Currency hedged, tax exposed: is history about to repeat?

Key points

In 2026 we have seen increased appetite for currency hedged ETFs from asset allocators seeking to position their portfolios for an appreciating Australian dollar (AUD). This includes very significant inflows into our own Global Shares Currency Hedged ETF (ASX: HGBL).

At face value currency hedging has been the right call over the last twelve months, with AUD now trading above USD 0.711. However, some investors in currency hedged funds and ETFs might be about to receive a rude shock when it comes to tax time.

What happened in 2021

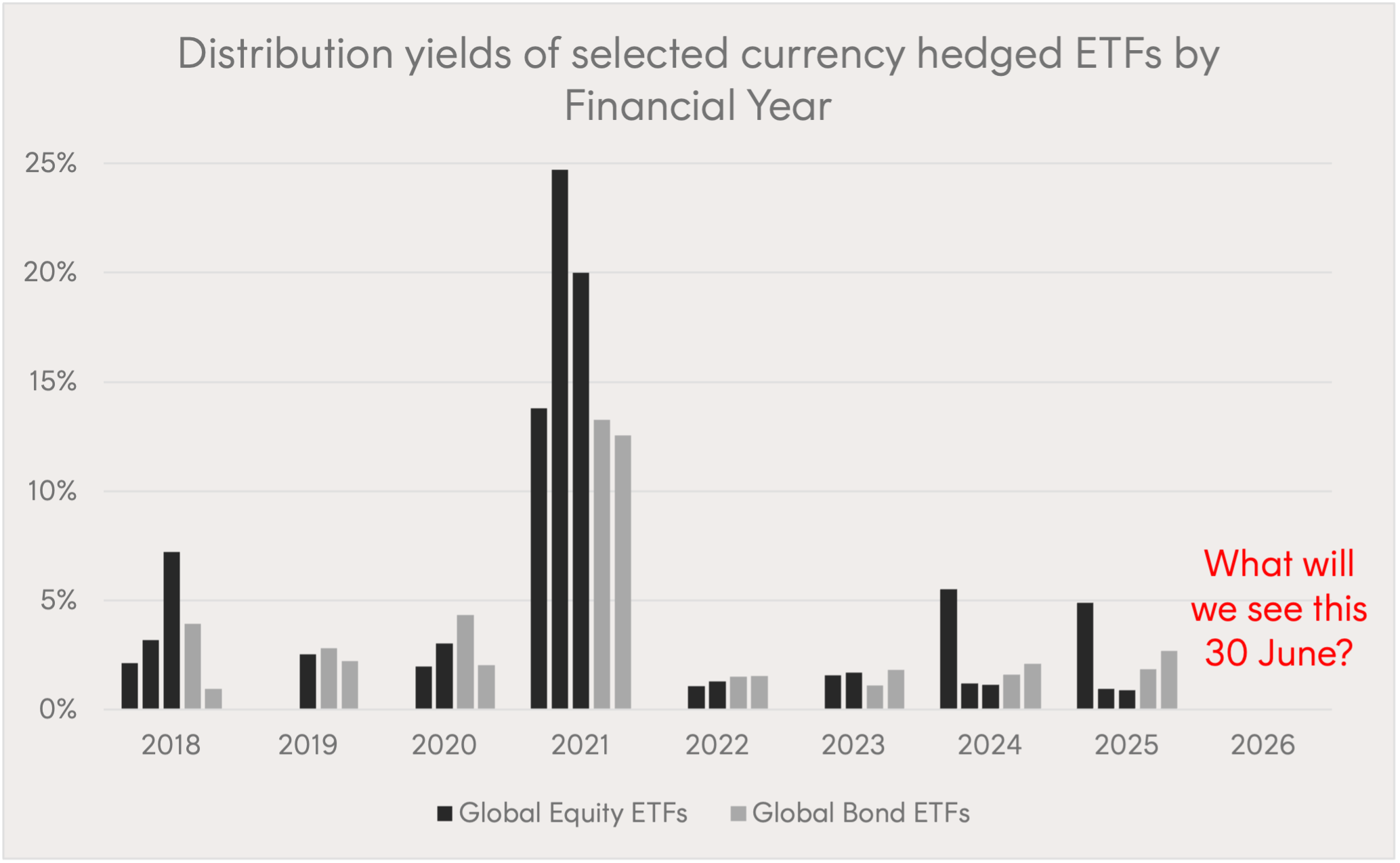

In the 2021 tax year the AUD appreciated, creating large income distributions for a number of currency hedged funds that had not elected into the Taxation of Financial Arrangements framework (or TOFA, for short). This is illustrated in the annual distribution yields of three selected global equity ETFs and two global bond ETFs (all currency hedged) shown in the chart below.

Source: Bloomberg, as at June 2026. Past performance is not an indicator of future performance. Yield may vary at the time of investment.

For an explainer on TOFA and previous coverage on the implications of TOFA and currency hedging, please see here and here. But in summary, where a fund has not been elected into TOFA any profits on hedging activity are characterised as income, which is a mismatch from the assets being hedged and creates tax implications for investors on an ongoing basis.

While the large 2021 distributions might have been inconvenient for investors, the real damage was the amount of tax most investors would have had to pay for that tax year. The double whammy: the ETFs shown above did not appear to take advantage of the AMIT framework to significantly reduce the cash distributed. In some cases, this meant selling down part of the underlying share portfolio to fund the payout, crystallising significant capital gains on top of the taxable income.

The irony for these investors was that they made the right call to be currency hedged in 2021, but the tax consequences of inefficiently structured currency hedged funds eroded much of the benefits of being hedged in the first place.

Concerns around TOFA hedging dissipated over 2022 to 2025, in the absence of hedging gains.

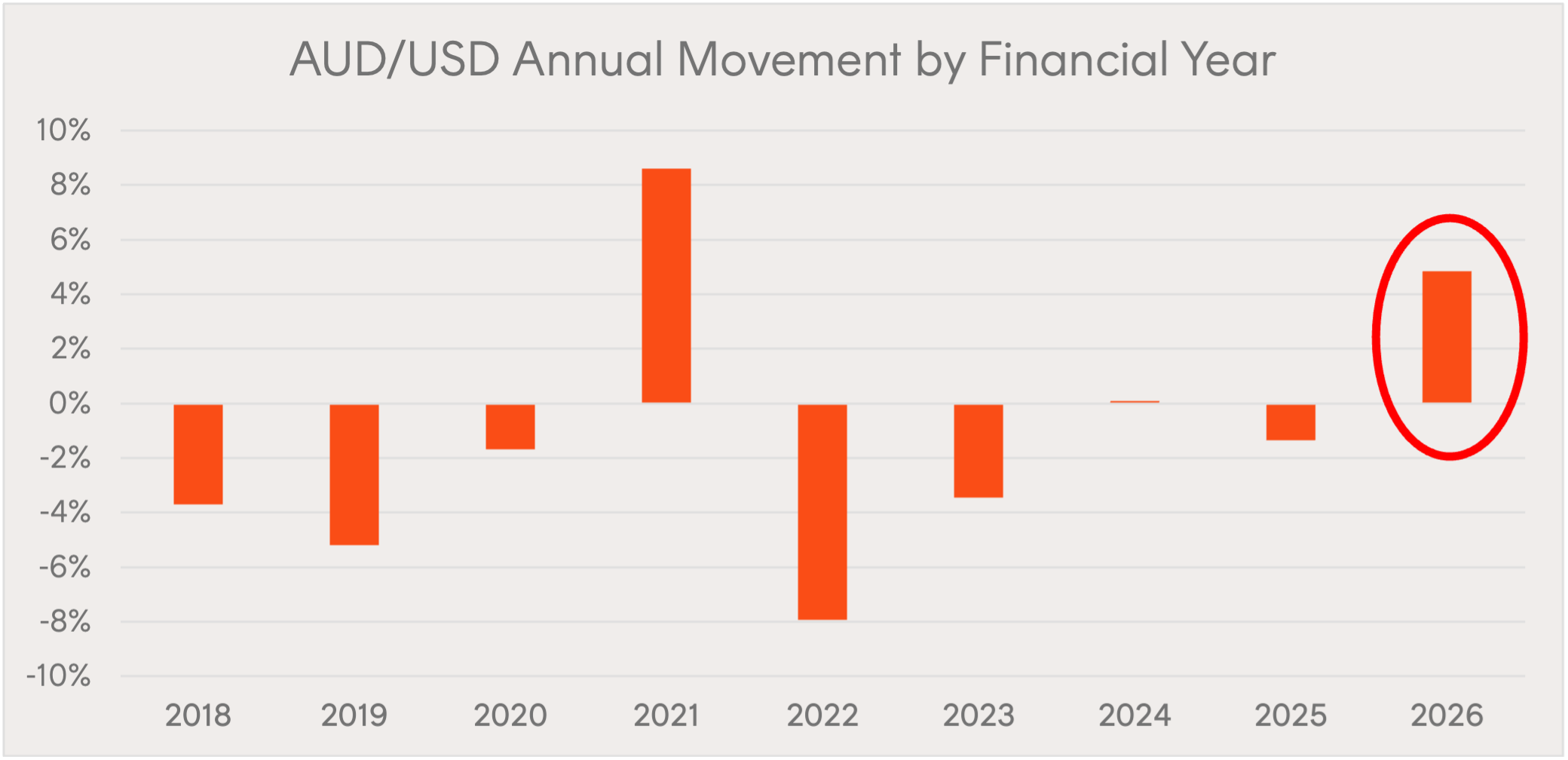

Source: Bloomberg, as at 2 June 2026. 2026 annual movement is up to 2 June 2026, rather than a full year figure. Past performance is not an indicator of future performance.

Five years on, the 2026 tax year looks like it will be the first tax year since 2021 where we are on track for the AUD to appreciate against the USD.

What can we expect in terms of 2026 June distributions and tax consequences?

As at the time of writing, there still appears to have been no TOFA election made for most of the selected ETFs highlighted in the first chart above. The managers of these ETFs may rely on the AMIT provisions, such that we do not see the same dramatic spike in cash distributions, reducing the realised capital gains. However, it doesn’t avoid the core issue: if there are hedging profits, there may be an associated income tax obligation for investors in those funds for the 2026 tax year, depending investor circumstances.

It is worth noting that one of the ETFs highlighted above has now been elected into TOFA, effective 1 July 2024. What that means practically is that TOFA will apply only to the proportion of the portfolio purchased on or after 1 July 2024. But given the very low turnover that is typical of index funds it is likely that a substantial portion of any hedging profits will still be taxable at the end of 2026 on income account.

If instead TOFA applied to 100% of the portfolio of these ETFs, then:

1. The 2026 hedging gains would not be taxable this year, but rather only when the underlying portfolio assets are sold. Index-tracking equity ETFs typically have turnover of 5-10% pa, making the average portfolio asset holding period 10-20 years.

2. The tax characterisation of the hedging gains switches from income to capital. This is intended to provide better matching (currency hedging is intended to produce gains when the AUD appreciates and erodes the value of A foreign asset in AUD terms) and generally means investors pay less tax due to either the CGT discount or indexation.

Deferring and lowering the ongoing tax drag of any investment allows unit holders to have more money in the market to take advantage of compounding. Minimising tax drag can be as important as minimising fees and costs for net (after-tax) performance.

At this stage it’s difficult to say how significant the tax consequences will be for investors in funds that need to recognise some or all of their 2026 hedging gains on income account. There are a few swing factors that might increase or decrease the taxable income for each fund, for example the timing and magnitude of applications and redemptions relative to hedging profits. The final impact will only be revealed on their 2026 distribution tax statements.

Currency hedging without the potential tax drag

Rather than facing high variability of distributions and tax consequences, there are alternatives for investors seeking currency hedged exposure to global shares or global bonds. For example:

These are core global asset class building blocks specifically designed for Australian investors seeking tax-efficient investment outcomes. Betashares made a TOFA hedging election when these funds were initially established, meaning TOFA treatment applies to their entire portfolio.

Of course, the overall investor outcomes are driven by more than just tax. Other important considerations include fees and costs and the risk and return of an investment strategy.

If you had any questions about TOFA elections please reach out to your respective BDM or to [email protected].

There are risks associated with an investment in the Funds. An investment in the Funds should only be considered as a part of a broader portfolio, taking into account an investor’s particular circumstances, including an investor’s tolerance for risk. For more information on risks and other features of the Funds, please see the Product Disclosure Statement and Target Market Determination, both available on www.betashares.com.au.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

This article does not constitute tax advice. The tax treatment described is general in nature, may be based on the current law and Betashares’ interpretation of it, and may not apply to your particular circumstances. Tax outcomes depend on individual circumstances and may change. Investors should seek professional tax advice specific to their situation before making any investment decision.

This material may contain forward-looking statements. These statements reflect current expectations based on information available at the time of writing.

1. As at 2 June 2026.