Hugh Lam

4 minutes reading time

Markets breathed a sigh of relief overnight following President Trump’s plan to end the war without fully reopening the Strait of Hormuz.

While US stock markets rallied, the situation remains far from over with elevated oil prices creating real demand destruction in parts of Asia. If unresolved, the negative supply shock (~11 million barrels per day) may lead to more persistent inflationary pressures and weigh on global growth expectations.

The Houthi’s threat to Red Sea shipping may also present another left-tail risk. While oil is finding its way through an ‘escape hatch’ to the Yanbu port located on Saudi Arabia’s West coast, the Iranian backed Houthi’s could add more fuel to the fire by blocking the Bab al-Mandab Strait.

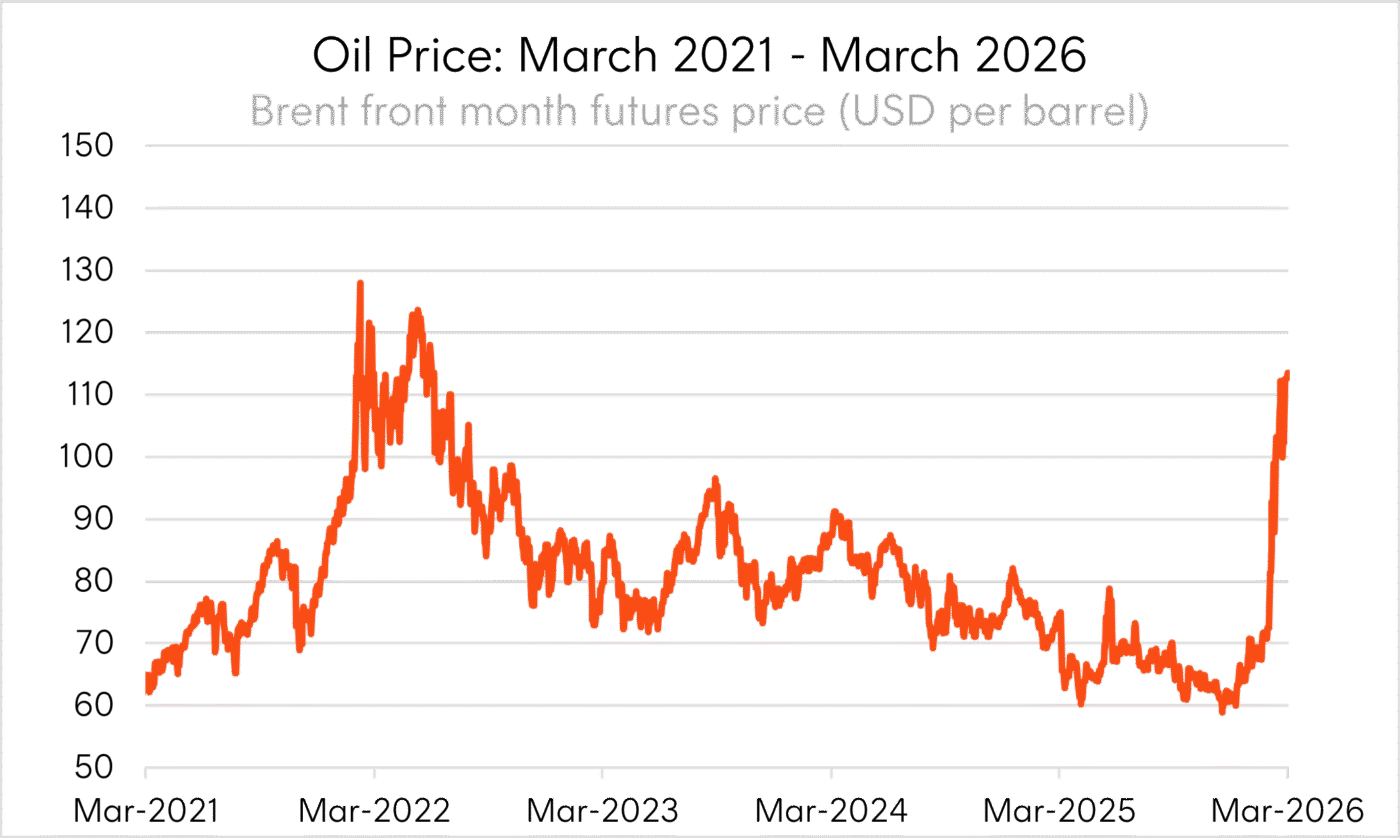

1 – But I’m feeling (twenty) twenty-two ♫

Oil prices have surged above US$100/barrel following the outbreak of war between the United States-Israel and Iran, and back to 2022 levels when Russia invaded Ukraine.

In response to the surprise US-led attack, Iran has placed an effective close on the Strait of Hormuz, a major chokepoint that sees roughly 20% of total global oil consumption transiting through it every day.

Source: Bloomberg. As at 31 March 2026.

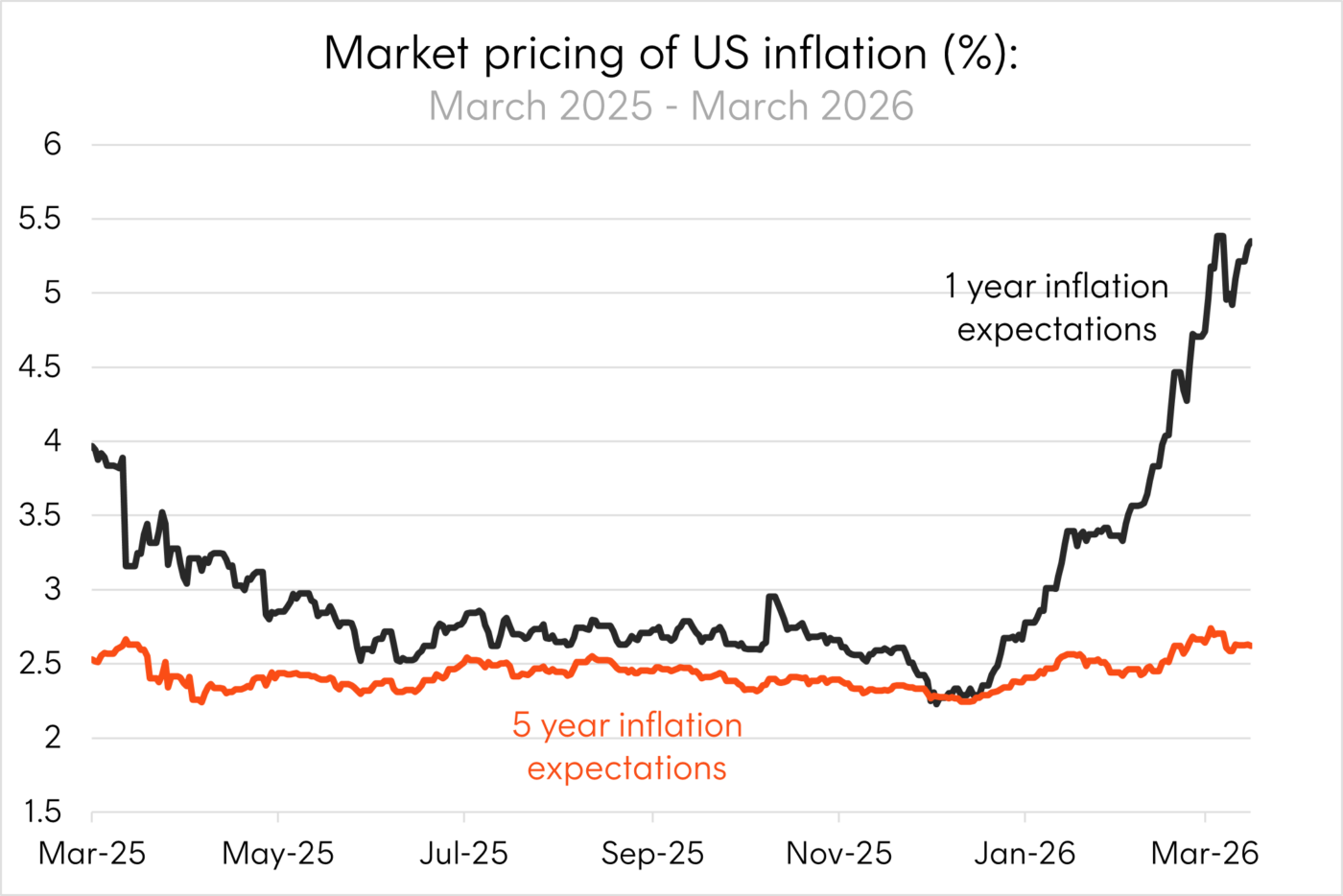

2 – Long-term inflation expectations well-anchored

The negative supply side shock in energy markets has fed through to inflation expectations with US 1-year breakevens climbing to ~5.35%. That said, 5-year breakevens (which measures expectations for average annual inflation over the next five years) remain far more contained at around 2.6%, suggesting the spike in oil prices may be temporary.

Source: Bloomberg. As at 31 March 2026.

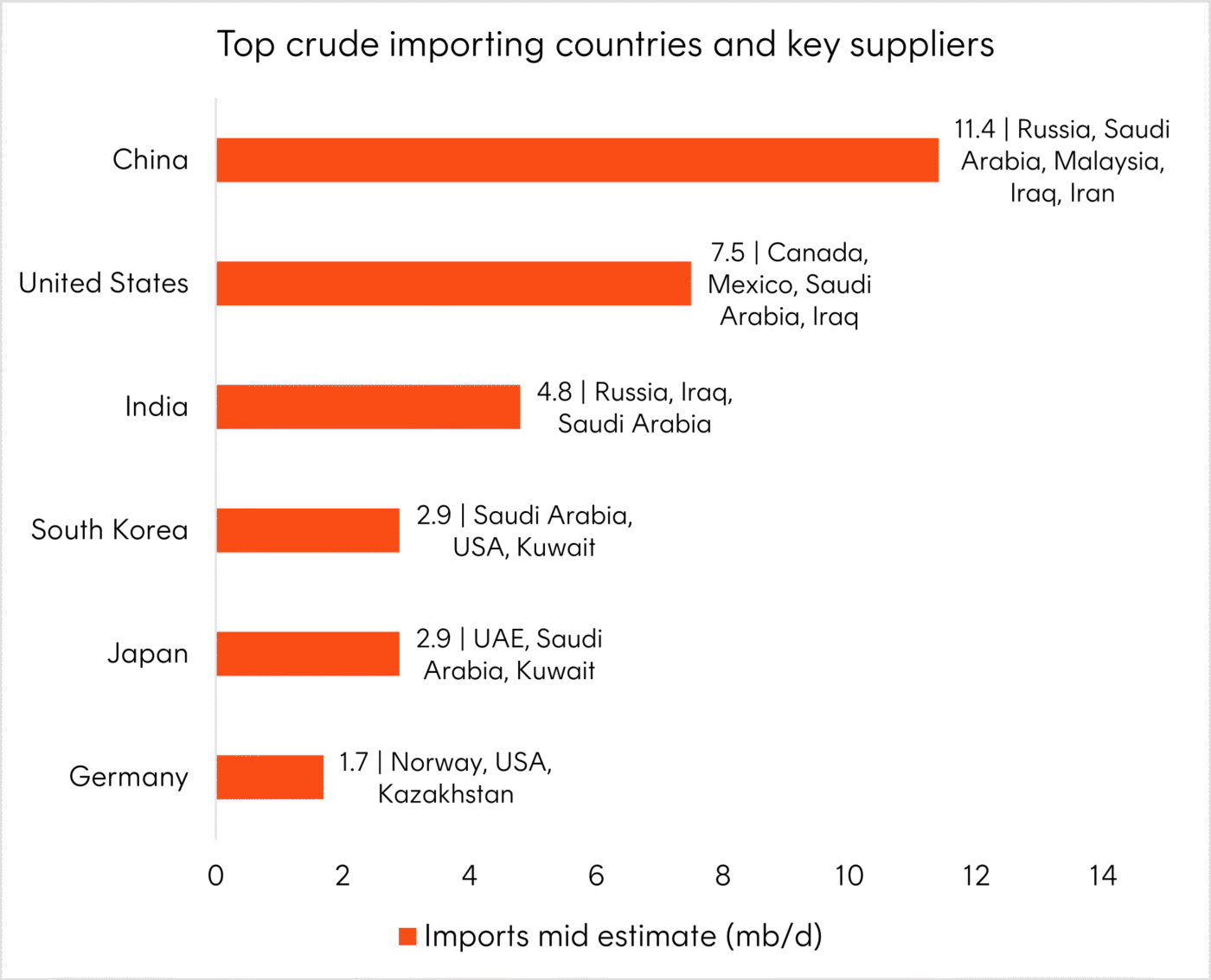

3 – Asian economies are facing real demand destruction

The key risk, however, is whether the Strait of Hormuz remains closed for longer than markets are expecting. In this scenario, major oil importing countries would be more negatively affected as the risk of broader inflation increases, and economic growth slows due to a reduction in discretionary spending.

In response, some countries like Pakistan have already implemented a four-day work week and 50% work from home policy for government employees to conserve fuel. Australia will halve the fuel excise on petrol and diesel for three months, and Sri Lanka has declared Wednesdays a public holiday for government institutions such as schools and universities.

Source: Estimates based on recent trade data, 2024–2025. mb/d = million barrels per day.

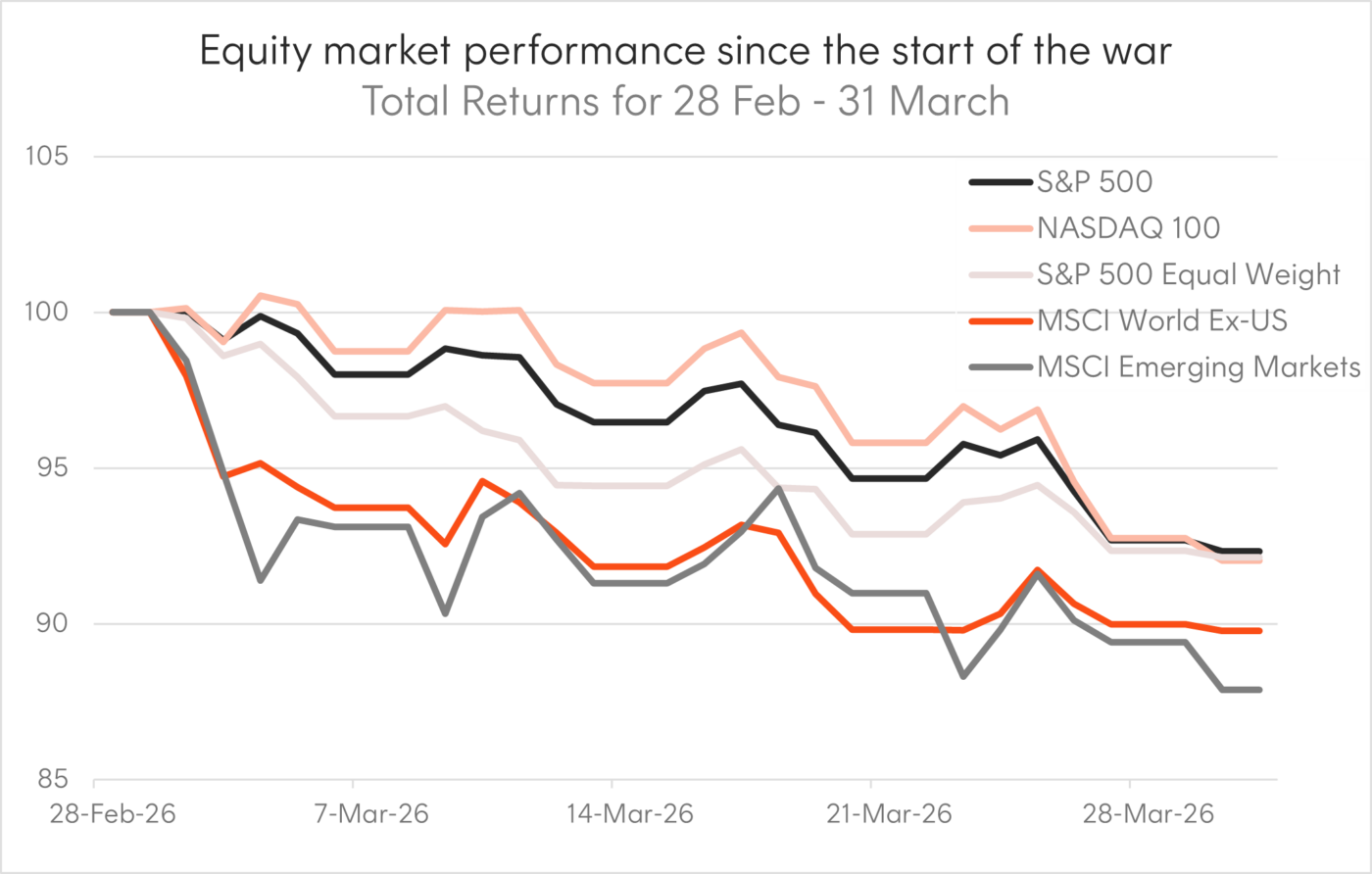

4 – How have global share markets responded?

The US sharemarkets have been relatively more resilient compared to the rest of the world given the market’s view that America’s shale production would be enough of a shock absorber to the rise in spot oil prices. i.e., the US is a net oil exporter while Europe and Asia are largely net oil importers.

However, US shale output has been drifting down with frackers having cut the number of active drilling rigs in the Permian Basin to 243 from 300 a year ago, according to US energy technology company Baker Hughes1.

Source: Bloomberg. As at 31 March 2026. Rebased to 100 as at 28 February 2026. Past performance is not indicative of future returns future returns

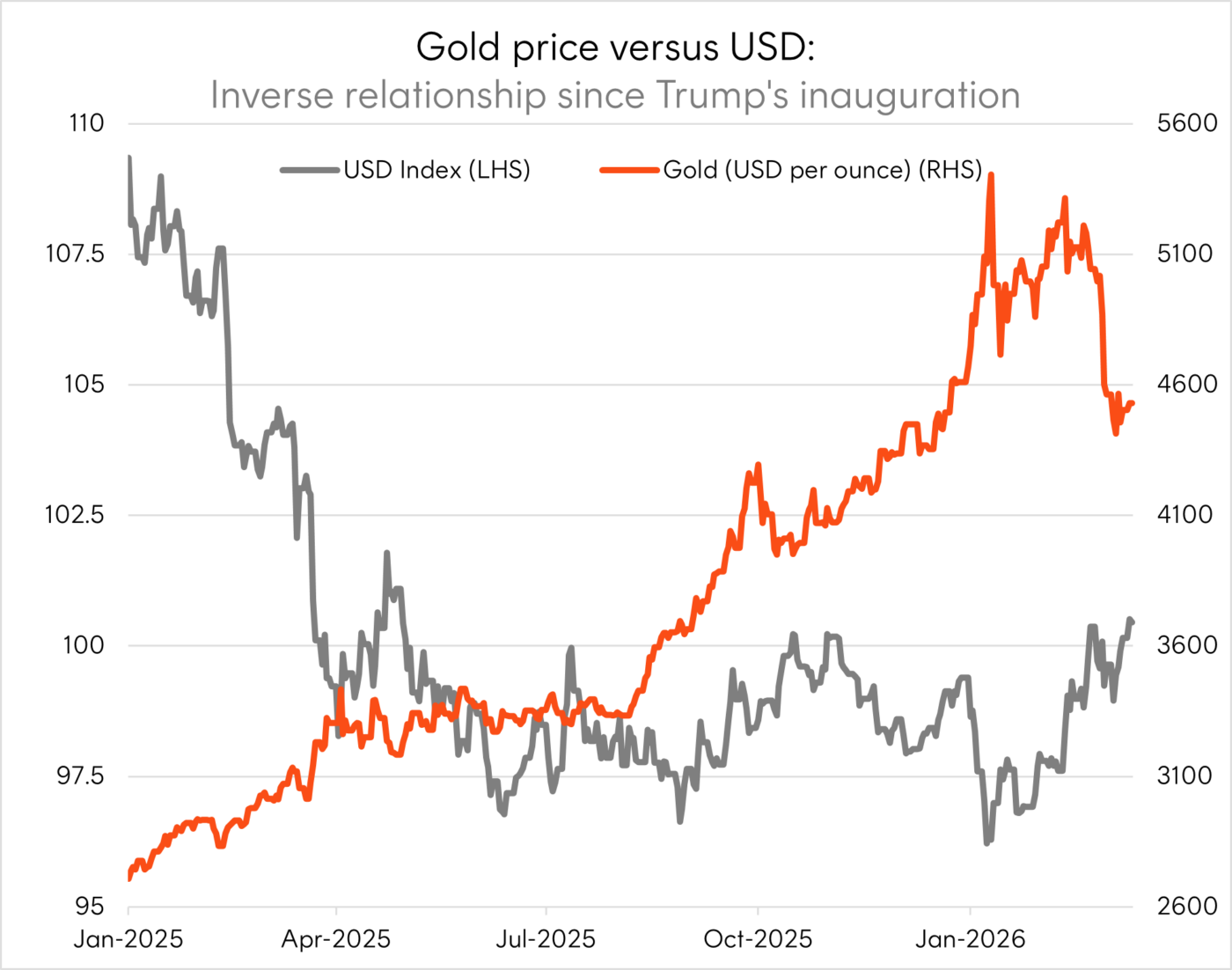

5 – What about gold?

Gold’s price reaction since the outbreak of the war may be confusing for investors given it’s often regarded as a ‘safe haven’ asset in times of volatility and economic uncertainty.

While the yellow metal initially appreciated at the outbreak of the crisis, it has sold off as expectations of US rate cuts were pushed back (due to higher inflation expectations) while the US dollar has strengthened. Additionally, investors may have been selling gold to take profits and de-risk their portfolios because of losses in other asset classes.

Source: Bloomberg. As at 31 March 2026. Past performance is not indicative of future returns future returns.

Source:

2 comments on this

Very interesting overview, thank you! What was missing though is some historical data, or even just a brief mention of how accurate these “inflation expectations” are. Without that, it’s hard to know how seriously these numbers can be taken.

…just to clarify my previous comment, those sentiments, the inflation expectations undeniably have the power of moving the markets I’m just curious about the predictive accuracy of them. I suspect they are generally more or less “on the money” but may have blips of inaccuracy during something like the COVID disruption and other world shaking surprise events.