Same hedge, different tax outcome: one key consideration when comparing global bond ETFs

Annabelle Dickson

6 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

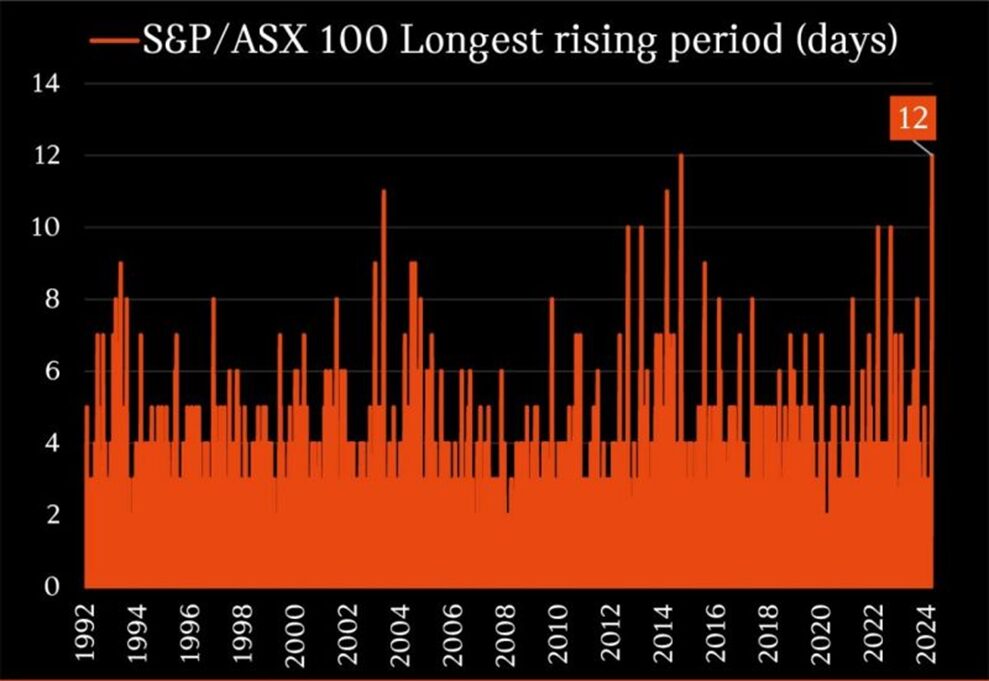

After a short, sharp sell-off at the start of August, large-cap Australian shares (as measured by the S&P/ASX 100 Index) staged a stunning comeback to finish the month essentially where they started. In fact, the S&P/ASX 100 rallied for 12 straight trading days from 9 August, equalling its record for the longest winning streak since the inception of the Index.

Source: Shaw and Partners, S&P Dow Jones Indices. As at 27 August 2024.

So what caused the market’s sudden about-face? Might it continue? And how can investors position themselves in this environment?

Where we stand now

In order to understand the recovery, it’s important to understand the context of the sell-off. We covered it in detail in this webinar and article, but in short, the sell-off was triggered by three main factors:

- An interest rate rise in Japan, leading to an unwind of ‘the Yen carry trade’

- Fears of a US recession

- Expensive US equities.

Let’s explore how each of these has changed (or not).

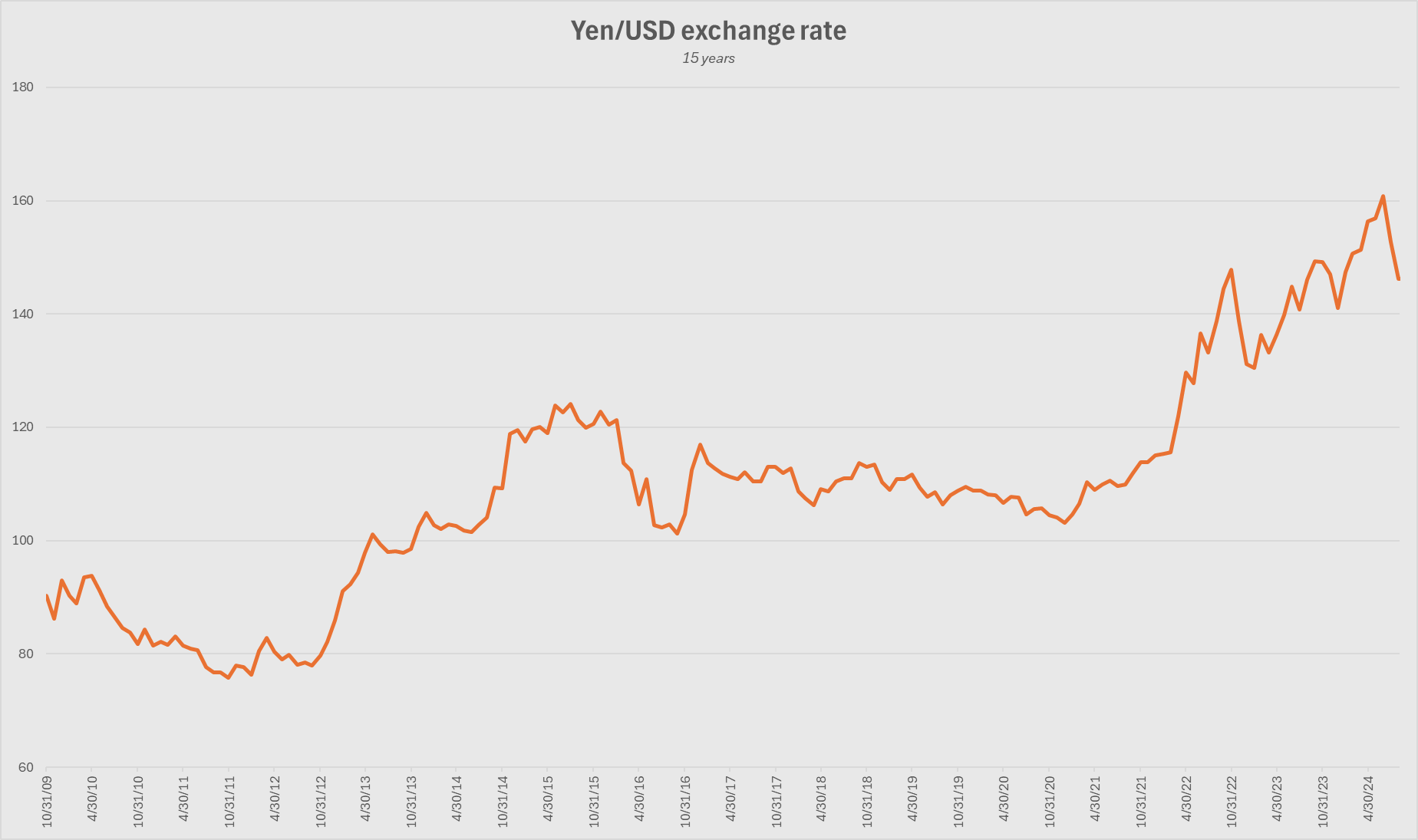

Improvements in Japan

The ‘Yen carry trade’ refers to a longstanding trend of traders borrowing in Japan at very low or even negative interest rates, exchanging the funds for US dollars, and then investing those funds in the US.

This led to a long-term increase in the value of the USD versus the Yen, with the USD peaking at over 160 Yen in June this year. This began to reverse when the Bank of Japan decided to raise interest rates (see chart below).

Source: Yahoo Finance, Betashares. As at 3 September 2024.

Source: Yahoo Finance, Betashares. As at 3 September 2024.

The following week however, Bank of Japan Deputy Governor, Shinichi Uchida said the bank would “not raise its policy interest rate when financial and capital markets are unstable”1. This appeared to placate the markets, with the falls in equities and the rise in the Yen stabilising before beginning to reverse.

Source: Yahoo Finance, Betashares. As at 3 September 2024.

Source: Yahoo Finance, Betashares. As at 3 September 2024.

So for now at least, concerns about this issue appear to have passed. Though it could rear its head again, as Betashares’ Chief Economist David Bassanese explained in Bass Bites, “how the BOJ manages this balancing act remains to be seen.”

US recession fears

The economic news out of the US was almost universally positive in August. July retail sales improved, jobless claims declined, inflation pressures eased, and critically, Q2 GDP growth was upgraded. US Federal Reserve Chair Jerome Powell said in a speech that “the time has come” to begin cutting rates, however, given the recent slew of positive data, Bassanese believes a 0.25% cut seems more likely than a 0.5% cut.

US equities

At a broad, market cap-weighted level, US equities do still appear to be expensive. The S&P 500 recovered last week to hit a new all-time high2, though the Nasdaq 100 still remains somewhat below the mark it set in July3.

Though plenty of opportunities exist for those willing to look. As Bassanese said in Bass Bites, “we’ll need the dust to settle from recent market volatility to discern whether the much-debated broadening in the global equity rally beyond Japan/large-cap technology will gather steam.

Can cheaper value stocks outperform as equity markets continue to trend up? I suspect that they can, but the evidence to date remains patchy.”

Where to from here?

Jerome Powell has telegraphed an imminent US rate cut, ASX data indicates a cut in Australian rates early next year4, and other developed markets such as Europe, Canada, and New Zealand have already cut rates5. So despite sticky inflation, it seems that rates are on their way down, even if Australia appears set to lag the rest of the world.

The ideal scenario is that inflation continues to fall, unemployment remains subdued, and GDP growth is maintained. Bassanese said this ‘soft landing’ scenario remains on track both in the US and locally7, and should be broadly supportive for most asset classes.

But inflation is yet to hit the central banks’ target band in either country, so this ‘goldilocks’ scenario is far from guaranteed. With two thirds of the year now behind us, the three risks laid out in our 2024 market outlook remain relevant.

- Inflation and interest rates may still catch up with the economy, continuing to squeeze living pressures and leading to an increase in bad debts.

- Central banks could be too late to cut rates, leading to rising unemployment and a possible recession.

- Geopolitical concerns could escalate, given continued fighting between Israel, Hamas, and Hezbollah. A Trump presidency remains a distinct possibility, with betting markets indicating that the outcome of the presidential election is essentially a coinflip8. A win for Trump could have significant implications for the wars in both the Middle East, as well as Ukraine and Russia.

Opportunities in ETFs

Given this range of possible outcomes, here are three ETFs investors can consider based on the opportunities in the current state of markets.

Following trends

If you expect recent trends to continue, MTUM Australian Momentum ETF is one way to implement this view. MTUM uses a rules-based strategy that selects stocks based on their 6- and 12-month risk-adjusted returns, creating a portfolio of companies displaying a recent trend of outperforming the broader market.

A reversal of fortunes

Conversely, if you expect cheaper, more value-oriented stocks to make a recovery, QOZ FTSE RAFI Australia 200 ETF may be worth a look. QOZ draws from the top 200 companies listed on the ASX, just like MTUM.

But rather than selecting companies based on their returns, it weighs them based on economic importance, using measures such as sales, cashflow, book value, and dividends. In doing so, it aims to deliver outperformance by selling relatively ‘expensive’ shares while buying those which are comparatively undervalued.

The neutral position

For those who remain ambivalent or agnostic on the question of following trends vs buying undervalued stocks, an equal-weight approach may be suitable. This simple approach treats all companies in the index equally, rather than taking position sizes based on market capitalisation, fundamentals or other factors. QUS S&P 500 Equal Weight ETF provides exposure to the same 500 companies in the S&P 500 Index, but with a 0.2% allocation to each company at the time of rebalancing.

Sources:

3. Nasdaq

4. ASX

6. Oddschecker

Explore

Markets