Cameron Gleeson

9 minutes reading time

This is part one of an excerpt on geopolitics from the 2026 Investment Outlook. For part two, click here.

Geopolitical risks, particularly short-term ones, can often be best left ignored by strategic investors. However, US-China rivalry is reshaping the global economic order, with strategic priorities now driving trade, technology, and energy policy in ways that could profoundly impact markets. In this environment geopolitics can take centre stage of investment decisions.

Great power competition

A key part of Trump’s agenda is to dismantle the rules-based global order that the US created after World War II. He has shown disdain toward institutions, like the UN, and collective intergovernmental forums, such as the G7, that underpin multilateral cooperation between nation states. Trump believes the US’s interests are best served by bilateral negotiations of a transactional nature and unilateral actions that may ignore broadly accepted international norms.

The new world order will be defined by US-China competition across various spheres, from trade to technology, but the ramifications of this new dynamic will impact all corners of the world.

The defining characteristics of the new era are:

- Trade driven by strategic priorities rather than market forces

Tariffs, sanctions and export controls will remain a feature beyond 2025 as governments prioritise resilience and security over lowest-cost sourcing. The current US-China trade deal is best characterised as a temporary truce, rather than a comprehensive resolution of underlying structural issues. In October 2025 China issued rare earth and lithium battery export controls that, for the first time, sought to restrict how those products were used downstream outside of China (copying the extraterritorial export controls the US implemented on semi-conductors). This demonstrates how China’s supply chain dominance of critical industries gives it leverage in future tariff negotiations with Trump and other trade partners.

- State based capitalism, with an American flavour

Rather than a liberalisation of the Chinese economy we are witnessing the reverse: increasing US intervention in the economy and markets. Firstly, Biden’s Inflation Reduction Act tax and loan incentives for energy transition projects. Now under Trump, the US government has announced it will facilitate the $500 billion Stargate project, help finance a $80 billion project to build nuclear power plants, take at 15% equity stake in listed rare earths producer MP Materials, and demanded the CEO of Intel resign.

Investors need to monitor fiscal incentives, regulatory frameworks, and geopolitical developments, as these will shape sectoral performance and global capital flows. Other countries are being forced down a similar route of state support of private companies to maintain international competitiveness.

- Self-sufficiency and new strategic relationships

Much of the state-based capitalism is aimed on building self-sufficiency in critical industries. China’s focus on leadership in renewables, battery technology, semi-conductor and LLMs is driven by a goal of energy and technological independence. Europe’s new defence spending program sets the goal of sourcing 50% of procurements within the EU by 2030, rising to 60% by 20351. Meanwhile, Korean companies like Hanwha Aerospace have emerged as key suppliers for Europe’s rearmament, helping to forge new ties between countries with shared values.

- Spheres of influence

In late 2025, the White House released a new US National Security Strategy paper that signalled an important strategic pivot back towards the Western Hemisphere. Proving he is no chicken, Trump authorised a stunning military operation that resulted in the capture of Venezuelan President Nicolás Maduro and his wife.

While Washington remains deeply engaged in Europe and the Indo-Pacific and opposes Russian and Chinese influence in these regions, it increasingly expects allies to assume greater responsibility for their own military deterrence. As US support becomes less direct and unconditional, China and Russia are positioned to become increasingly influential over their regional spheres.

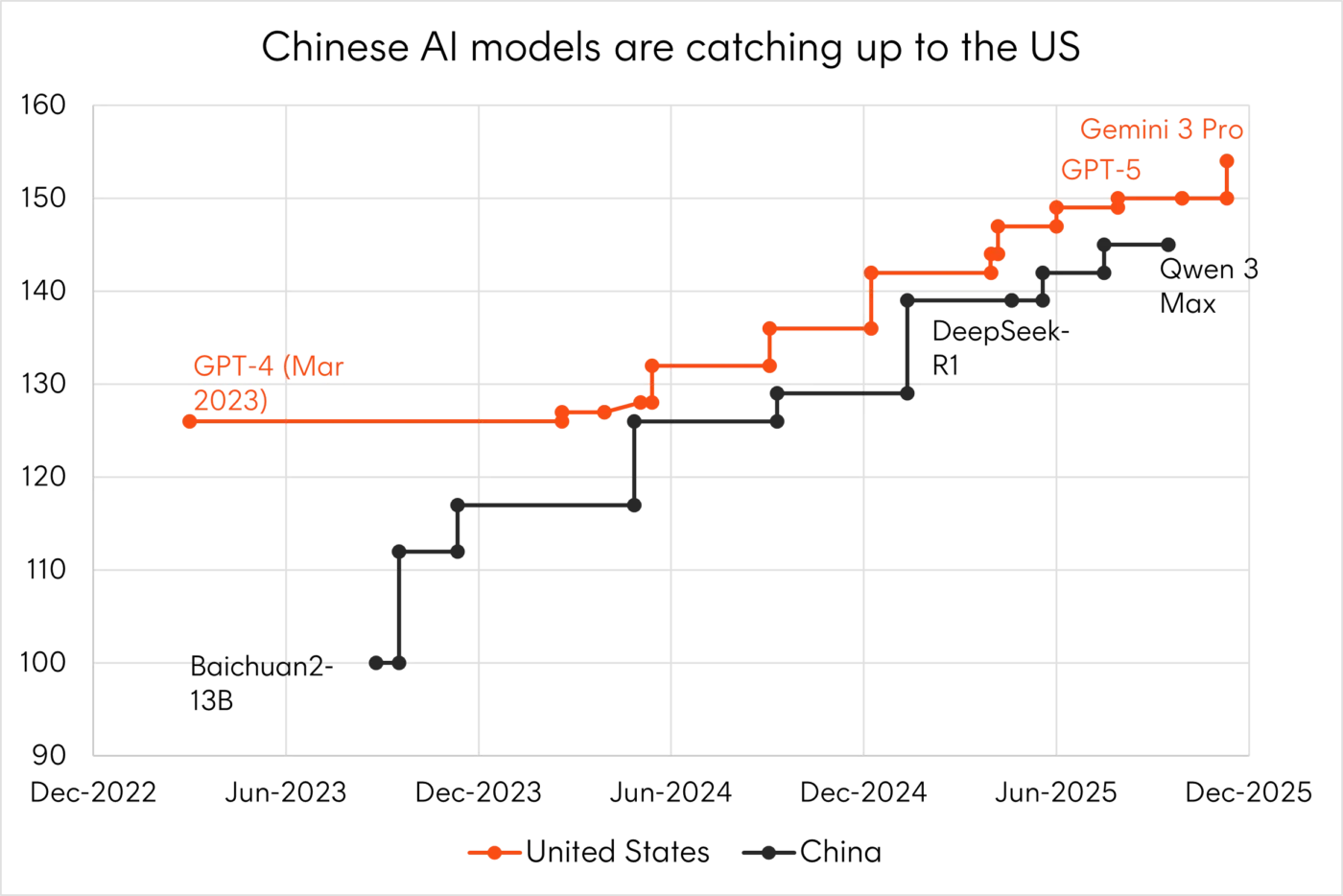

AI and energy: US vs China

With geopolitical competition now a feature of today’s world, artificial intelligence and its commensurate energy requirements have become a key strategic priority for both the US and China. While they share similar goals in achieving dominance in the global sphere, their approaches differ significantly based on their respective comparative advantages.

The US is focused on building out the best performing frontier models with the predominant goal of achieving AGI (artificial general intelligence). Given this approach requires a massive amount of data and computational power, many of the US hyperscalers have found themselves in a prisoner’s dilemma situation whereby overinvesting in AI capex poses less of a risk than underinvesting.

On the other hand, China has largely remained compute constrained since 2022 due to US export controls on high-performance GPUs. This restriction has led to two work arounds, will developers either a) build computationally efficient, open-source models like DeepSeek’s R1 model2, or b) take a brute force approach by building large GPU clusters using domestically produced chips from companies like Huawei, which require significantly more hardware and power to achieve comparable results.

Either way, Chinese model performance is beginning to challenge the leading US models.

Source: Luke Emberson, Epoch AI. Published 2 January 2026.

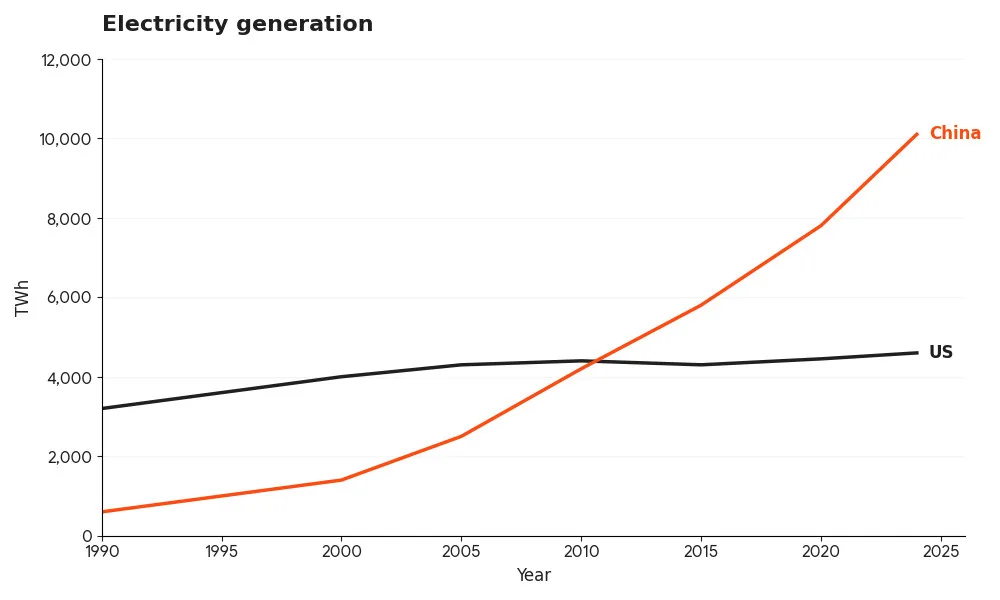

A key ingredient to winning the AI arms race (and also ensuring broader industrial strength) is access to cheap energy. On this point China and the US have also taken very different paths.

US foreign policy is fixated on “energy dominance”, which translates to producing enough oil and gas to keep domestic prices low and allow exports, thus increasing US leverage over countries buying that oil and gas. The US has cemented its status as the world’s number one producer pumping 13.5 million oil barrels per day3.

Meanwhile in China, most of the growth in generation capacity comes from zero-carbon sources. China currently has a global market share of ~75% in lithium-ion batteries, 90% in rare earth magnets; and Chinese firms lead in solar panels, wind turbines, grid equipment, as well as the EVs and drones built using these components4. This is the result of decades of industrial policy, building manufacturing scale and lowering its cost curve. The median build time for a nuclear power plant in China is 5.7 years (versus 20.8 years for the US) and China already accounts for over 40% of global planned and in-construction nuclear capacity5.

Source: Energy Institute, JPMAM, 2025

US utilities had planned flat or declining demand, but AI has reversed that assumption almost overnight. Data centres currently only represent 4% – 8% of US power demand but are projected to account for two thirds of load growth6. The US will struggle to add generation capacity and transmission grid infrastructure fast enough and in the right locations. Cheap oil is not enough to fuel the AI boom. China, with its centralised planning and stronger energy industrial base, can turn electricity generation into a competitive advantage in the AI arm’s race.

Geopolitical risks for 2026

We acknowledge that predicting geopolitical risks are hard. Nevertheless, below are some potential developments that may unfold in geopolitical hotspots around the world in 2026:

- Further US intervention in the Western Hemisphere

Venezuela is not a significant enough oil producer for further instability to impact global oil markets. However, 2026 might bring implications for lithium, copper and other critical minerals, on increased cooperation between the US and new right-wing presidents in Chile, Argentina and Peru. A US invasion of Greenland appeared unlikely and is now off the table.

- Regime change in Iran risks global oil supply attack

At the time of writing the government of Iran appears to have quelled nationwide protests, while a US “armada” has gathered in the Persian Gulf. A regime change would disrupt Iran’s oil supply. Any foreign strike on Iranian leadership would be viewed as an existential threat, provoking retaliation. Saudi and Iraqi oil production as well as Israel and the Strait of Hormuz would be the most likely targets.

- Russia continues to threaten Europe

One possible positive outcome for 2026 is a peace agreement in Ukraine, accompanied by a substantial fiscal expansion in Europe to fund reconstruction. In any case, Russia is likely to continue testing Europe’s resolve through sabotage and airspace incursions. As a result, European defence spending is likely to increase, although populist parties may push back against the cost of collective security.

- China adopts the Beiping model for Taiwan

China will likely use the US actions in Venezuela to diplomatically strengthen its alliances in Asia and the Global South. It will continue to conduct military exercises that demonstrate that it could blockade Taiwan and engage in psychological and political warfare, rather than initiating a full-scale war. Frictions over these actions could result in periodic re-escalations in the US China trade war.

Investment implications

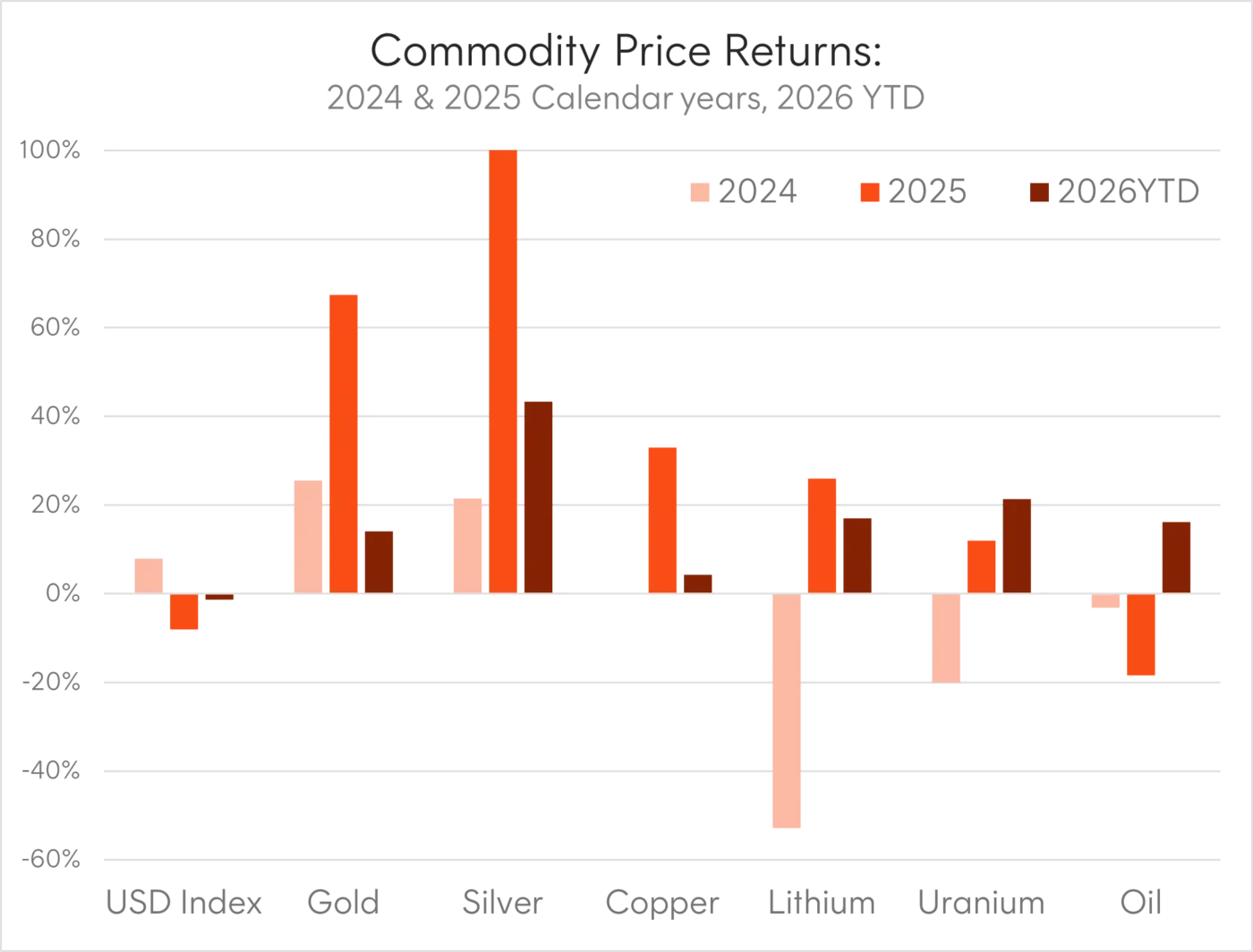

The potential developments above all have implications for investors. But the perhaps the return potential from geopolitical risk is best illustrated by the size of the price moves seen in the US dollar, and various commodities, including precious metals and critical minerals, over the last couple of years.

Source: Bloomberg, 29 December 2023 to 31 January 2026. The 2026YTD return is measured from 31 December 2025 to 31 January 2026 is Past performance is not an indicator of future performance.

Investors in this new world order may look to align themselves with the strategic importance of global choke points like the AI supply chain or critical minerals. The earnings growth of shifts in Fiscal support to key industries also provides an opportunity for upside. Furthermore, investors should consider how to best insulate their portfolio from downside in the event of a geopolitical shock. Please see the follow-on insights piece, Hedging geopolitical risk, for more details and ETF implementation ideas.

Sources:

1. European Commission and High Representative, “White paper for European defence – Readiness 2030,” March 19, 2025 ↑

2. DeepSeek’s latest model is expected to be released mid Fed 2026. ↑

3. Source: U.S. Energy Information Administration (EIA), January 2025. ↑

4. Source: Ember, “China Energy Transition Review 2025,” September 2025 ↑

5. Source: World Nuclear Industry Status Report 2025, November 26, 2025. ↑

6. US Department of Energy, Report on U.S. Data Centre Energy Use, December 2024. ↑