David Bassanese

4 minutes reading time

Due to the war in Iran, the usual Market Trends report has been suspended this month in favour of a more abbreviated format that focuses on market developments over the past month.

The outlook for investment markets obviously remains highly dependent on events in Iran over the next few weeks – with usual economic and market fundamentals taking a back seat.

Major asset class performance

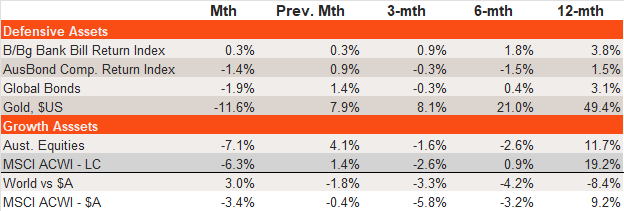

Global equities slumped in March reflecting the commencement of military hostilities in Iran. The MSCI All-Country World Index declined 6.3% in local currency terms, although only 3.4% in Australian dollar terms due to weakness in the Australian dollar. Against the US dollar, the Australian dollar slipped from US71.2c to US69.0c.

Australian equities also declined, with returns on the S&P/ASX 200 Index down 7.1% for the month.

A 50% surge in oil prices also heightened inflation risks, which led to higher global bond yields and weakness in fixed income markets. Global and Australian benchmark bond indices declined by 1.9% and 1.4% respectively.

Gold prices also weakened, with the US dollar price down by 11.6% over the month. This likely reflected profit taking and investor needs to raise cash – along with reports of some central bank selling to help support their currencies.

Source: Bloomberg, Betashares. Cash: Bloomberg Australian Bank Bill Index; Australian Bonds: Bloomberg AusBond Composite Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged); Gold: Spot Gold Price in $US; Australian Equities: S&P/ASX 200 Index; Global Equities: MSCI All-Country World Index in local currency and $A currency (unhedged) terms. Past performance is not indicative of future performance.

Pre-war market outlook

The global economy and financial markets entered 2026 on a reasonably solid footing, with resilient economic growth and broadly contained inflation.

Most central banks (with some exceptions, such as the RBA) retained a neutral to easing policy bias. The corporate profit outlook remained strong, underpinned by continued solid performance among large-cap US technology companies.

This outlook favoured continued positive returns from both global equities and bonds.

The major pre-war issue globally was the artificial intelligence (AI) boom, and whether this was becoming more of a headwind for markets – due to fears of disruption, excessive valuations and over-investment – compared to the earlier euphoria following the release of ChatGPT in late 2022.

Associated with these concerns were signs of a ‘great rotation’ by investors away from US technology companies and into cheaper non-US exposures, such as Japan and emerging markets.

In Australia, a solid rebound in corporate earnings expectations – reflecting firm global commodity prices and improving local economic growth – has been counterbalanced by a rise in interest rate fears, with the Reserve Bank shifting to a tightening policy bias due to the rebound in inflation.

Implications of the war: an eventual TACO?

The Iran war has suspended many of the above concerns, although it has heightened fears that the RBA will need to hike interest rates even more aggressively due to the added upside inflation risks. My base case remains the RBA will hike rates only once more in May, following the release of another uncomfortably high quarterly inflation report in late April.

But globally, the main new fear is stagflation (higher inflation and weaker economic growth) associated with the surge in oil prices. Whether these fears materialise depends critically on how long the Iran war lasts and whether there is serious damage to oil production facilities.

My sense is that the US began these attacks in the expectation of a speedy victory and possible regime change – it did not want to become entrenched in a war that would lead to a surge in oil prices and the risk of US recession. It did not anticipate Iranian resistance and the effective blockade of the Strait of Hormuz. Accordingly, US President Donald Trump is looking for a face-saving exit – though the challenging fact is that Iran, so far at least, has not afforded him that opportunity. Importantly, there has been no serious damage to Middle East oil production facilities (as of writing) and only a blockade of oil flow through the Strait.

As of 8 April 2026, we’ve now reached the point where both sides have at least formally agreed to talk. A two week ceasefire is in place and Iran has agreed to open the Strait of Hormuz during this time. One way or another, my judgement is a deal will be reached and conditions will gradually get better rather than become a lot worse. This should ultimately lead investors to refocus on the pre-war market concerns and opportunities note above – but we are not there yet.