Key points

The SaaSpocalypse selloff

Earlier this year, the release of autonomous AI tools saw billions of dollars wiped out across the software sector. In what was dubbed ‘SaaSpocalypse’, the broad-based selloff priced that this industry would be most at risk to AI disruption.

If these new agentic tools can autonomously execute complex workflows and allow anyone to build working software prototypes in a short period of time, then what valuation should investors ascribe?

While overdone, sharp selloffs during periods of structural disruption are not uncommon as markets reprice the sector first before later differentiating between the winners and losers.

Why cybersecurity is different

One of the areas within software that we view as winners are global cybersecurity companies with strong moats built around deep proprietary networks.

Despite the release of several frontier AI models, vibe-coded solutions simply cannot replace incumbent solutions provided by leading security companies such as CrowdStrike (CRWD) and Palo Alto Networks (PANW) overnight.

That’s because these companies have spent years consolidating dozens of point solutions into unified platforms that ingest telemetry across millions of networks and endpoints in real time. It is this depth of data that trains the detection models and makes the platforms increasingly difficult to replicate.

When overlaid with AI, the same technology that enables more sophisticated attacks also enables these platform offerings as defensive solutions; automating threat detection, accelerating response times and identifying vulnerabilities before they can be exploited. Markets appear to be reflecting this shift in narrative away from ‘AI is eating software’s lunch’ to ‘AI is additive to software’ with many cybersecurity stocks having re-rated sharply.

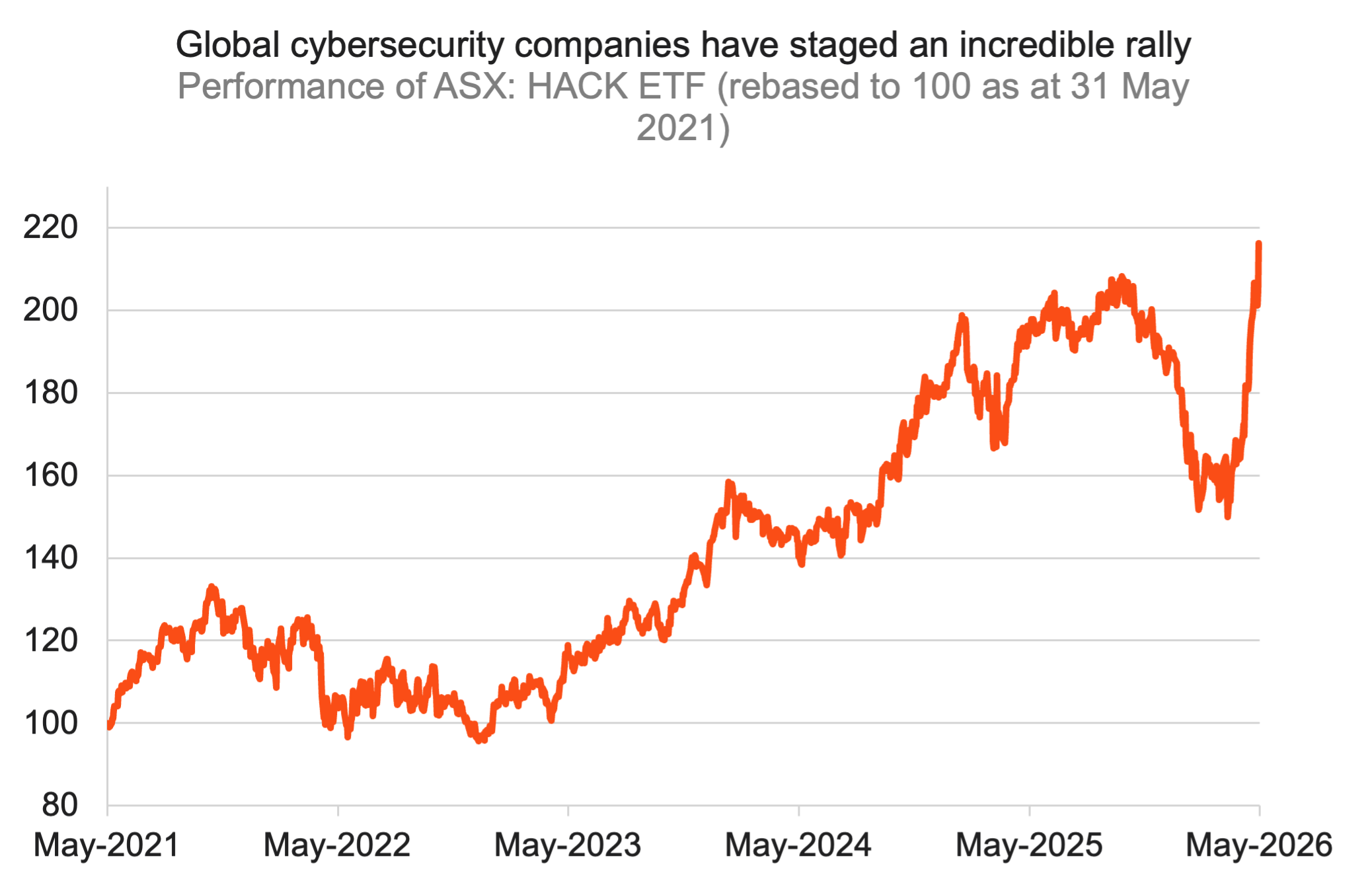

For example, the Betashares Global Cybersecurity ETF (ASX: HACK) is up 31%1 since April 7, 2026, when Claude Mythos Preview was launched – an unreleased frontier AI model by Anthropic able to discover and exploit vulnerabilities across major operating systems and browsers. Since inception on 30 August 2016, HACK returned 18.01%.2

Source: Bloomberg. As at 31 May 2026. Past performance is not an indicator of future performance.

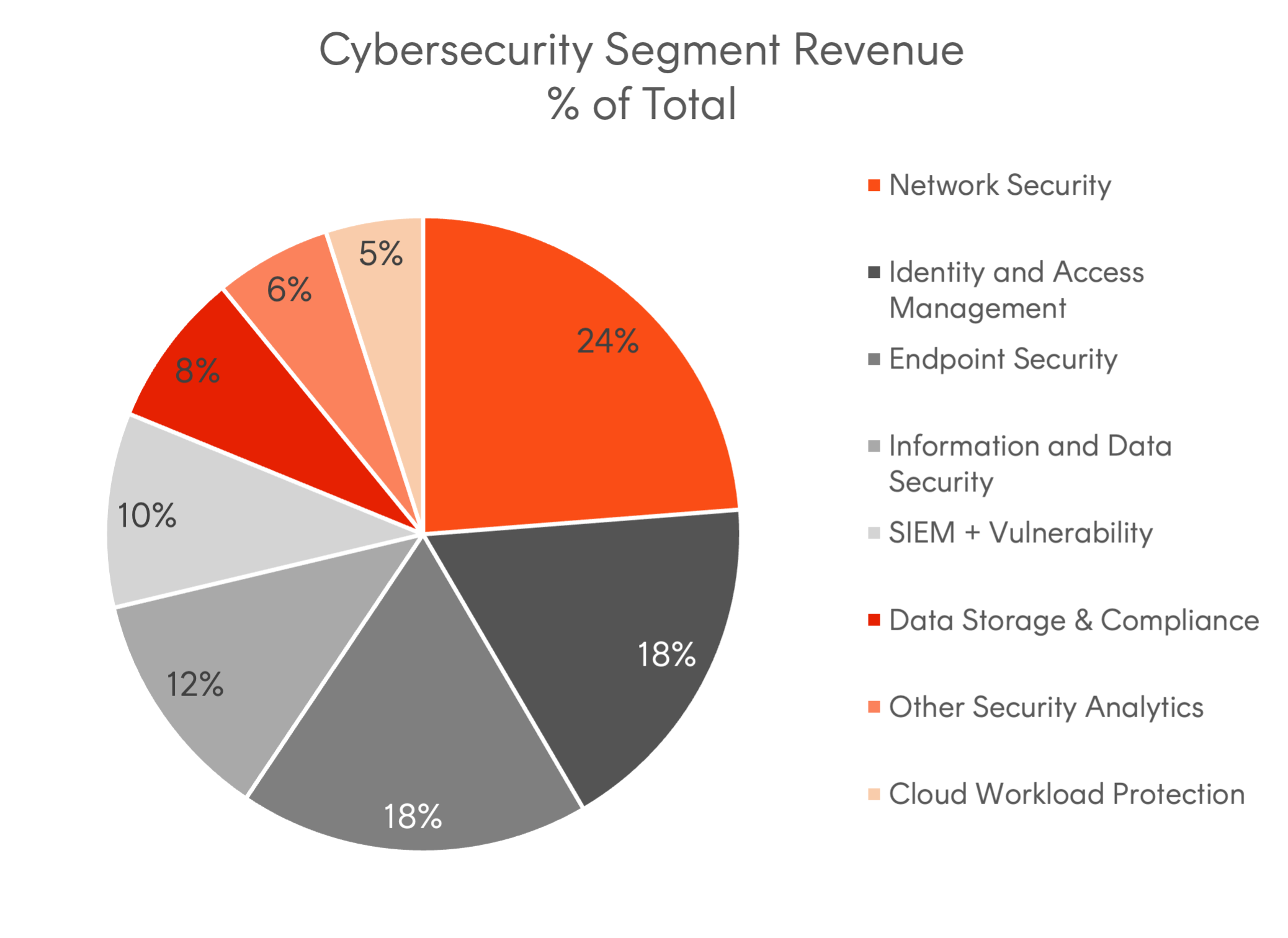

Initially viewed as a threat to existing cybersecurity business models, its impact is relatively narrow in scope given vulnerability assessment and SIEM-related functions are segments that account for just ~10% of the broader cybersecurity market.

Source: Bloomberg. Cybersecurity Segment Revenue 2026E.

What is the outlook from here?

While some may argue the rally reflects momentum rather than fundamentals, there have been recent earnings results from the major security players that may give more substance.

In the first week of June, both Palo Alto Networks and CrowdStrike delivered better than expected earnings for their respective quarterly updates. Both pointed to the rise of frontier AI capabilities as a key driver of heightened customer demand.

Palo Alto Networks delivered a strong beat in its fiscal Q3 2026, with revenue growing 31% year-on-year to US$3.0bn as demand for AI-driven security accelerated. The standout was Next-Generation Security Annual Recurring Revenue (ARR), which surged 60% to US$8.13bn.

CrowdStrike also topped expectations in its fiscal Q1 2027, with revenue up 26% to US$1.39bn and ARR crossing US$5.5bn. Net new ARR hit a record US$256m as platform adoption deepened, prompting management to raise full-year growth guidance. CEO George Kurtz framed the quarter as a turning point, describing the convergence of frontier AI and cybersecurity as a structural tailwind for the business.

These two companies are key holdings in HACK, in addition to Fortinet (FTNT) whose share price is up over 80% at the time of writing driven by product revenue growth of 41% year-over-year3 as enterprises upgraded to their next-generation firewalls.

Clearly, the fundamental outlook is intact and indeed the Nasdaq Consumer Technology Association Cybersecurity Index (the index that HACK seeks to track) is forecast to deliver earnings growth of approximately 14.1% over the next 12 months.4

Moreover, the longer-term structural tailwinds that have made cybersecurity a popular investment theme in the first place may be here to stay.

Geopolitical tensions continue to define markets, and the rise of advanced AI threat tactics like prompt injection attacks mean the need for robust security solutions on the defensive side has never been more important.

For more information on the Betashares Global Cybersecurity ETF (ASX: HACK), click here.

There are risks associated with an investment in HACK, including market risk, cybersecurity companies risk, concentration risk and currency risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your client’s particular circumstances, including their tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available at www.betashares.com.au. No assurance is given that any of the companies in a Fund’s portfolio will remain in the portfolio or will be profitable investments.

1. Source: Bloomberg. As at 31 May 2026.

2. Source: Betashares. As at 29 May 2026.

3. https://investor.fortinet.com/static-files/9dc7117a-d2dc-4d9f-b151-c2eea950a0e4

4. Source: Bloomberg. As at 4 June 2026.