This short video explains how currency hedging works.

There are risks associated with an investment in each Betashares Fund. Investment value can go up and down. An investment in any Fund should only be made after considering your client’s particular circumstances, including their tolerance for risk. For more information on the risks and other features of a Fund, please see the relevant Product Disclosure Statement and Target Market Determination, available at www.betashares.com.au.