David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

Global week in review: Optimism but Strait still closed

Global stocks rose further last week, reflecting hopes around a two-week US-Iran ceasefire agreement and weekend peace talks.

Markets must face an uncertain new reality this morning, with news overnight that the peace talks (at least the first round) had failed to reach an agreement. What’s more, US President Trump then announced the US Navy would:

- Impose its own blockade, preventing “any and all ships trying to enter or leave” the Strait of Hormuz.

- “Seek and interdict” every vessel on the high seas that has paid a toll to Iran.

- Enter and begin clearing Iranian mines in the Strait, and fire upon “any Iranian… who fires upon us”.

This appears a very tall order for what experts suggest is an already stretched Navy, even if one concedes it is the best in the world.

Sadly this comes despite the fact we did appear to be on the verge of the Strait re-opening, at least for two weeks.

After all, Iran had pledged to keep the Strait open for the two-week ceasefire – albeit provided Israel stops bombing Lebanon. Israel, in turn, had announced its own ceasefire talks with Lebanon, likely under pressure from the US following its last devastating Lebanese strikes just after the US-Iran ceasefire talks were announced.

Iran still maintains it will keep the Strait open, and wants to keep talking.

Global week ahead: Brinkmanship continues

Global events will remain almost exclusively focused on Iran.

Trump’s strategy now seems to be either/or 1) pressure Iran financially by denying it funds from its own oil exports 2) have China pressure Iran into agreeing a deal at the risk of the former losing access to oil.

I can’t see either strategy working. The good news, at least, is that Trump has ceased threatening to blow up Iranian power grids and oil facilities (for which Iran had threatened similar retaliatory strikes across the region).

But we now face an extended blockage of the Strait and new geo-political flashpoints. Will the US really refuse Chinese linked ships from leaving and/or entering the Strait? Will the US really stop any ships that may have paid a toll to Iran – and how could the US verify the payment? Will the US Navy enter the Strait to clear mines and will Iran shoot at them?

The lingering hope is that talks will resume and Trump’s bark will remain worse than its bite when it comes to actually stopping ships at sea. The political reality facing Trump remains as stark as ever: extended blockage of the Strait will only drive up global oil prices, US recession risks and the chance of a Republican wipe-out at the November mid-term elections.

Can a deal be done? According to Trump, the main sticking point is US insistence that Iran renounce any desire for a nuclear bomb. But this is already Iran’s historic official position, although its advanced uranium enrichment program has left many experts long worried and suspicious of its true intentions. Iran could at least continue to pay lip service to its desire not to have a nuclear bomb, though Trump might also insist it give up its current enriched uranium reserves.

A potential face-saving deal for Trump might be one in which Iran merely pledges (as it has previously done so) not to pursue a bomb, although whether Trump still pushes for the enriched uranium could be a sticking point for the Iranians. In exchange, Trump could promise to stop bombing, maybe release some confiscated Iranian wealth and leave the Strait to the Iranians (provided they don’t start charging tolls). These aspects at least seem to be at the heart of the ceasefire debate.

At the time of writing, early market reaction to Trump’s latest threats are measured; Brent crude rose 8.4% in morning trade to $US103 a barrel, while S&P 500 futures were down 1.2%.

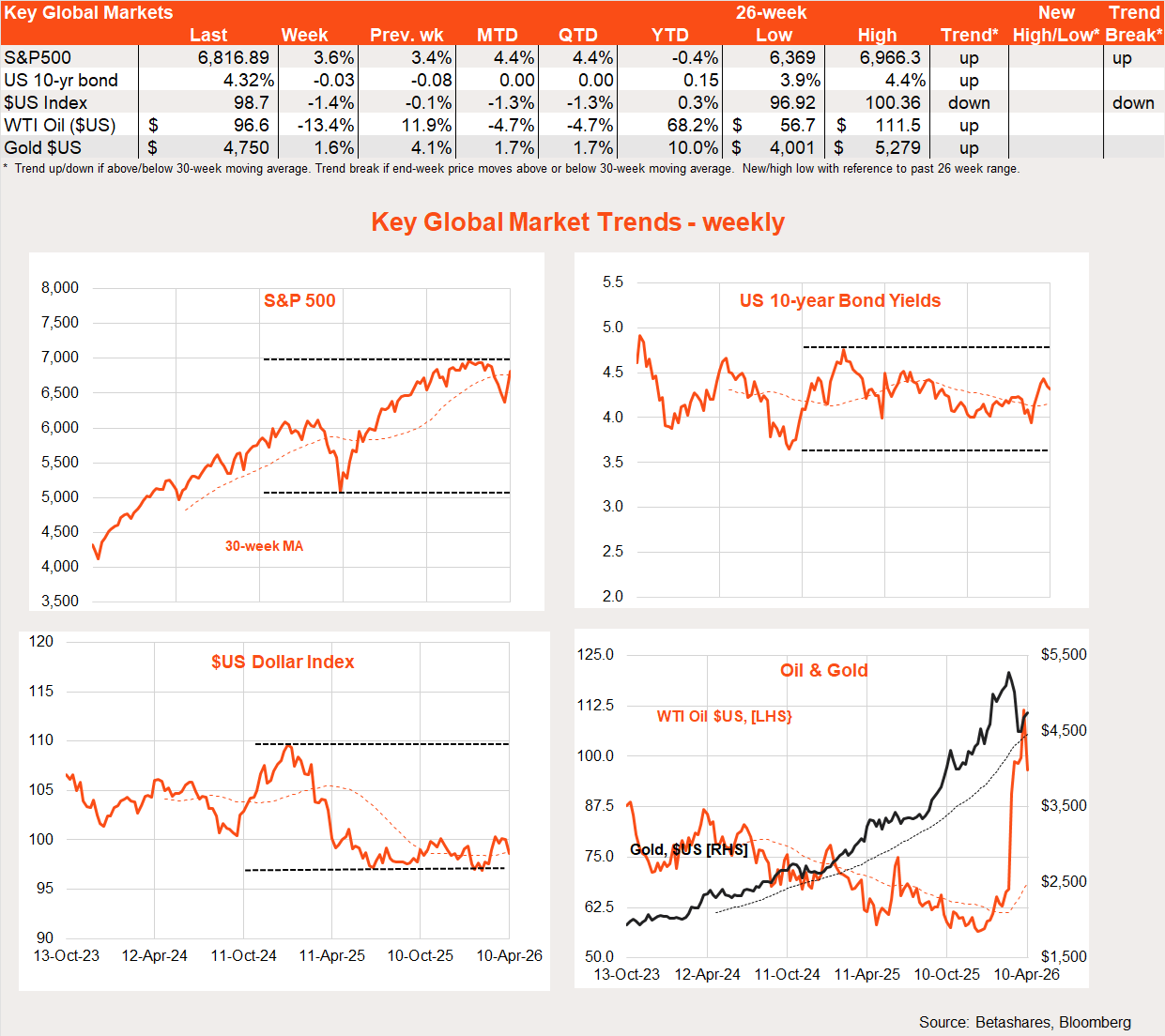

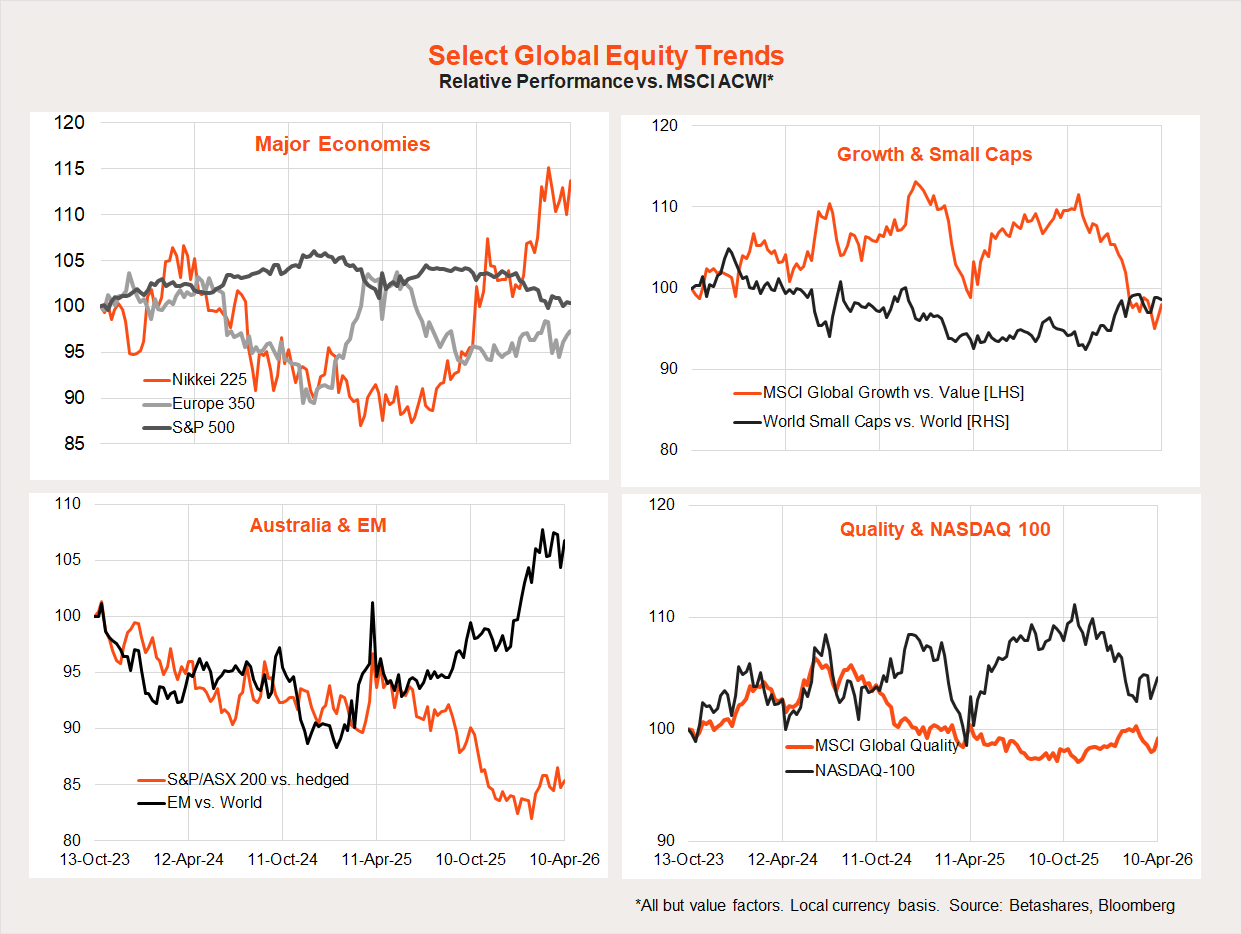

Global equity trends

Last week’s optimism saw those areas hardest hit by the war rebound the most – Japan and emerging markets – while energy declined.

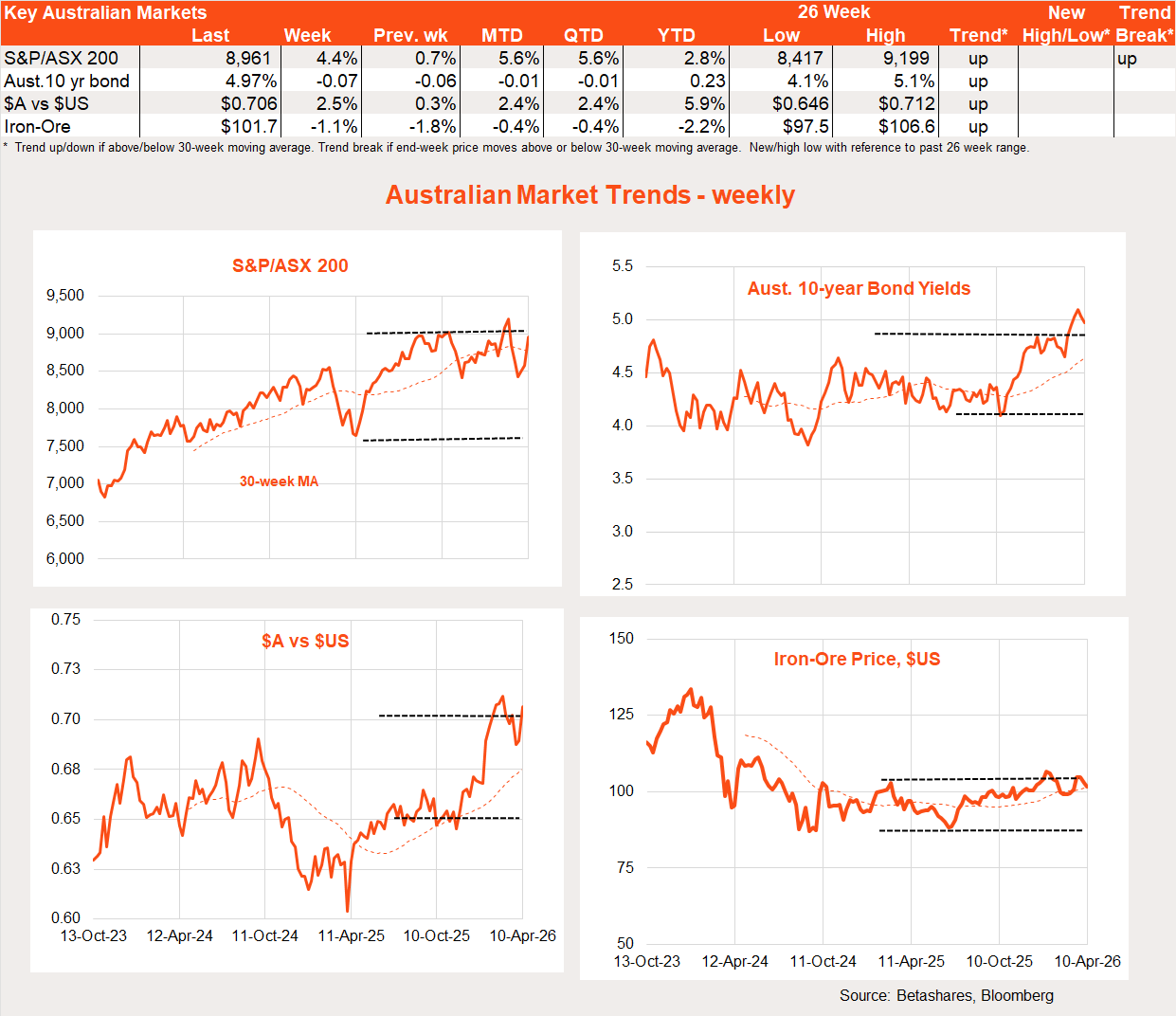

Australia in review: still-firm local data

With little major local economic news, local shares also enjoyed a further bounce last week on Iran hopes.

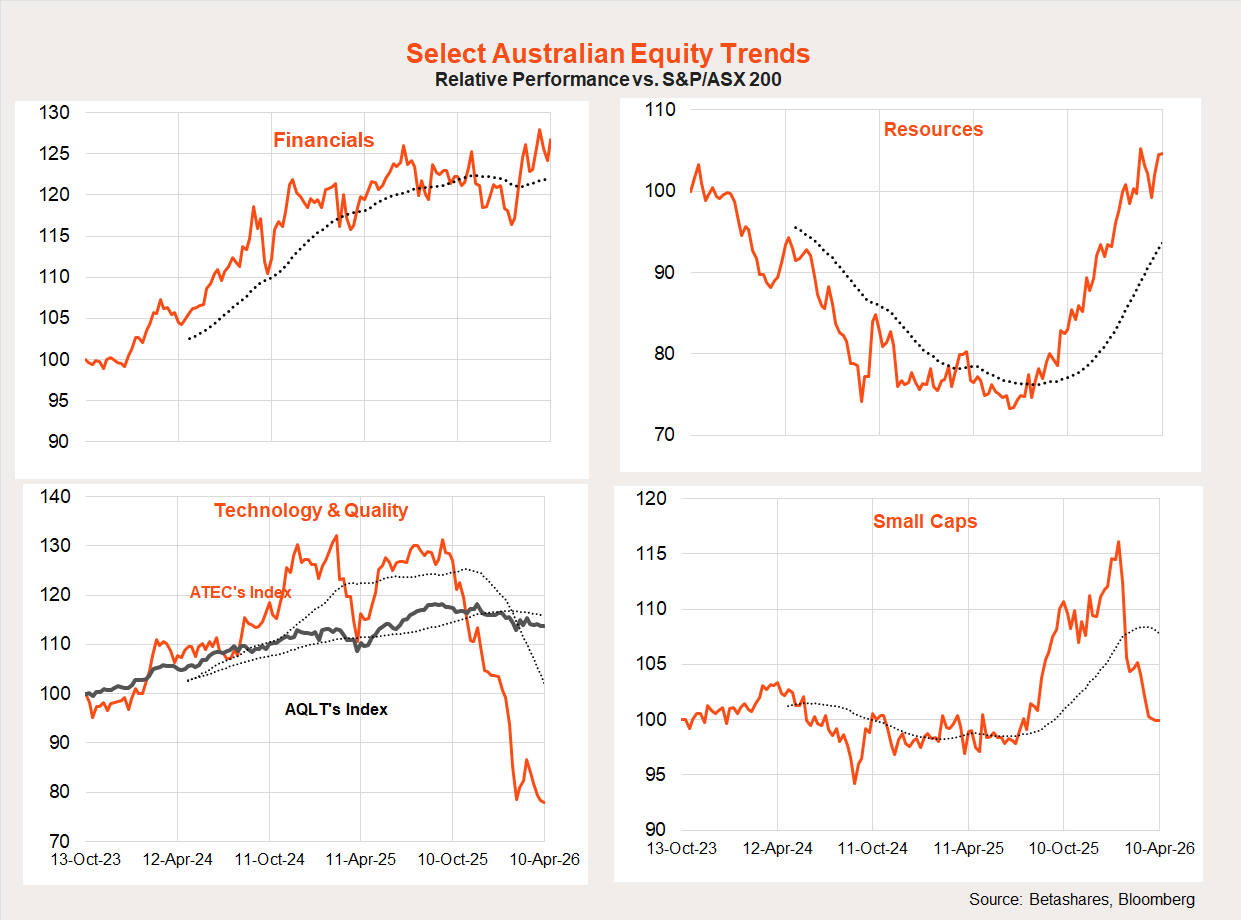

Local equity market trends

The Iran war has not been kind to high-beta local exposures such as technology and small caps. Relative performance of the larger cap resource and financial sectors has been choppy, but both have broadly held up.

Australia week ahead: Iran and employment

We get a smattering of local economic news this week, but focus is likely to remain on Iran. Business and consumer sentiment reports are released tomorrow, with the labour market report on Thursday. It would be surprising if the sentiment surveys did not at least dip given the worrying Iran news, while employment growth is expected to remain firm (a gain of 18k is expected following the 49k gain in February).

As regards the RBA, the question is whether the worsening outlook in Iran makes it less likely it will hike again in May despite the energy-related upward pressure on inflation. The markets have wavered but have broadly retained a probability of around 70%. A May rate hike is still my base case.

Have a great week!