James Fleiter

8 minutes reading time

- Private assets

- Private credit

This information is for the use of licensed financial advisers and other wholesale clients only.

Recent months have provided the first meaningful liquidity test for the growing universe of evergreen private market funds. Despite the tone of some media coverage, the evidence we’ve seen so far suggests these structures are functioning largely as designed, with investors receiving the liquidity that the funds have committed to provide.

What we believe this episode highlights is not only a test of the structures themselves, but also of investor knowledge of the asset class. These semi-liquid private asset funds differ materially from traditional funds that hold publicly traded securities, and understanding these differences is essential for advisers communicating with clients.

Liquidity and the structure of private markets

A useful starting point is a simple principle: fund liquidity ultimately comes from the liquidity of the underlying assets.

Public market securities trade continuously on exchanges, allowing funds that hold them to offer daily subscriptions and redemptions. Private market investments operate differently. Direct loans to companies, for example, are negotiated privately and typically held over time rather than traded actively.

Because these assets cannot be sold instantaneously without affecting price, private market vehicles provide periodic rather than daily liquidity.

This reflects a broader principle of financial markets: liquidity and return are closely linked. Investments that offer immediate liquidity often provide lower expected returns, while assets requiring longer holding periods have historically commanded an illiquidity premium, reflecting the additional compensation investors demand for reduced liquidity.

Private credit is often cited as an example of this trade‑off.

How liquidity is structured in evergreen private credit funds

Evergreen private market funds were designed to broaden access to these hard to access investments while respecting the illiquid nature of the underlying assets.

Unlike traditional closed‑end funds, which lock capital up for many years, evergreen funds allow investors to subscribe and redeem capital on a regular schedule. Because the underlying assets remain illiquid, these funds operate with structured redemption programs.

Across the industry, whether in Australian private credit, U.S. private credit, or other private market strategies, each fund establishes its own liquidity framework designed to balance investor access to capital with the long‑term nature of the underlying investments.

Redemption windows typically occur monthly or quarterly, and investors can redeem up to a specified percentage of the fund’s net asset value during each period, commonly between 2% and 10% of NAV.

If redemption requests exceed the available capacity in a given period, they are typically prorated. For example, if a fund offers 5% quarterly liquidity but receives redemption requests equal to 6% of the fund, each investor would receive approximately five sixths of their requested amount in that redemption window. This is what occurred in Q1 2026 with most of the markets largest, and most well regarded funds seeing elevated redemption requests. Pleasingly all, to our knowledge at time of writing, fund managers have acted in accordance with their stated policies and been able to meet their scheduled liquidity obligations despite the media narrative to the contrary.

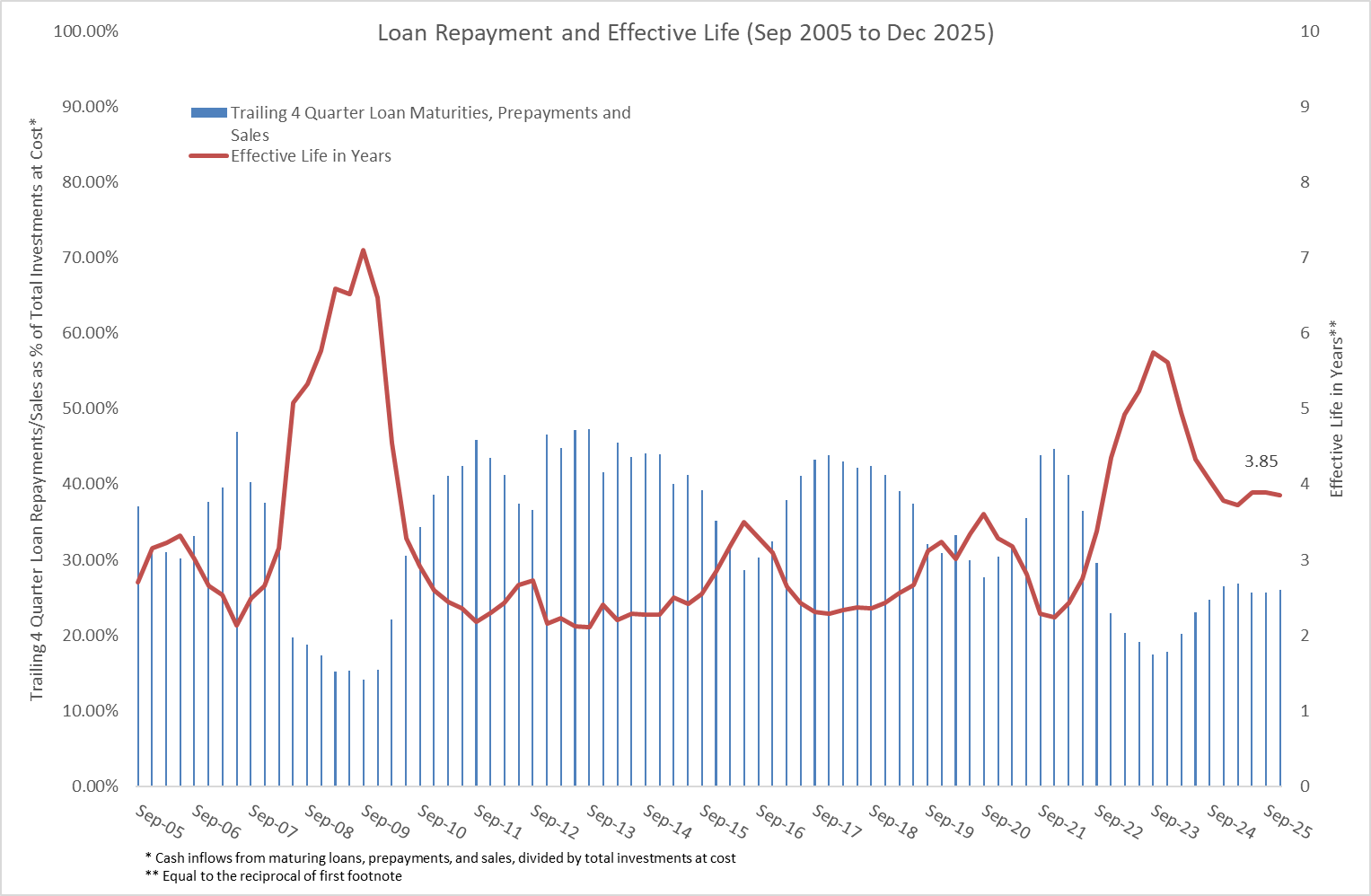

Underlying Asset Class Liquidity Profile

Importantly, liquidity in private credit portfolios does not rely solely on selling assets. Direct lending, the largest and most tenured sub-asset class within private credit, portfolios typically generate ongoing cash flows through loan amortisation, interest payments, refinancings and repayments as borrowers refinance or repay debt. ³

In fact, there are 20 years of historical data that help us understand the effective life of direct loans, defined as the weighted average period over which principal remains outstanding, reflecting the timing of repayments rather than the stated maturity. As of December 31 2025, the effective loan life equalled 3.85 years, down significantly from 4.36 two years ago, but still elevated relative to the 3.28 historical average. Said another way, history indicates 30.5% portfolio turnover each year.

Source: Cliffwater Direct Lending Index 31/12/2025.

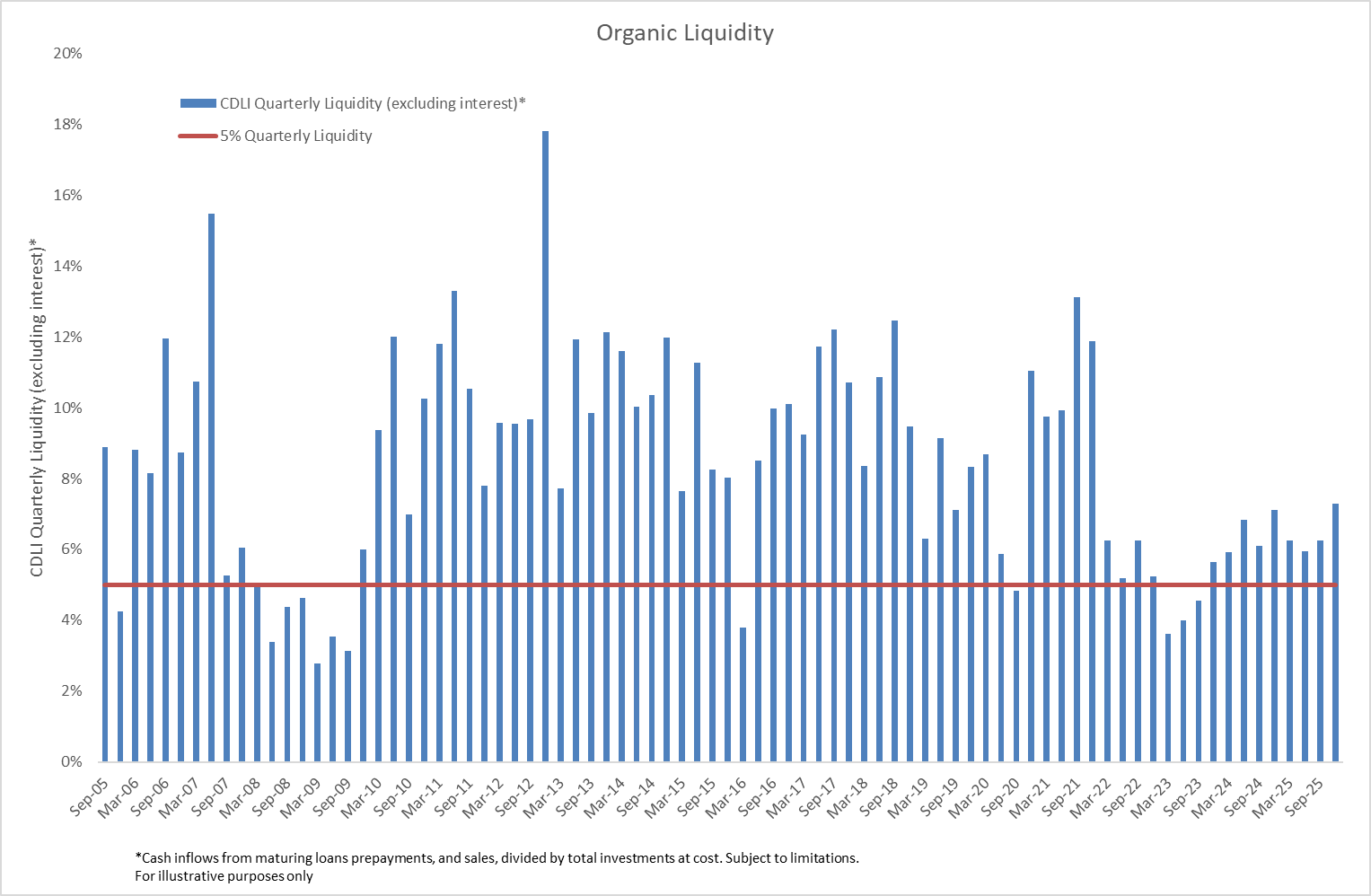

When looked at on a quarterly basis, this explains why the historical baseline for redemptions limits set by private credit funds is 5% per quarter, as this aligns very closely with the ‘organic’ liquidity of the asset class. Some fund managers, however, do in fact offer more than 5% per quarter, although there is no free lunch in private assets. The more liquidity they offer investors the less organic that liquidity can become, which can often come with its own set of trade offs.

Source: Cliffwater Direct Lending Index 31/12/2025.

Importantly, this organic liquidity is why private credit is, amongst the other main private asset classes like Private Equity, Real Estate and Infrastructure, the most well suited to evergreen structures given its natural liquidity. It is the ‘most liquid’, of the ‘illiquids’.

Why redemption requests have increased in private credit

During the fourth quarter of 2025 and first quarter of 2026, redemption requests across parts of the private credit market have increased following negative media coverage around credit conditions.

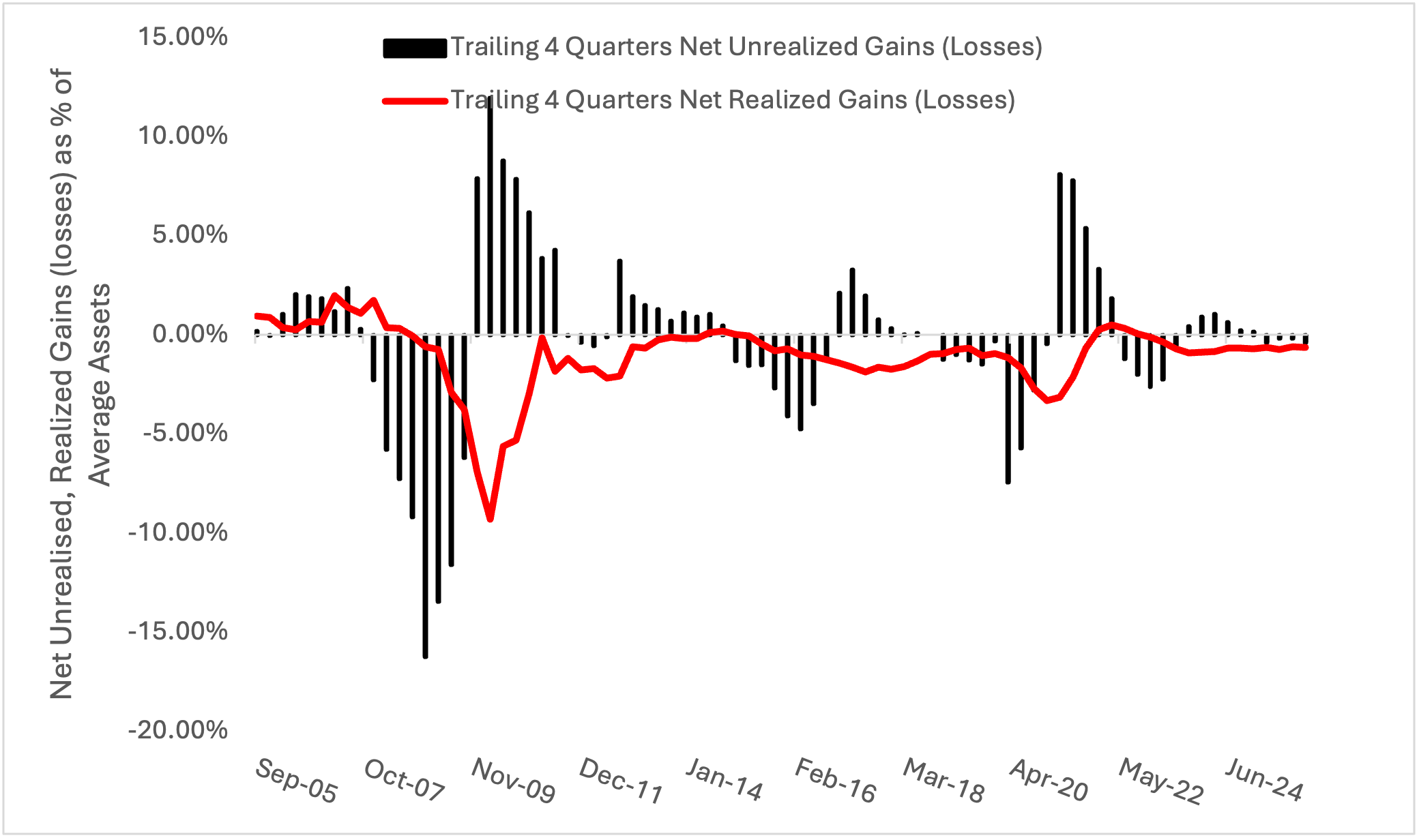

However, realised credit losses across the asset class remain relatively low by historical standards. According to the Cliffwater Direct Lending Index (CDLI), which tracks approximately 20,000 loans to U.S. middlemarket companies with data going back 20 years, losses were 0.64% during the most recent 2025 calendar year, relatively unchanged year over year and still below the long term historical realised loss rate of approximately 1.01%. Importantly, unrealized losses, a historic leading indicator of future realized losses, were low at the end of 2025, implying the market was not forecasting a rise in realized losses.

This is not to say that macroeconomic events or other factors will not lead to a rise in the future, but at this stage the data seems far more positive than the media narrative suggests.

Source: Cliffwater Direct Lending Index 31/12/2025.

The scale of the market is also important. With an underlying universe of roughly 20,000 borrowers, even a small percentage of companies experiencing financial distress can translate into hundreds of individual credit events each year.⁵ Since the inception of the CDLI realised losses have been 1 percent on an annualised basis implying an almost 2 percent default rate. Feasibly the media could report in excess of one default a day, which would have minimal impact on the overall market itself, and hence why we believe the current sentiment of systemic risk is grossly misplaced.

What the current environment tells us about private markets

Periods of elevated redemption requests are often interpreted as signs of structural weakness. In practice, they should more accurately be understood as moments when the design of semi-liquid vehicles becomes visible.

Private market investments are inherently long‑term. The structures built around them aim to balance two objectives: providing investors with periodic access to capital while avoiding forced asset sales that could erode value for remaining investors.

Diversification also plays an important role. Large direct lending funds typically hold hundreds, or in some cases thousands, of individual loans. These portfolios generate ongoing cash flows through amortisation, interest payments, refinancings and repayments as loans mature. The more diversified the fund, the more predictable this liquidity becomes given the law of large numbers, which insulates a portfolio from idiosyncratic factors.

More broadly, the current environment represents the first large‑scale test of the evergreen private markets fund model.

For advisers and investors, the key takeaway is that liquidity in private markets operates differently from public markets, but this is by design. The illiquidity of the underlying assets is not a flaw of the system – it is one of the reasons these investments have historically offered attractive long‑term return potential. For this reason, diversified portfolios typically combine private market exposures with liquid assets, balancing access to the illiquidity premium with the need for portfolio flexibility.

For financial advisers and wholesale clients only. Must not be distributed or made available to retail clients.

Betashares Capital Limited (ABN 78 139 566 868 AFSL 341181) (Betashares) is the issuer of this information. It contains general information only and does not take into account any person’s objective’s financial situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. Past performance is not indicative of future performance. Any information provided is not a recommendation or offer to make any investment or to adopt any particular investment strategy. In preparing this information, Betashares has relied on, without verification, data sourced from external parties.

Betashares does not warrant the accuracy or completeness of this information. This document may include opinions, views, estimates, projections, assumptions and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially from those reflected or contemplated in such forward-looking statements.

Footnotes

1. Acharya & Pedersen (2005); Ang (2014) – academic research on liquidity risk premiums.2. U.S. Investment Company Act Rule 23c‑3 (interval fund structures) and non‑traded BDC liquidity programs.3. Cliffwater Direct Lending Index methodology; Preqin Private Debt Reports.4. Cliffwater Research – New Private Credit Data Contradicts the Recent Risk Narrative February 23 2026.5. Cliffwater Direct Lending Index dataset (~20,000 underlying loans).