David Bassanese

6 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

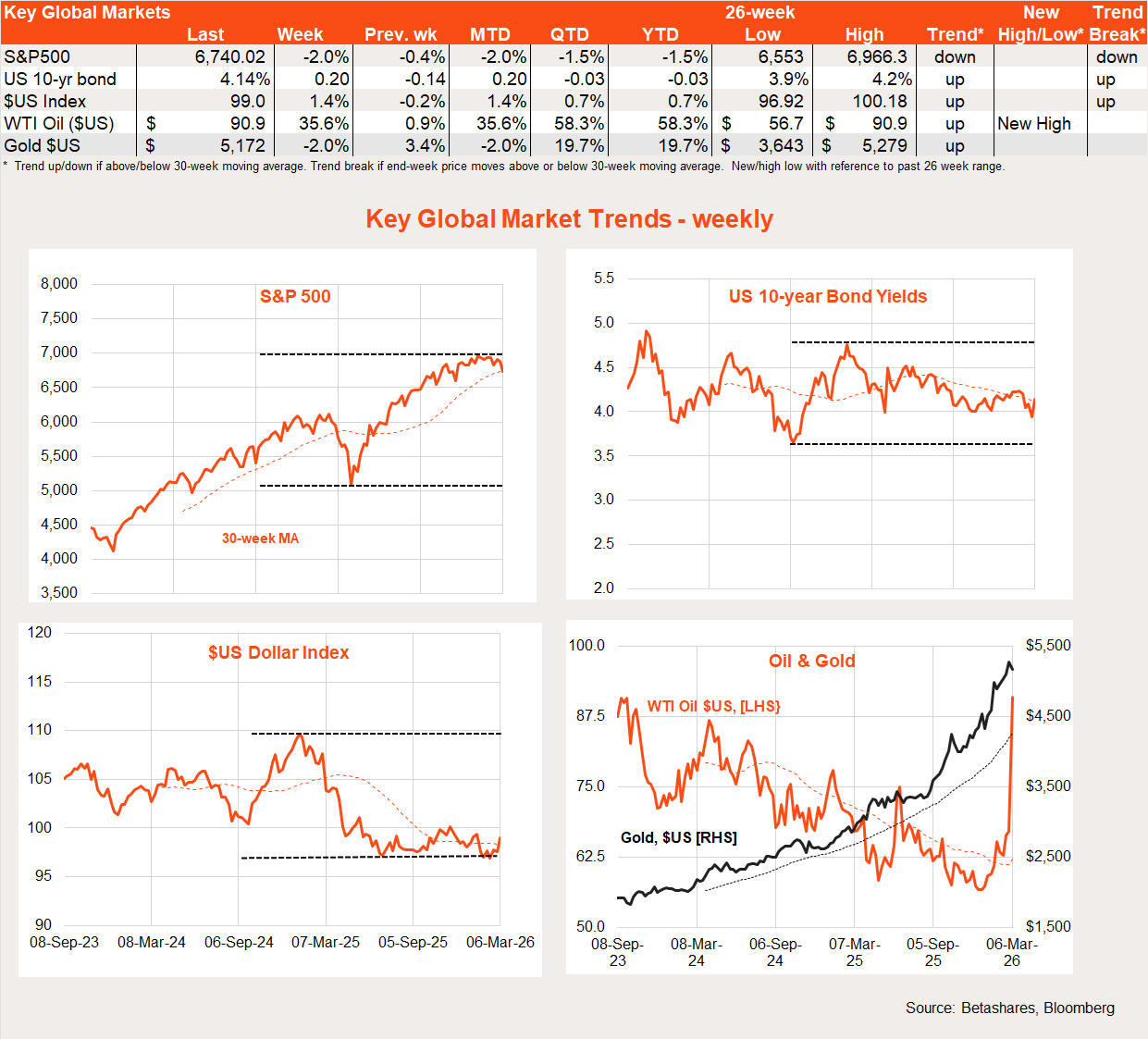

Global stocks slumped last week, reflecting the surge in oil prices due to the Middle East conflict.

Global week in review: Iran digs in

Global stocks understandably slumped last week as the ongoing war in the Middle East led to a 35% surge in crude oil prices. Lacking boots on the ground, US and Israeli missile strikes appear unable to easily dislodge the Iranian regime – which, so far at least, is digging in.

At time of writing, WTI oil prices surged a further 16% in today’s morning trade, reaching $US106 a barrel. The S&P/ASX 200 was down 3% in early Monday morning trade.

Perhaps most importantly last week, the Iranian regime was effectively able to scare off most oil freighters from using the Strait of Hormuz, through which 20% of global oil trade flows. Unable to ship its product and with storage tanks filling up fast, several Middle Eastern countries are winding down oil production. Drone and missile attacks on oil refineries have only added to the risk. The longer this war drags on, the larger the upside risk to oil prices, and presumably the greater the pressure on Trump to try to strike a deal.

Also of note was that bond yields rose around the world rather than fell, with investors fearing the upside inflation risk from higher oil prices rather than the downside risks to economic growth. In the US, 10-year bond yields rose 0.2% to 4.14% as investors all but fully priced out one of the two Fed rate cuts expected this year. Along with safe haven flows, this shift in policy expectation also pushed up the US dollar, which in turn hurt gold prices and the Australian dollar.

Indeed, across markets, it is notable that some of the more popular trades of late – namely non-US markets, gold and value sectors such as materials – have slumped the most, suggesting investors are hunkering down and raising cash.

Other US economic news was mixed. The services sector PMI index was surprisingly robust in February, suggesting the overall economy continues to tick along well. offsetting this was Friday’s surprise 92k slump in February employment, although a strike in the health care sector and blizzard conditions seem partly to blame.

Global week ahead: Iran & inflation

The coming week will again be dominated by the Iran conflict. Who will blink first, and will it happen as early as this week? I suspect the resilience of the Iranian regime in the face of heavy attacks has surprised the US, but whether it can continue to hold out remains to be seen. The longer it can, the greater the pressure on Trump to ‘do a Greenland’ – i.e. claim victory and walk away.

The second most important point of interest this week will now be two US reports on inflation – the consumer price index (CPI) and the private consumption expenditure deflator (PCED). Annual growth in the core CPI is expected to hold steady at 2.5% – which excluding tariff effects – is probably closer to the Fed’s target of 2% (thanks in large part to easing housing inflation). Annual growth in the Fed’s preferred measure of underlying inflation (core PCED) will likely be less pleasing. Core PCED is expected to tick up to 3.1% from 3.0%. The PCED is currently running higher than the CPI due to its lower weight to housing.

Also on Friday will be an update on US labour demand, with job openings data. We also get the consumer sentiment report which has staged a mini-recovery in recent months but is still wallowing at low levels.

Global equity trends: the great rotation continues

The MSCI All-Country World Equity Index dropped 3.2% last week, modestly underperforming the S&P 500’s drop of 2.0%. As noted above, position squaring likely accounts for heavier falls among recent popular trades – and does not necessarily suggest a shift in the underlying trends.

Since the end of October 2025, we’ve seen underperformance of US/growth/technology, replaced by strength in Japan, emerging markets and small caps. There are also tentative signs of a bottoming out in the underperformance of the Australian market. Despite the US tech sector’s underperformance, global quality (among factors) is also holding up reasonably well.

As we saw in 2022, if a global energy shock plays out, there may be a further rotation from interest rate-sensitive cyclical and technology sectors into more value-orientated defensives and resources.

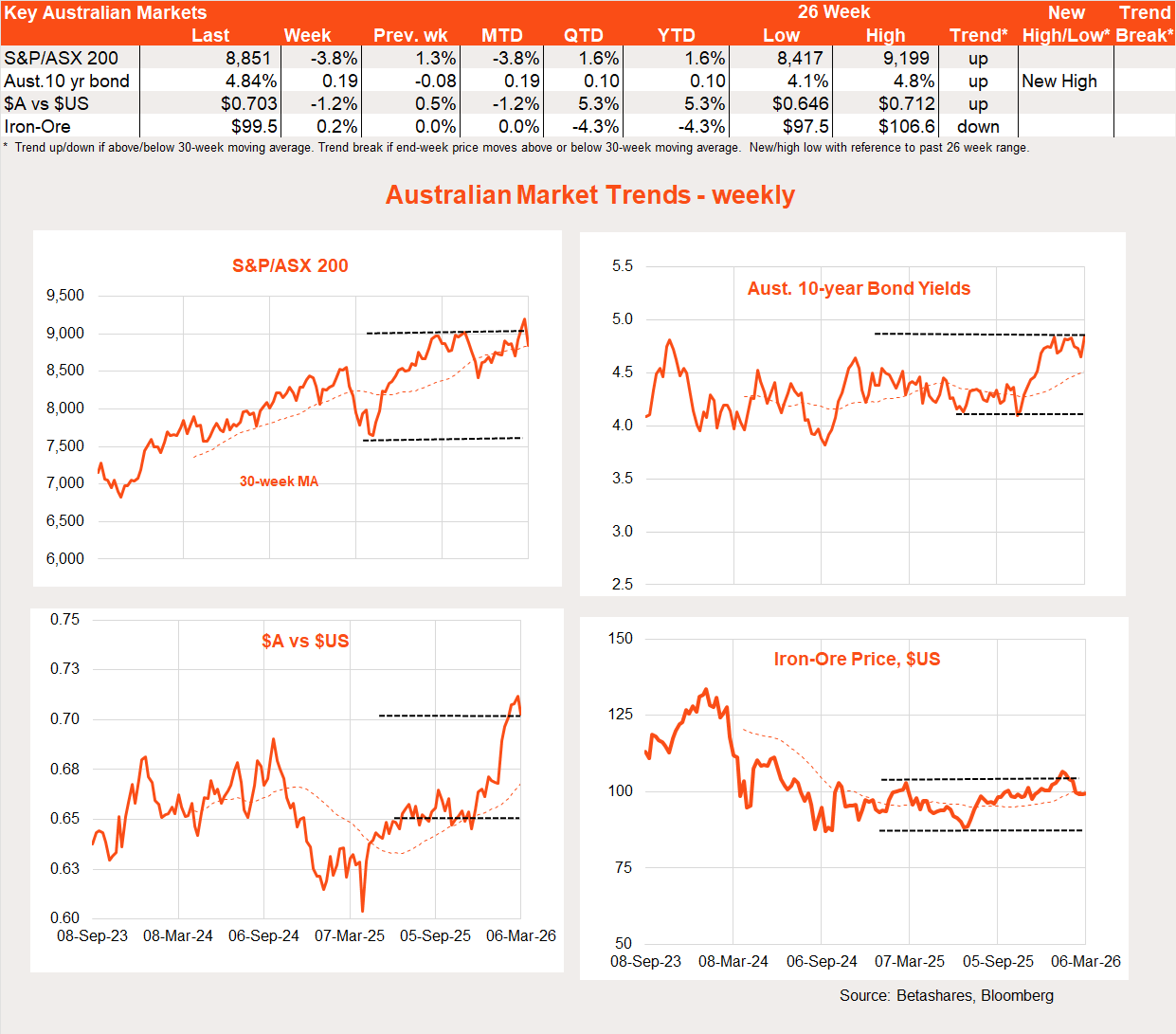

Australian week in review: still firm employment

The major local highlight last week was the firm 0.8% gain in Q4 GDP, which – along with hawkish commentary from RBA Governor Michele Bullock – increased fears of another near term rate hike.

Contrary to market opinion, my take on the GDP report was less hawkish. Despite a solid production gain, overall domestic demand slowed notably from 1.3% in Q3 to 0.5% in Q4. Consumer spending rose a measly 0.3%, and even allowing for the drag from electricity subsidies, was probably still only 0.5%. Of course, it’s also likely that a lot of spending on cigarettes is not being recorded, given so much now takes place on the black market.

RBA Governor Bullock also chimed in last week, reminding us there’s a policy meeting this month which should be considered ‘live’. My base case is that the RBA will again pull the rate hike trigger, although not until May after the Q1 CPI report in late April. Having said this, I guess a move this month can now no longer be ruled out.

Australian week ahead: sentiment in focus

Local highlights this week will be NAB and Westpac measures of business and consumer sentiment respectively. Both will likely be under pressure from interest rate fears – although may not yet reflect the added drag from the Iran war.

Australian equity trends

Materials were the big loser on the Australian market last week, declining 7.4% while the energy sector surged 9.0%. Even technology bounced last week, rising 3.3%.

Given position squaring, the Iran war will naturally play havoc with recent trends over the short run – although energy stocks are a clear winner for now.

Have a great week!