Southern route

Tom Wickenden

7 minutes reading time

- Sector & regions

Related articles

Financial intermediary use only. Not for distribution to retail clients.

Japanese equities entered a one-day bear market to start August as a Bank of Japan (BoJ) rate hike played a part in triggering a global equity market sell off (our portfolio management desk discussed this episode in detail here).

The sell off came on the back of a 3-year period in which the Japanese Topix was the best performing major equity market in the world.

At this pivotal moment investors are questioning whether the Japanese structural growth story is real, or simply a function of Japanese Yen weakness.

In this note we explain why we believe there is a long-term case for currency hedged Japanese equities in a diversified global portfolio, even in the face of an appreciated Yen.

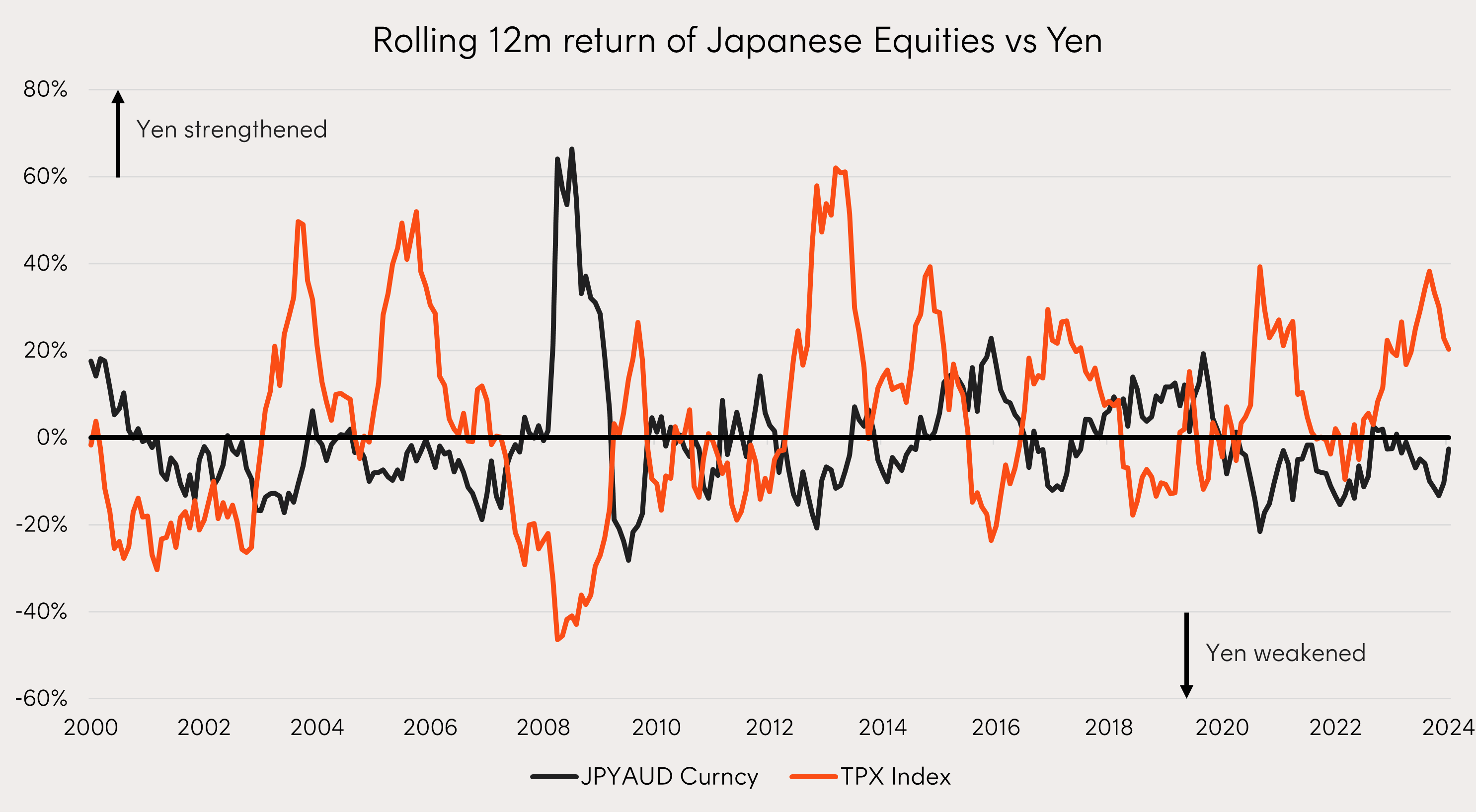

Are Japanese equities simply a function of their currency?

Japanese equities have historically been inversely correlated to the Yen – performing well when the currency is weakening.

Deflation, low growth, and cash hoarding headlined a list of issues for Japan Inc. as the economy underwent multi-decade structural changes following the 1990’s crash.

During this period, it was the Yen that had the largest influences on Japanese equity performance. A weaker Yen boosted the exporter driven economy’s competitiveness and earnings while an appreciated Yen had the opposite effect.

Source: Bloomberg. July 2000 to July 2024. Depicts index performance of the Japanese’ Topix Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Slightly more than half of Japanese equities revenue is currently earned offshore. This is unsurprising, given Japan Inc has produced global leaders like Toyota, Sony, Daikin, Fast Fashion (Uniqlo), Fanuc and Tokyo Electron. With rising geopolitical tensions Japan Inc’s leadership in high tech manufacturing and robotics makes it an important ‘friendshoring’ partner.

A strong argument therefore remains that if an investor is very bullish on the Yen, they should probably not be as bullish on Japanese equities.

However, there is much more behind the investment case for Japanese equities today than just Yen weakness.

The turnaround story of Japan Inc.

Decades of deleveraging has put more cash in the hands of Japanese corporates and successful reforms are now putting this cash back in the hands of investors.

Low interest rates in 1980’s Japan led to a vicious leverage cycle pushing asset prices to unimaginable levels. Ultimately when the economy came crashing down in the 1990’s a massive deleveraging cycle began.

Fast forward two decades and Japanese corporations found themselves with some of the largest cash balances in the world – a collective US$4.8 trillion in 2019 – hoarding cash to avoid the calamities of the 90’s. Free of net debt interest payments Japanese companies also saw profitability grow rapidly. However, not enough was being returned to shareholders. This has begun to change.

Reforms dating back to 2015 sought a shift in Japanese corporate leadership to usher in a new generation of more shareholder-friendly policies. This sentiment has continued, as recently as last year the Tokyo Stock Exchange (TSE) threatened delisting of corporations hoarding cash, leaving their price to book ratios below 1x, if they didn’t get their act together by 2026.

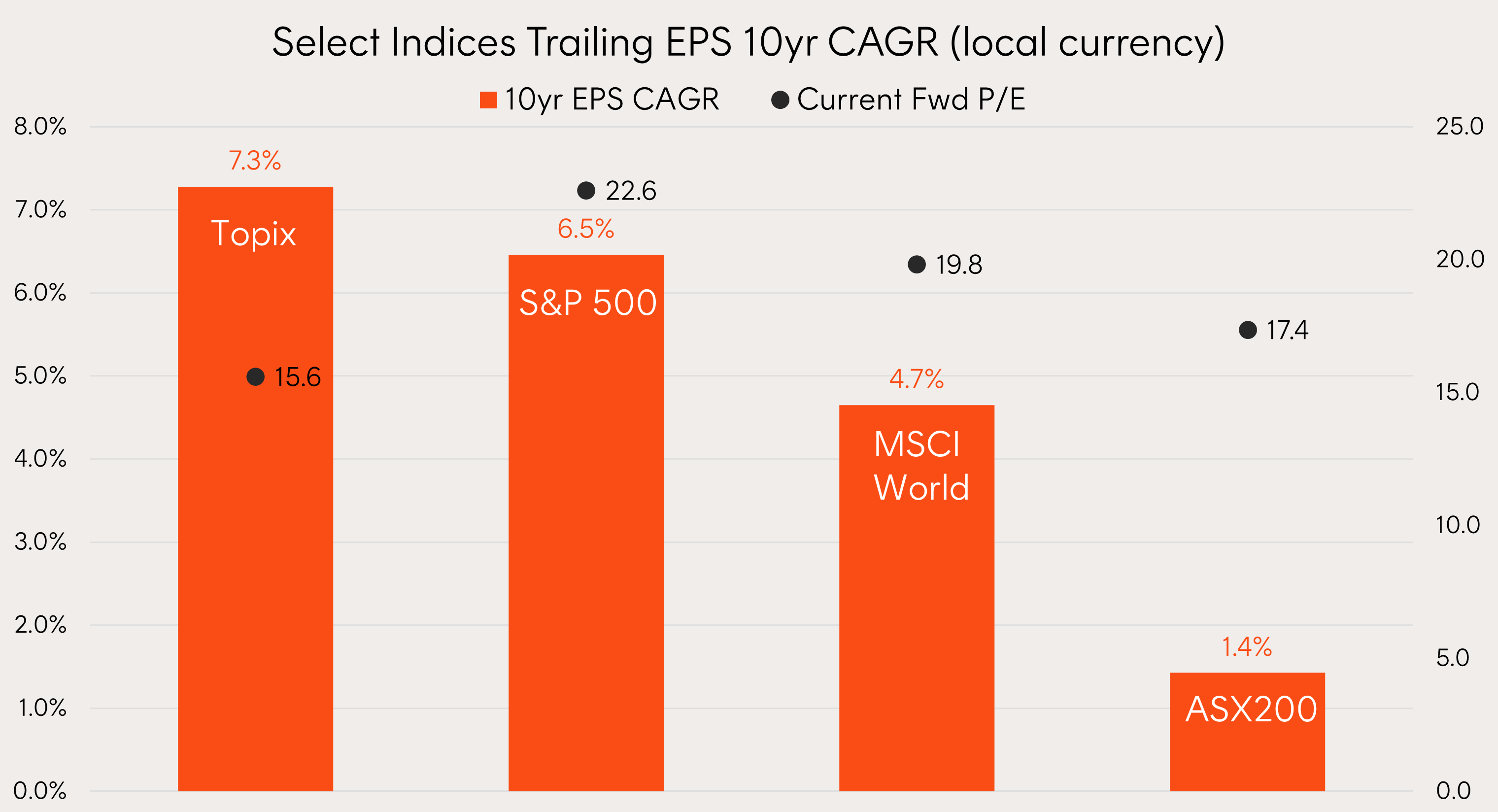

Source: Bloomberg. As at 28 June 2024. You cannot invest directly in an index.

The success of these reforms have started to be seen through:

- Four consecutive years of record share buybacks. 2024 has already seen US$57b announced to May equating to ~1/5th of Japan’s fiscal year corporate profits and already nearing the full year record set in 23’,1

- 10% p.a. dividend growth over the past decade,2

- A 20% drop in the number of listed companies trading below a 1x price to book ratio since the TSE threat – this figure still sits above 40% compared to 9% for the S&P500,3

- The highest level of EPS growth globally, 7.3% CAGR, over the past 10-years (in local currency terms),4

Japanese corporations have shifted to more closely resemble a distinctly investor friendly US approach which is seen as the gold standard for shareholder returns.

This shift in Japanese corporate governance, which still has a long way to play out, may allow Japanese equities to continue to perform well even in the face of an appreciated Yen.

Understanding the currency hedging question for Japanese equities

An important question for Australian investors looking to Japanese equities is whether to currency hedge. Over the past decade, a currency hedged approach has outperformed significantly due to the depreciation of the Yen and the often-lesser appreciated benefit of carry.

Even after the BoJ’s recent hike, the current interest rate differential between Australian and Japan provides +460 bps p.a. of ‘carry’ (positive returns) for currency hedged investors.

The BoJ understands a weak yen is good for their export oriented economy, hence they may be likely to take a cautious approach to any further hikes. Much of Japan’s recent higher inflation was ‘imported’, and with inflation falling elsewhere around the globe and market pricing of inflation expectations benign, the inflation outlook looks contained.

If we consider a more ‘normalised’ interest rate differential between Australian and Japan may be something close to 200bps, this would still result in a 2% p.a.5 benefit to currency hedged investors from carry.

With uncertainty around what a normalised Yen exchange rate will be for the future, the interest rate carry buffer provides investors an incentive to take currency uncertainty out of the Japanese equation and take a hedged approach to investing (particularly if the Yen depreciates further).

Portfolio implementation

With an investment approach favouring Japanese exporters and currency hedging its exposure, Betashares HJPN seeks to benefit from the relatively weak Japanese Yen and structurally lower interest rates in the Japanese economy. These thoughtful elements in HJPN’s index construction have factored into it being the best performing Japanese equities fund (ETF or managed fund) in Australia over all timeframes since common inception and outperforming the Topix index (in AUD terms) by 10% p.a. over a 5-year period.6

For more information on HJPN please reach out, I would be very happy to book in a meeting with our investment team to explore how it could fit in your portfolios. You can also visit the fund page here.

Future results are inherently uncertain. The information above may include opinions, views, estimates, projections, assumptions and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in such forward-looking statements. Forward-looking statements are based on certain assumptions which may not be correct. You should therefore not place undue reliance on such statements. Betashares does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date such statements are made or to reflect the occurrence of unanticipated events.

There are risks associated with an investment in HJPN, including market risk and country risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

Sources:

1. Nikkei, as at 30 May 2024.

2. Bloomberg, as at 28 June 2024

3. Man institute research, April 2024.

4. Morgan Stanley Research, Datastream, MSCI. Note EPS calculated in local currency. Based on MSCI indices.

5. The carry is based on the interest rate differential between the two economies. At the date of this article the RBA’s estimated neutral rate is 3.50%. The BoJ does not issue an official estimate of the neutral rate, however, estimates generally put this in the range of 1% to 1.5%. Actual results may differ materially.

6. Bloomberg. As at 28 June 2024. Past performance is not an indicator of future performance.

Explore

Markets