David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

Global stocks remained under pressure last week as the Iran war continued.

Global week in review: escalating attacks

The Iran war continued last week, with US President Donald Trump alternating between escalation and attempts at de-escalation. At times, he suggested operations could be wound down shortly, but at others he intensified threats.

Iran also sought to drive a wedge between the US and its allies by promising safe passage through the Strait of Hormuz for ships bound for China, India and, by week’s end, Japan. The US, meanwhile, attempted to limit oil price upside by easing restrictions on the sale of Russian and Iranian (yes, Iranian!) oil.

One worrying new development last week was attacks on energy infrastructure. Israel attacked one of Iran’s major LNG processing facilities, leading Iran to retaliate with an attack on a neighbouring plant in Qatar. The week ended with Trump issuing an ultimatum that the US would attack Iran’s electricity infrastructure if it did not fully open the Strait of Hormuz within 48 hours. Iran responded by warning it would attack energy and water infrastructure across the region if the US did so.

It’s a Middle East form of MAD: mutually assured destruction. The clock is ticking and the deadline ends Tuesday 1:14 am (Sydney time).

In other news, the Fed last week left rates firmly on hold and marginally lifted its inflation forecasts due to the recent rise in energy prices. Markets have all but priced out the hope of US rate cuts this year.

Global week ahead: Iran deadline

The coming week will again be dominated by the Iran conflict. With Trump’s deadline due to expire tonight Australia time, tensions are clearly running high. There is a very real risk of a major surge in risk-off sentiment, as hopes for a Trump TACO moment seemingly fade.

Attacks on energy infrastructure and/or further signs the US is considering “boots on the ground” could see oil prices soar, which would hurt both equity and bond markets. Due to US dollar strength and likely forced liquidation trades, gold is not proving to be a safe haven in these troubled times, with the US dollar price down 10% last week.

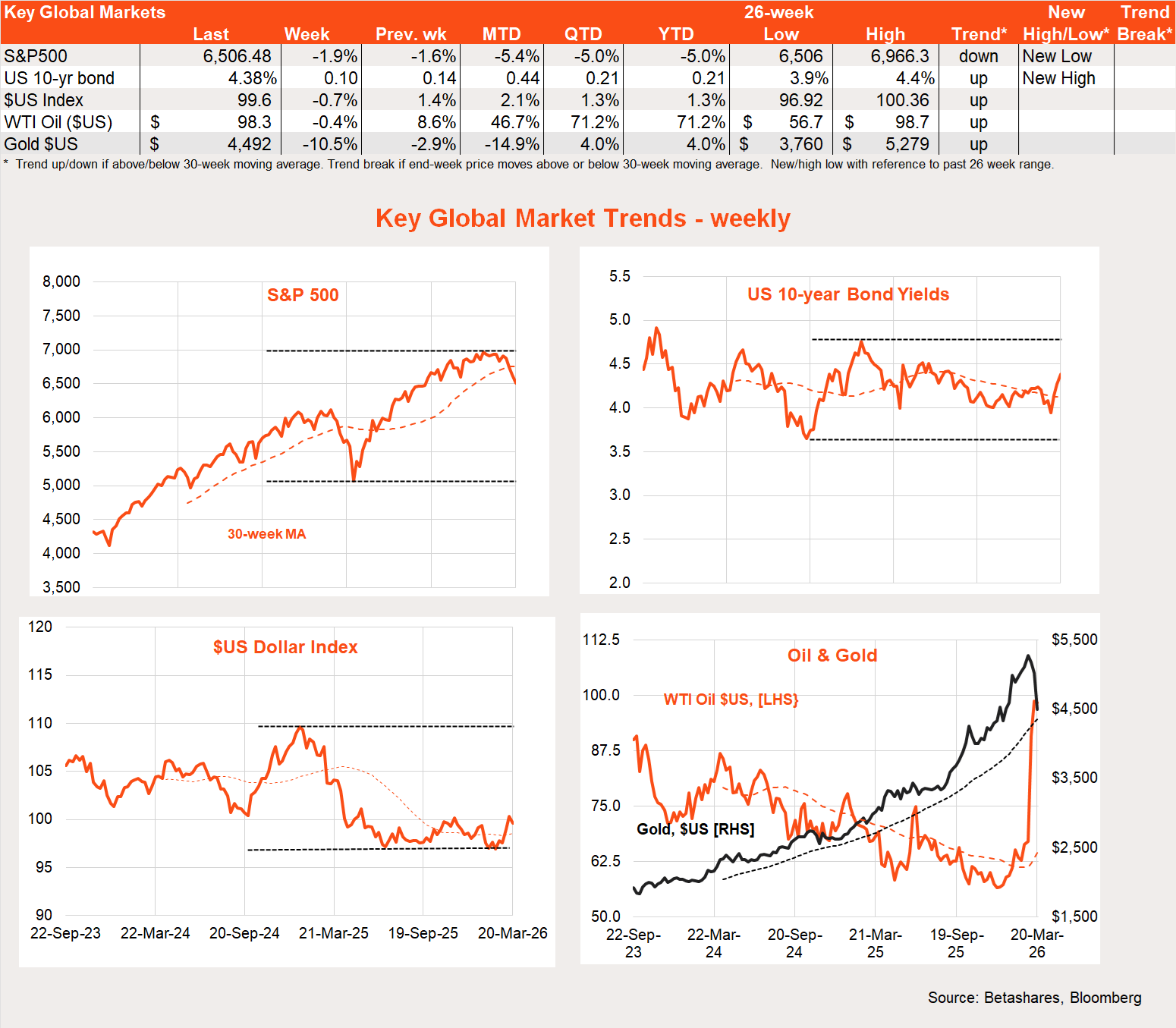

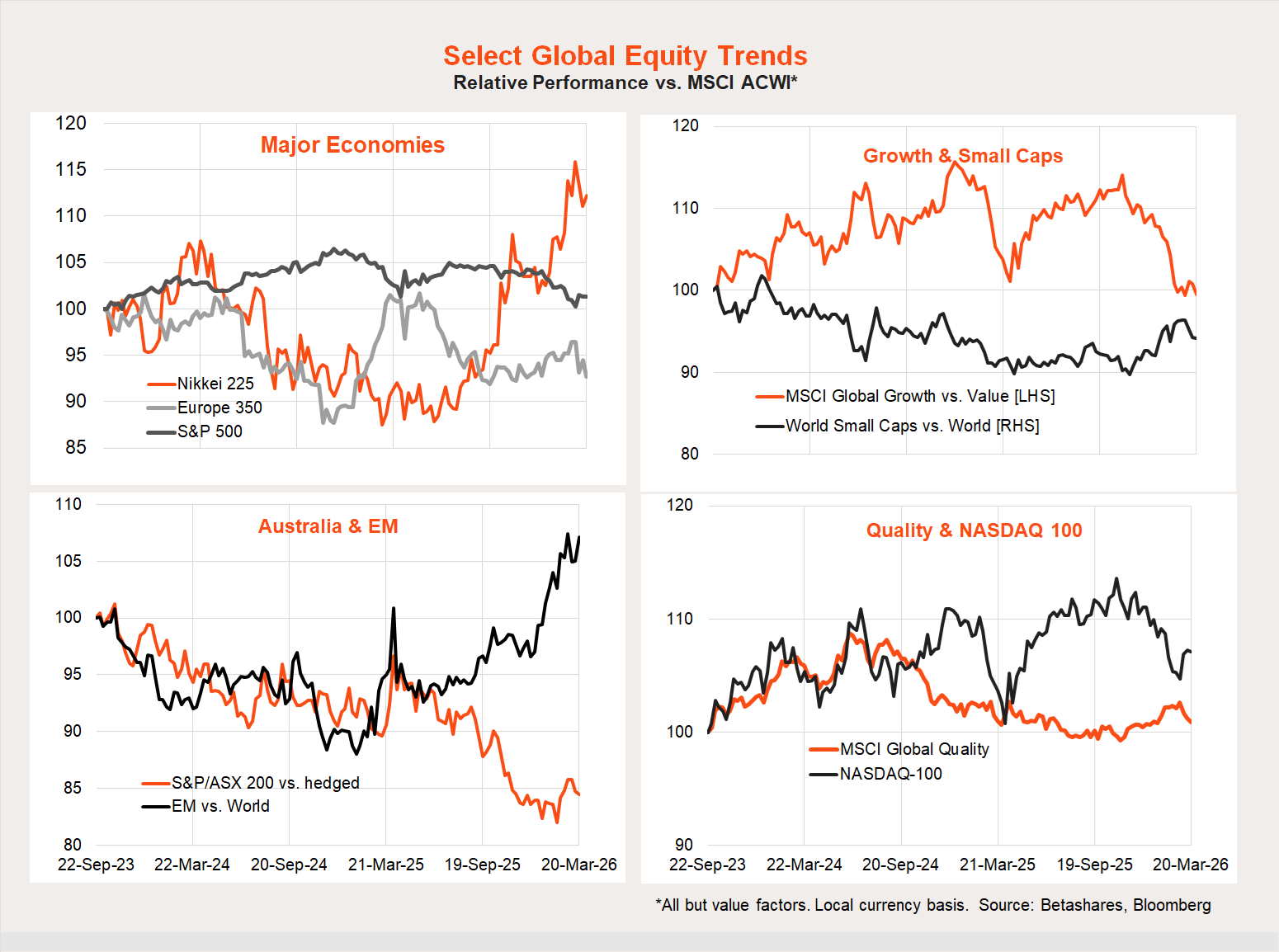

Global equity trends: the great rotation paused

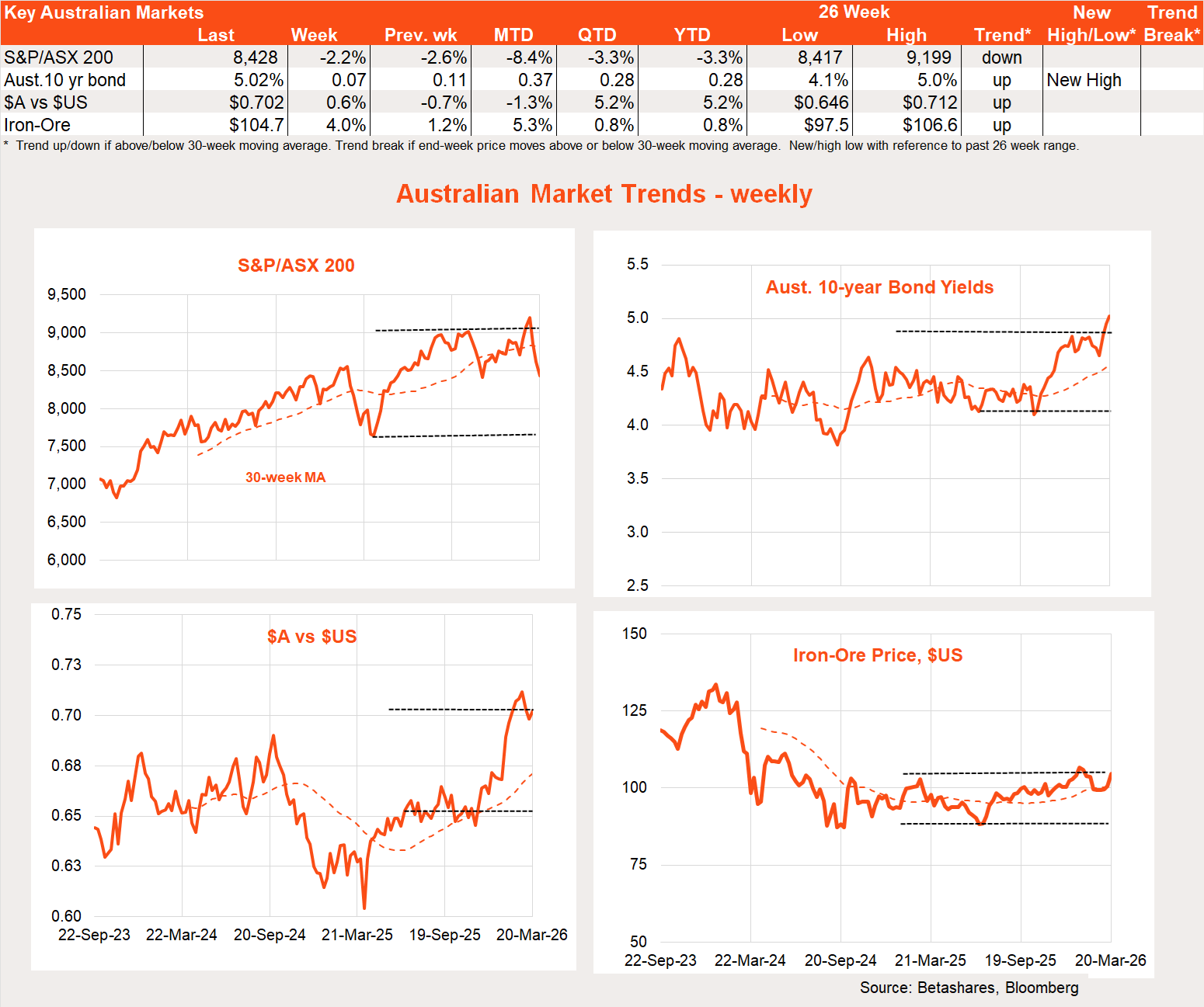

Australian week in review: RBA hike

The major local highlight last week was the RBA’s widely expected decision to raise interest rates by 0.25% to 4.1%.

Although most market observers expected the RBA to raise rates last week, the surprise was the closeness of the decision. Five board members voted for an interest rate hike while four members suggested holding interest rates given geopolitical uncertainty. As RBA Governor Michele Bullock noted, however, all members agreed on the need for likely further tightening – the only debate was on the timing.

Does this mean last week’s rate hike was a bring forward of the May hike – and so a move in May is now less likely? I doubt it.

While the RBA likely anticipated hiking rates in May even before the Iran war, the surge in energy prices and added inflation risk likely added and an extra rate hike to the RBA’s thinking. My base case is a final rate hike in May following a likely hot Q1 CPI report in late April.

In other news, the February labour market report was fairly mixed. While there was a solid 49k increase in employment, most of it was part-time whilst rising labour force participation (especially among older workers) saw the unemployment rate jump back to 4.3% from 4.1%. All up, the labour force now appears a little less “tight” than the RBA previously thought, but likely not enough to ward off another rate hike in May.

Australian week ahead: February CPI

With news of the Australian market down another 1.5% this morning, the S&P/ASX 200 is getting nearer to the 10% correction territory. Given the seriousness of the events in the Middle East, it’s perhaps surprising equities markets have not fallen harder in recent weeks – likely because investors have been hoping Trump would end hostilities at any given moment. So far that’s not been the case and sadly we may need to see more market pain before a Trump TACO moment might arrive.

The main local highlight this week will be Wednesday’s monthly CPI report for February. Although the monthly reports can be volatile and subject to seasonality, markets were dismayed last month with another seemingly “hot” reading for January, with annual trimmed mean inflation ticking up to 3.4% from 3.3%.

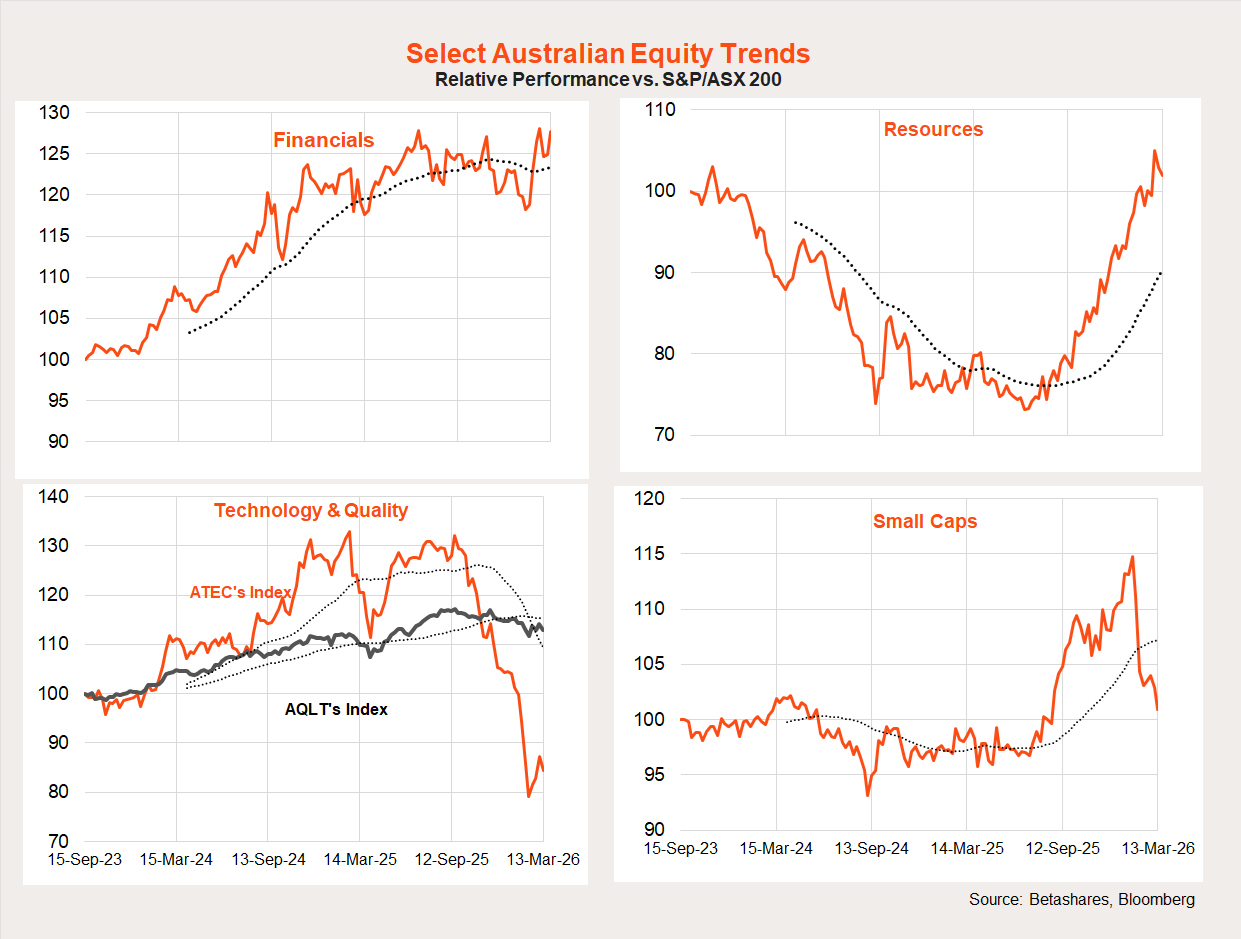

Australian equity trends

Materials were again a major loser on the Australian market last week, declining 7.1% while the energy sector surged a further 6.4%. Technology remained in the red, losing 4.2%.

Given position squaring, the Iran war will naturally play havoc with recent trends over the short run, although energy stocks are a clear winner for now.

Have a great week!