Betashares

Super contributions are payments made into your super account, either by your employer or by you.

Throughout our careers, for many of us super is a compulsory amount paid by your employer and it ticks on in the background. But that can change as retirement approaches.

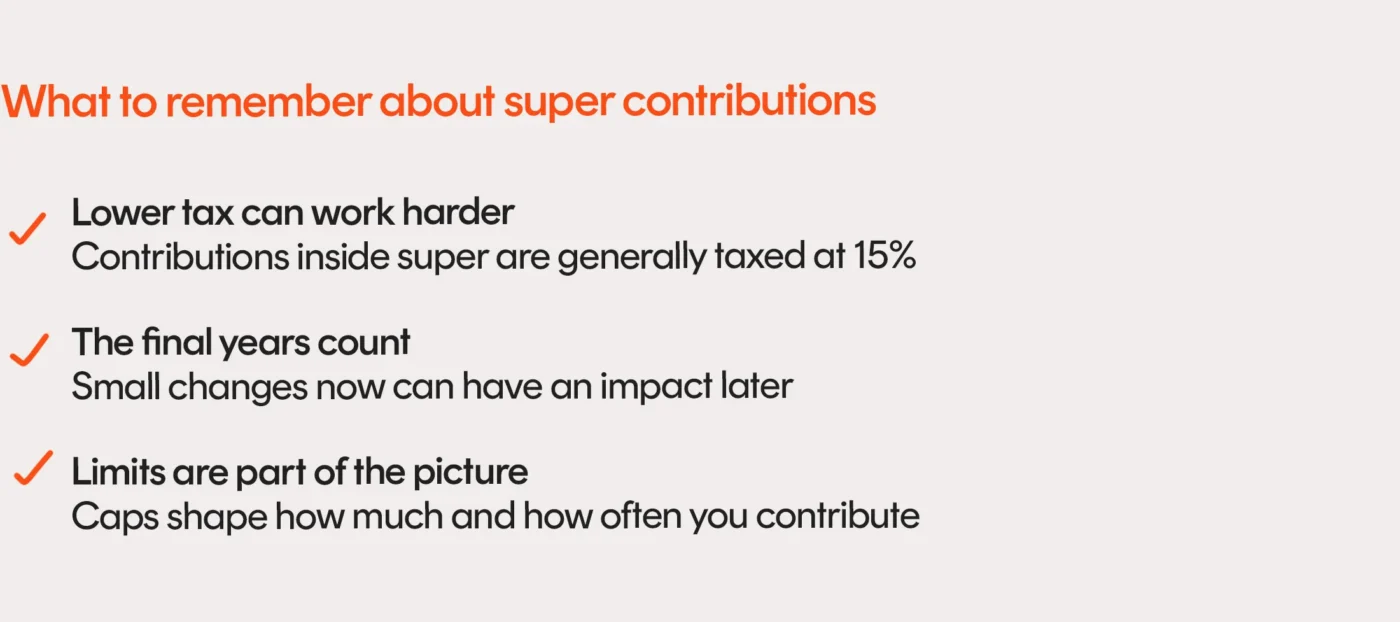

In the years before you stop working, super contributions can become one of the most effective levers you have – to reduce tax, boost your balance and shape the income you’ll eventually rely on.

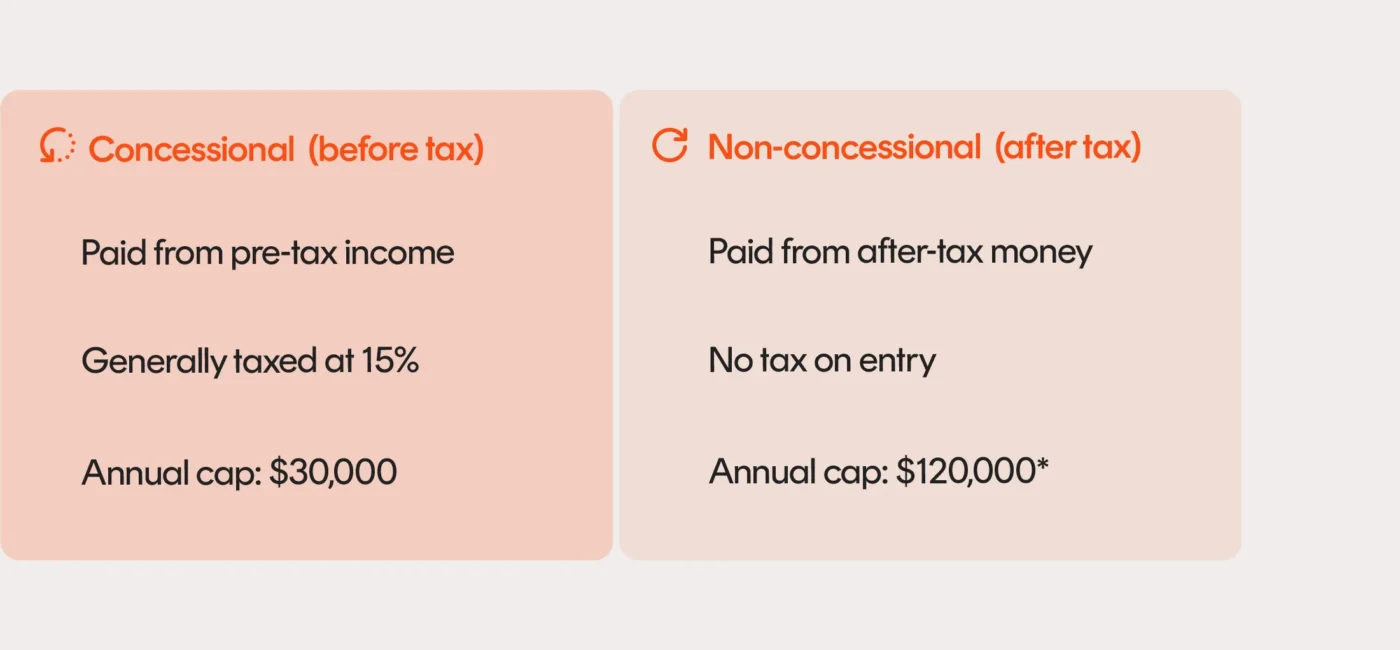

The two types of super contributions

All super contributions fall into two categories:

- Concessional (before-tax) contributions

- Non-concessional (after-tax) contributions

The real impact can often come down to when tax is paid on your contributions – and that difference can add up quickly.

*Non-concessional contributions are not taxed when they enter the Fund. However, there is a limit on how much you can contribute each year, known as the non-concessional contributions cap. For the 2025-2026 financial year, this cap is $120,000 per person per financial year, provided your total super balance, as at 30 June of the previous financial year is less than $2.0 million. You can also check if you’re eligible to bring forward the equivalent of 1 or 2 years of your annual cap from future years. To learn more about the bring forward arrangement visit the ATO website.

Concessional contributions (before tax)

Concessional contributions are made from pre-tax income and are generally taxed at 15% inside super. These include:

- Employer super contributions under the Superannuation Guarantee

- Salary sacrifice, where part of your pre-tax salary is directed into super

- Personal deductible contributions (PDCs), which you claim as a tax deduction

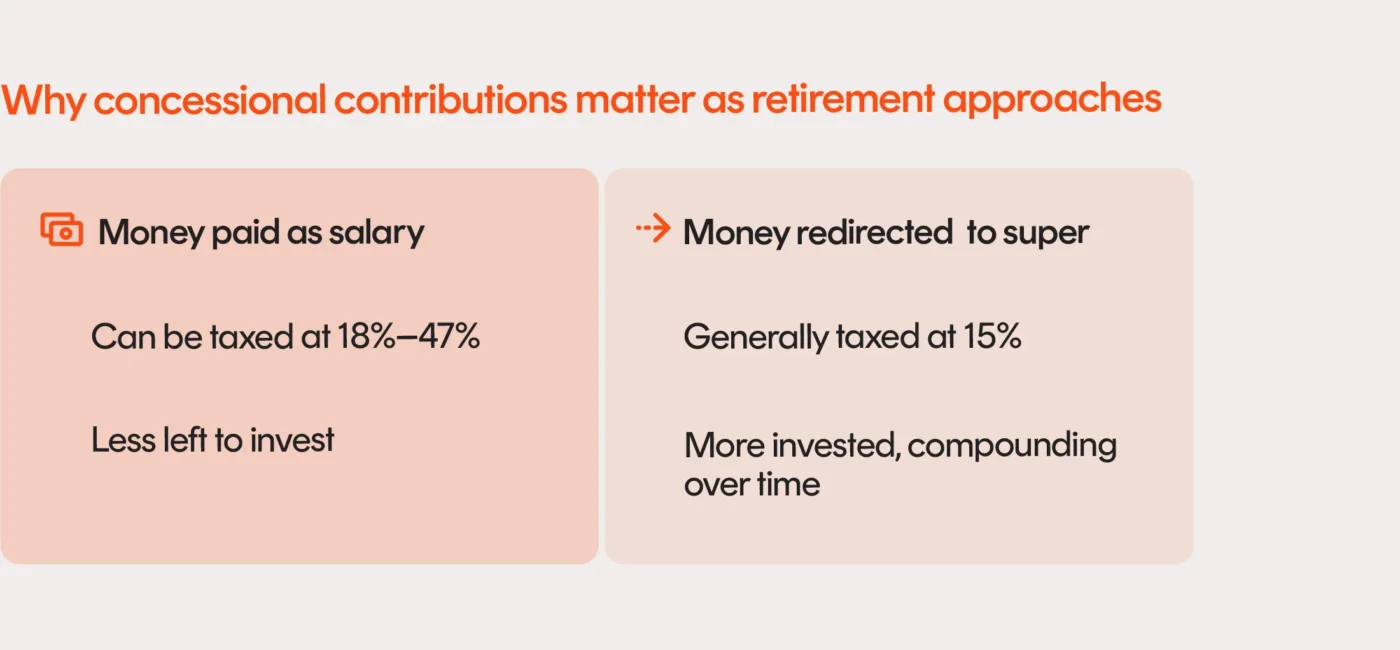

Why the 15% tax rate matters

If you earn enough that your marginal tax rate is 30% or higher, your salary is taxed more heavily than concessional super contributions, which are generally taxed at 15%. This makes salary‑sacrificed super a tax‑effective way to save for retirement.

It means money redirected from salary into super is often taxed at a lower rate than your income and stays invested for the years ahead. Even a few years of maximising concessional contributions can impact the size – and sustainability – of retirement income.

Thinking beyond your own super

As retirement approaches, super planning often shifts from individual decisions to household ones.

Depending on your circumstances and eligibility rules, spouse contributions may provide tax offsets or help manage balances ahead of retirement. You can find more information on spouse contributions here.

Government co-contributions can also apply for people on lower incomes who make non-concessional contributions. While more common earlier in a person’s working life, they may still apply if your income falls below the relevant threshold. For the latest details on super co-contributions, visit the ATO website.

What happens when you move into retirement

It’s worth knowing that there’s a limit on how much super you can transfer into the tax-free retirement income phase.

This is known as the Transfer Balance Cap and is currently $2.0 million (as at 1 July 2025). Amounts above this generally remain in the accumulation phase or are withdrawn as a lump sum.

Understanding how contributions work – and where the limits sit – can help you make more confident, deliberate choices before retirement.

An exciting future in superannuation

Betashares has recently acquired Bendigo Superannuation. Learn more about the acquisition and our future plans in superannuation.

This information is current as at 1 July 2025 and may be subject to change. You should not rely on this article to determine your personal tax obligations or other entitlements.

Bendigo Superannuation Pty Ltd (ABN 23 644 620 128 AFSL 534006) (Bendigo Super) is the trustee and issuer of Bendigo SmartStart Super and Bendigo SmartStart Pension (Products). Before making an investment decision in relation to the Super Products, read the relevant Product Disclosure Statement, available from this website (www.betashares.com.au/super/documents) or by calling 1800 033 426, and consider whether the product is right for you. You can find the Bendigo SmartStart Super Target Market Determination here and the Bendigo SmartStart Pension Target Market Determination here. This information is general in nature and doesn’t take into account any person’s financial objectives, situation or needs. You should consider its appropriateness taking into account such factors and seek professional financial advice. Past performance is not indicative of future performance.