David Bassanese

5 minutes reading time

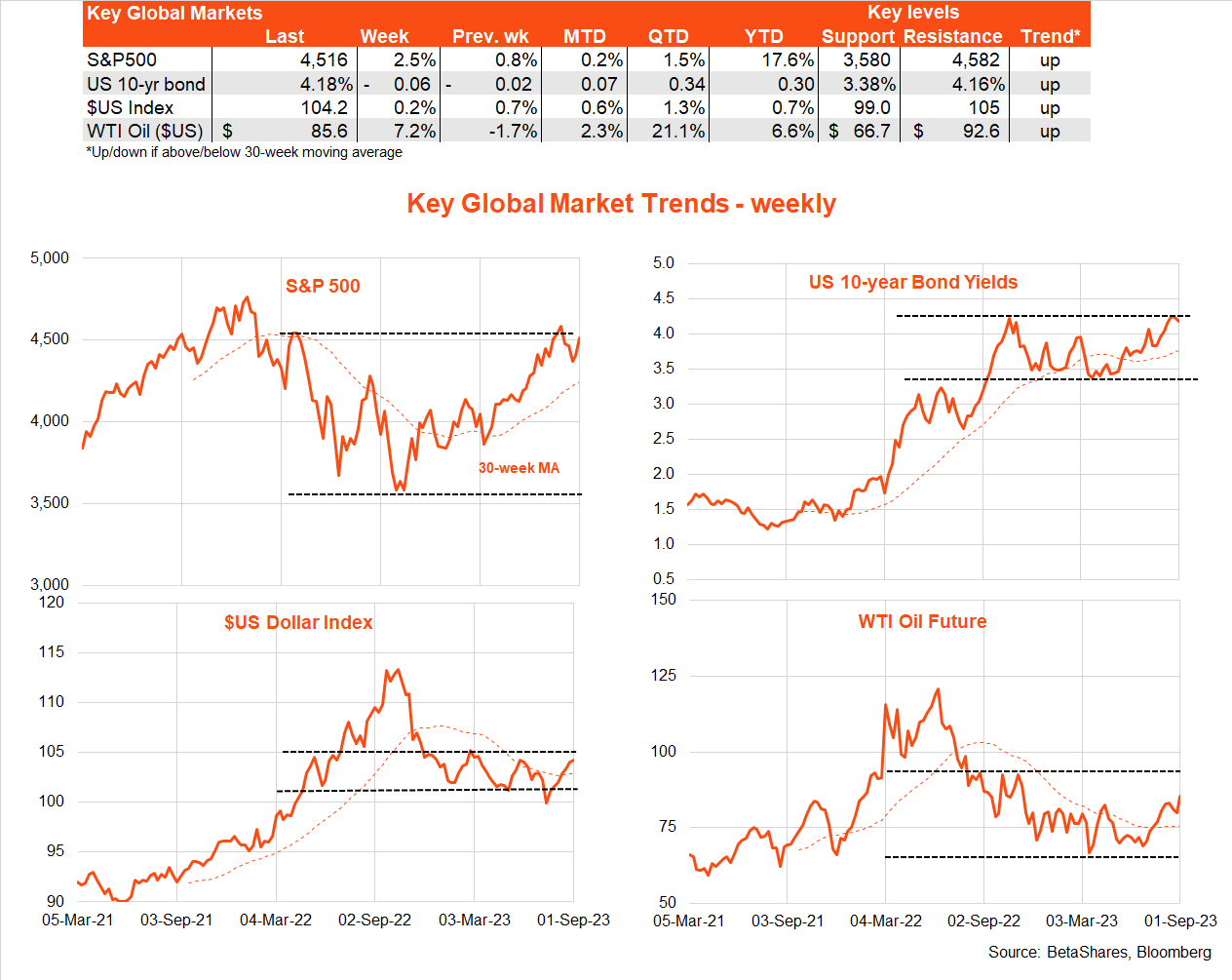

Global markets

Continued ‘Goldilocks’ reports out of the United States helped support equity and bond markets again last week, with the S&P 500 rebounding for the second week in a row. US 10-year bond yields edged lower over the week to 4.18%, from an end-week high of 4.25% two weeks ago.

Recent data have effectively ruled out the risk of a Fed tightening this month, though the market retains a 40% chance of a rate hike in November.

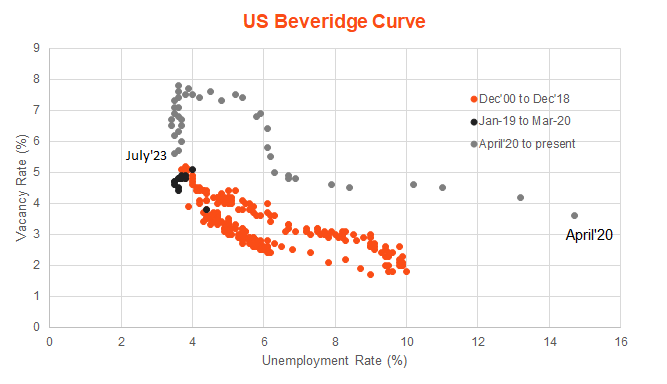

So what was so good about last week? US job openings declined a bit more than expected, while consumer prices continued to ease in line with expectations and Friday’s payrolls report indicated an ongoing cooling in the labour market.

Indeed, despite a higher-than-expected August employment gain of 187k in the US payrolls report, there were downward revisions to employment in the previous two months and the unemployment rate ticked up to 3.8% from 3.5% – driven by an increase in labour force participation. Growth in average hourly earnings was also a touch softer than expected, with annual growth easing from 4.4% to 4.3%.

As evident in the chart below, the US labour market continues to evolve in a way consistent with the (once derided) idea of ‘immaculate disinflation’, i.e. a decline in inflation without a recession. The job vacancy rate (job openings as a share of the labour force) has been falling – easing excess demand for labour – without as yet a material increase in unemployment. The black dots represent the situation in 2019, when wage and price inflation were comfortably low despite an unemployment rate around current levels – could history be repeating itself?

Of course, risks remain. One downside activity risk is that the US labour market could weaken a lot more – some analysts point to recent downward revisions to employment growth and a decline in temporary workers as potential lead indicators of more weakness ahead. An upside inflation risk, however, is the rebound in oil prices (and potentially global food prices due to El-Nino) which could start to push up headline inflation once again.

There’s little key US data of note this week, though various Fed speakers will share their views on the interest rate outlook. China will release a key services sector survey, export and import performance and its monthly consumer price index – all of which are likely to suggest the economic recovery remains sluggish. Chinese stimulus has been piecemeal so far, though markets may continue to hope for bigger measures if economic data remains soft.

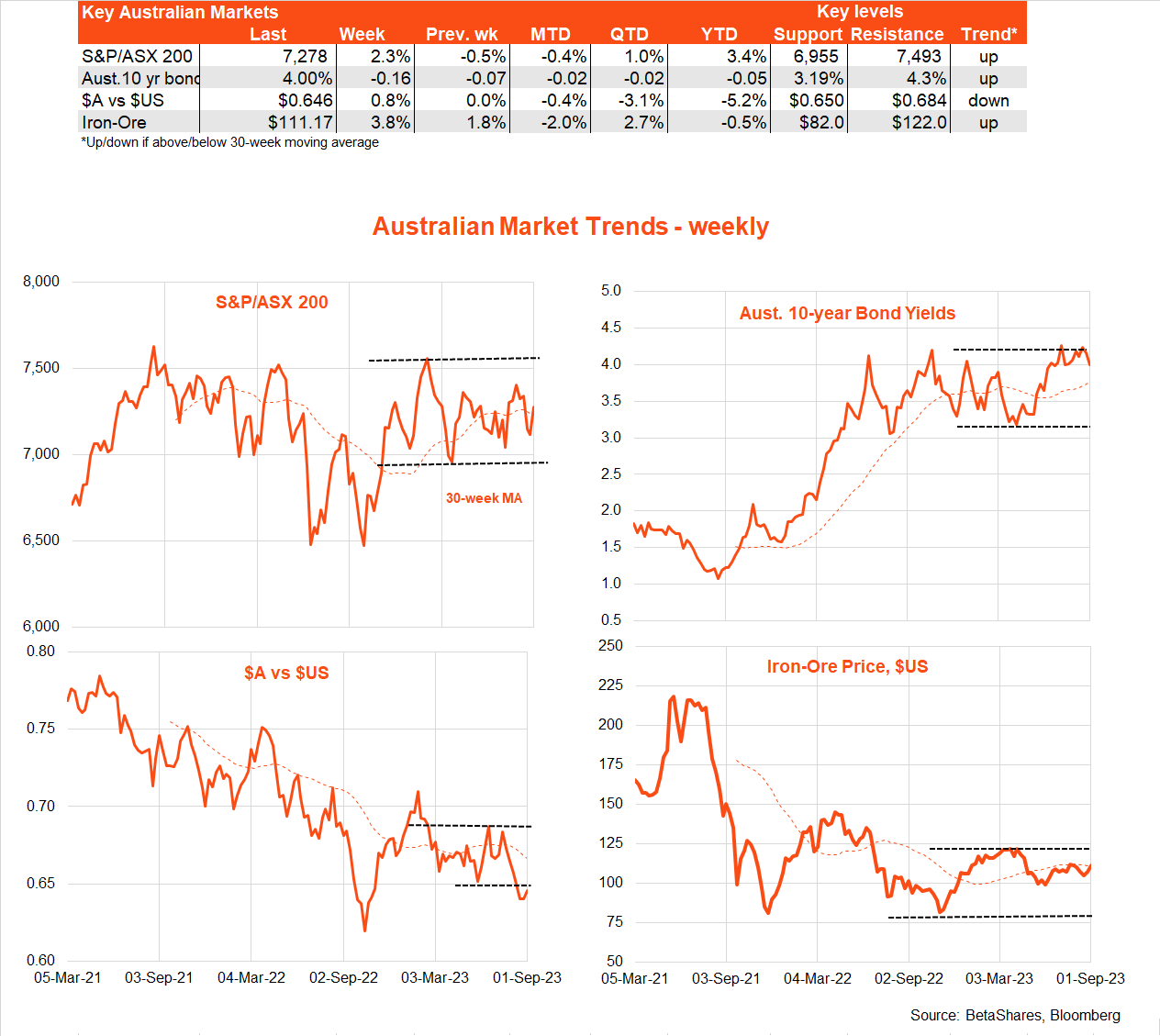

Australian market

Local stocks and bonds joined the global rebound last week, helped by further reassuring news on the local inflation front. Annual growth in the headline monthly CPI eased to 4.9%, compared to a market expectation of 5.2%. Trimmed mean annual inflation also fell nicely, from 6.0% to 5.6%. In other news, retail sales bounced back modestly in July after slumping in June – though a ‘Matilda boost’ and seasonal quirks around school holidays may have added to the strength.

Consistent with still firm business confidence, non-dwelling construction and business investment also remained firm in the June quarter – and the survey of investment expectations suggests solid business investment over 2023-24. As we’ll see in Wednesday’s Q2 GDP report, the bigger drags on economic growth remain consumer spending and housing construction. GDP is expected to grow by a modest 0.3%, with annual growth easing from 2.3% to 1.7%.

Against this backdrop, the RBA is expected to remain firmly on hold – for the third month in a row – at tomorrow’s policy meeting. I also doubt this decision will be as finely balanced as the Bank claims it has been in recent months. The two niggling concerns for the RBA at present are likely to be the soft $A (which adds to imported inflation risk) and the ongoing rebound in house prices.

But a rate hike to offset $A weakness is likely to be counter-productive – as markets may come to fear even weaker growth and deeper rate cuts later. House prices, meanwhile, have now recouped almost half their losses – due to limited market supply, rising immigration, and the fact there’s still a group of cashed-up asset-rich households prepared to ‘buy the dip’. With reports of more supply hitting the market, this could see house prices soften somewhat in spring. Either way, for the RBA this is really only relevant if stronger house prices lead to a speedy rebound in consumer spending – and so far that does not appear to be the case.

Have a great week!