Hugh Lam

6 minutes reading time

The tech selloff in context

The artificial intelligence theme has largely driven equity market returns since November 2022, but the tech sector faces fresh challenges.

The release of new agentic AI tools has raised questions about the viability of legacy software business models, while higher than expected hyperscaler capital expenditure commitments have led to broader unease.

“…the current AI repricing of public companies is a process of asking “if” any future cash flows are safe. We used to debate “when” those cash flows would degrade – in 10 years? 20 years? Now the question is if these future revenues (and RPO) have ANY value.” – Chamath Palihapitiya, Canadian-American venture capitalist and founder of Social Capital on X

However, the underlying story is more nuanced than what the selloff implies. Even as legitimate questions remain around the future of software, or whether AI-driven economic value circulates more broadly or concentrates toward the upper end of the income distribution, the productivity benefits of AI are becoming increasingly evident across the US economy.

Ultimately however, uncertainty is often a feature of major technological shifts and should serve as an important reminder of the value of diversification during periods like this.

Beyond the Magnificent 7

The Nasdaq 100 has always provided investors exposure to the innovation and creative destruction of the dynamic US technology sector. Since its inception, the index has cycled through successive waves of technological disruption from the Internet to cloud-computing, continuously replacing the companies that failed to adapt with those that drove the next cycle forward.

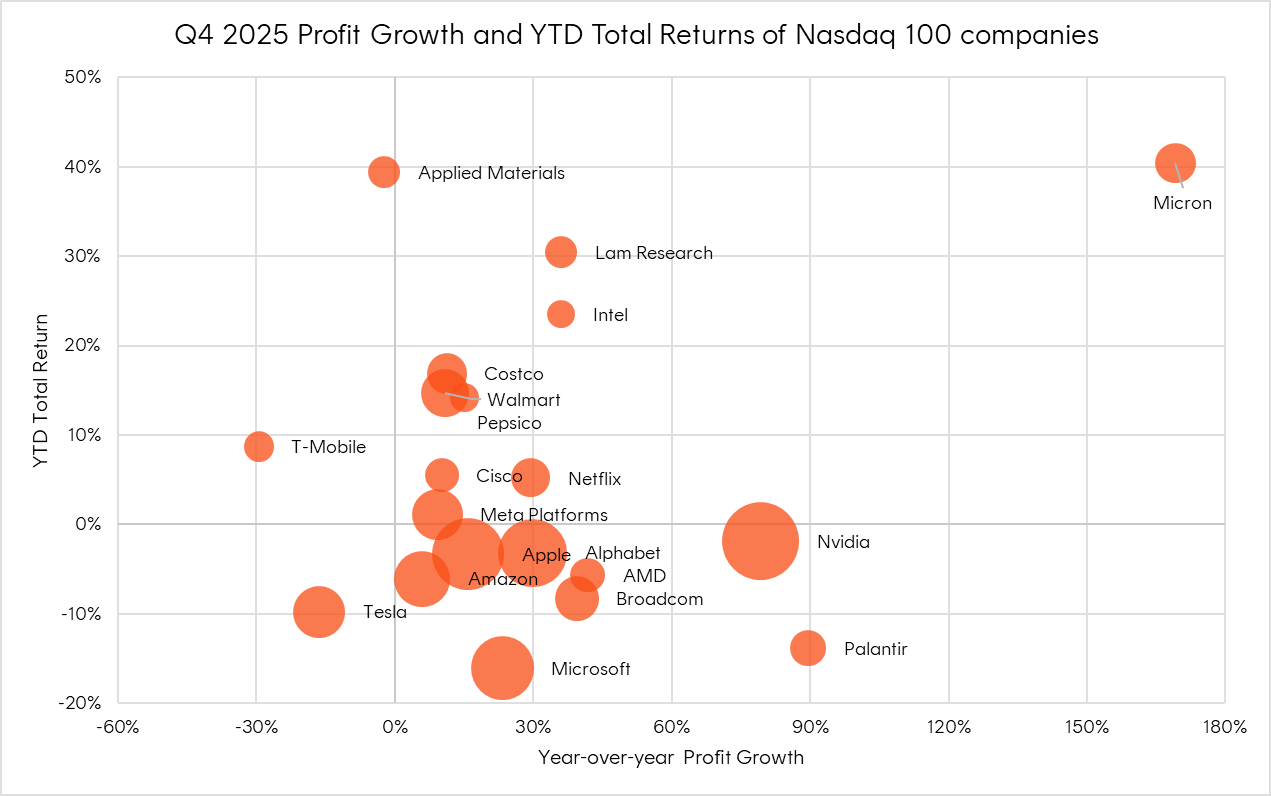

That evolution is taking place yet again as investors discern who will be the winners and losers of AI. Share price dispersion has widened significantly among the Magnificent 7 since Q4 2025, while earnings growth is broadening out to the other 93 companies within the index.

In fact, some of the largest contributors to its returns over the last 6 months have been “non-Magnificent 7” semiconductor stocks like Micron Technologies, Lam Research and Applied Materials that have benefited from the hyperscaler capex juggernaut that accounted for roughly a third of US GDP growth last year.

Source: Nasdaq Global Indexes, FactSet. As of March 4, 2026. Financial results have been adjusted to remove certain expenses such as one time costs or stock-based compensation.

Still, the sheer scale of this spending alone has also contributed significantly to the hyperscaler’s cloud segments where revenues re-accelerated during the most recent reporting season. Amazon’s AWS and Microsoft’s Azure now have more than US$100 billion in annualised revenue, while Google’s cloud platform was the standout performer, growing revenues by 48% year-over-year (yoy) as enterprises shifted workloads from experimentation to full-scale production.

|

Cloud Platform |

Q4 2025 Revenue (USD) |

YoY Growth |

ARR (USD) |

|

AWS |

$35.6B |

24% |

$142B |

|

Microsoft Azure |

$32.9B |

29% |

$131B |

|

Google Cloud |

$17.7B |

48% |

$71B |

Source: Company filings.

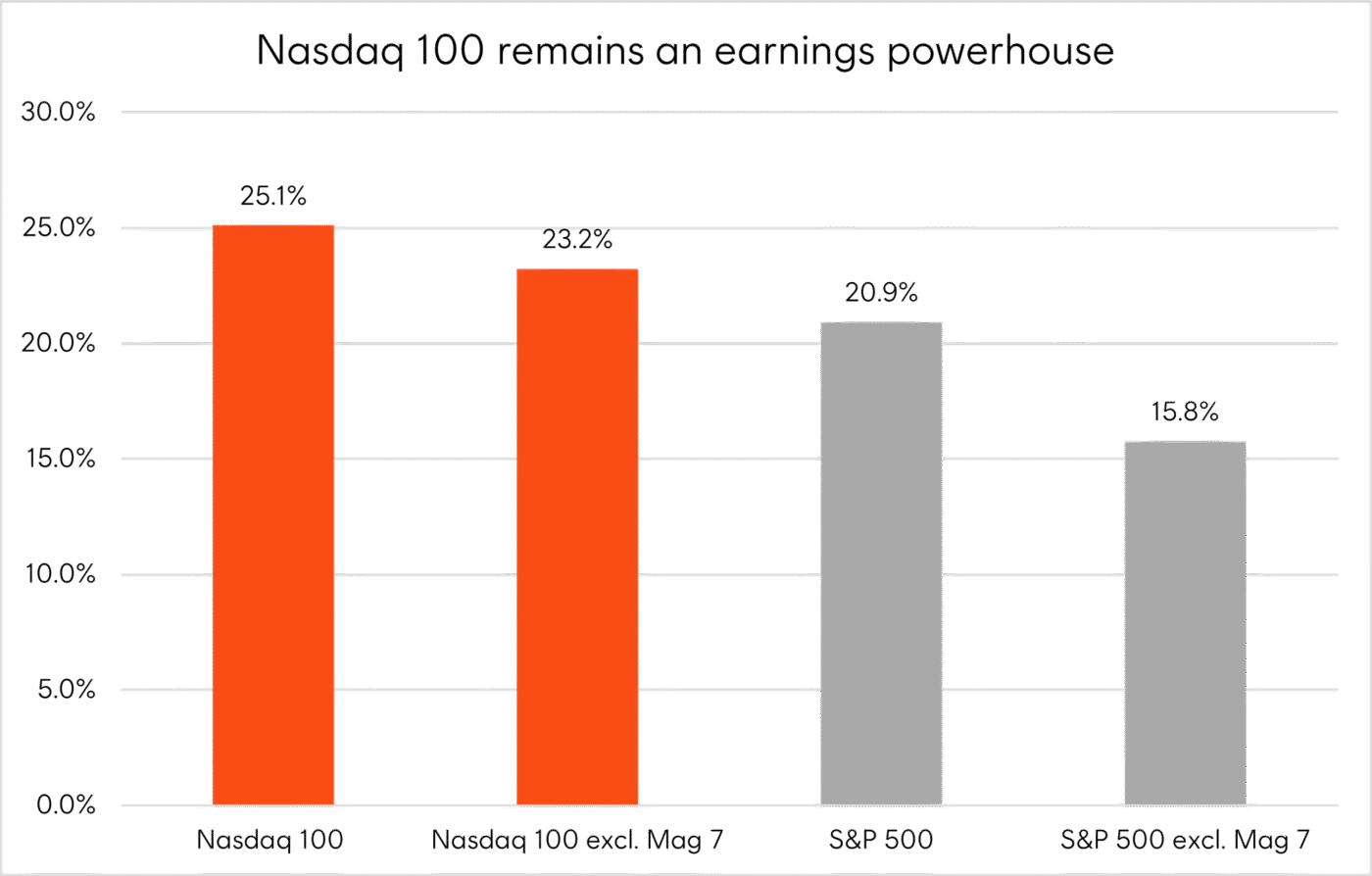

All in all, the earnings strength of the Nasdaq 100 continues to drive its performance and justify current valuation levels. The index grew earnings by 25.1% yoy1 during the most recent Q4 2025 reporting season – its 11th straight quarter of double-digit earnings growth. Even when excluding the Mag7, the Nasdaq 100 grew earnings significantly faster than the S&P 500 ex-Mag7 at 23.2% compared to just 15.8%. Record corporate buybacks (surpassing US$1 trillion) and strong M&A activity were also key drivers to index performance.

Source: Nasdaq Global Indexes, FactSet. As at 5 March 2026.

While renewed geopolitical and trade uncertainty have driven a marginal de-rating in risk assets over recent weeks, the exceptional earnings profile of the Nasdaq 100 should help underpin continued performance in index returns this year. Additionally, Asian semiconductor suppliers like TSMC and Samsung/SK Hynix are establishing manufacturing capabilities in the US, reducing long-term geopolitical supply chain risk – though near-term cost pressures from higher fab costs and rising HBM memory prices remain a consideration.

The big picture: Macro tailwinds may provide further support

Beyond earnings, supportive financial conditions and fiscal policy provide additional tailwinds for the Nasdaq 100.

A weaker US dollar could provide a tailwind for companies with high exposure to international sales, compared to those with more domestic US sales. This is because a weaker US dollar boosts reported company earnings when foreign sales are converted back into dollars. The Nasdaq 100 generates approximately 50% of revenues outside of the US, meaning companies within the index could receive an above-average tailwind from USD weakness.

Lower interest rates will also benefit growth-oriented companies with future cash flows and valuations supported by lower costs of capital. While interest rate cut expectations have been pared back following a pick-up in core inflation and higher oil prices from the ongoing fallout in the Middle East, the Federal Reserve is still on track to deliver 1.5 cuts according to market pricing as at 6 March 2026.

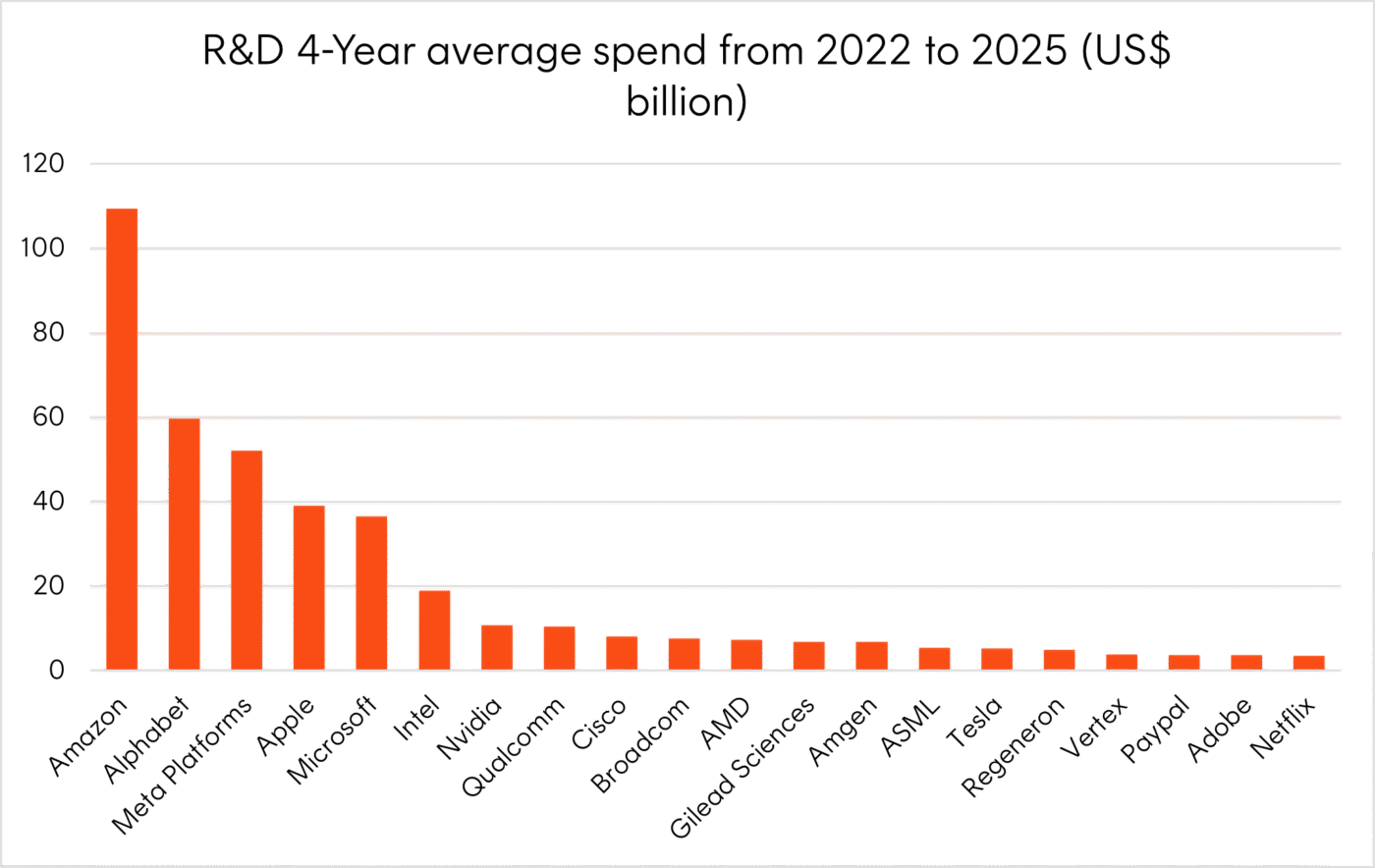

Finally, Trump’s One Big, Beautiful Bill Act (OBBBA) includes an incentive to encourage companies to spend more on R&D. This incentive allows companies to immediately expense domestic research and development (R&D) costs, in turn reducing both taxable income and tax payments. It is expected to provide a marginal boost to free cash flows for companies investing heavily in innovation, benefiting technology companies such as Amazon, Alphabet, and Meta.

Source: Nasdaq Global Indexes, FactSet.

Investment Implications

The Nasdaq 100 has never offered a smooth ride — but it has consistently rewarded investors who recognised that periods of creative destruction are precisely when the index’s self-renewing structure is most valuable. With eleven consecutive quarters of double-digit earnings growth, a broadening earnings base beyond the Magnificent 7, and the AI infrastructure supercycle still powering ahead, the fundamental case remains intact.

For investors seeking exposure to the companies defining the next decade of the global economy, volatility is the price of admission — and historically, it has been worth paying.

NDQ is Australia’s only ETF which aims to track the performance of the Nasdaq 100 Index (before fees and expenses), giving investors direct exposure to many of the biggest companies in the world such as Apple, Amazon and Nvidia all in one trade. Since its inception in May 2015, NDQ has returned 18.60% p.a. to its investors.

-

Source: Nasdaq Global Indexes. ↑