Tom Wickenden

7 minutes reading time

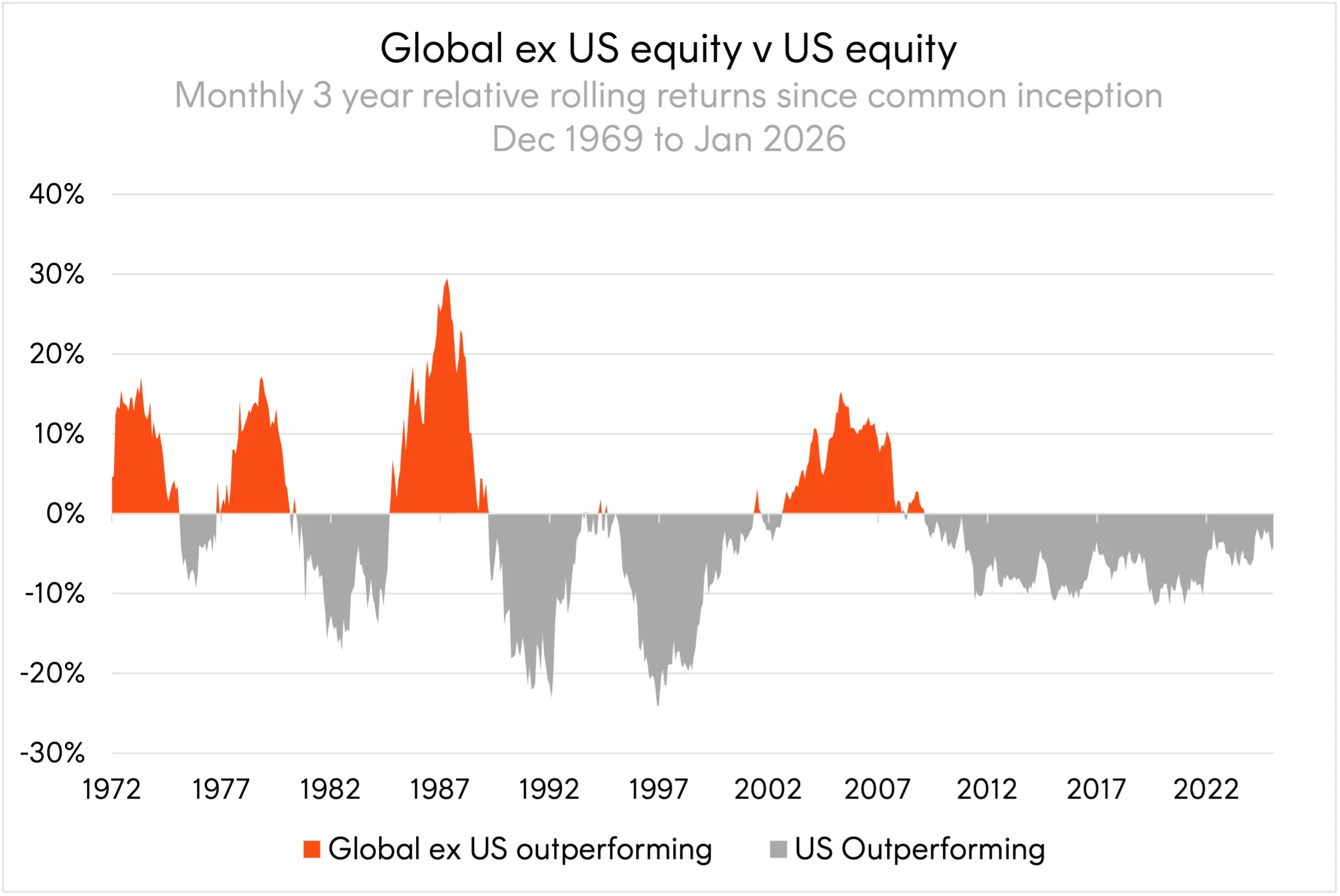

2025 saw developed market equities outside of the US outperform major US indices by the largest margin since 1993 (in USD terms)1. This reversion came during the US’ longest rolling 3-year period of outperformance on record2 – a measure used to capture market cycles, smooth short-term noise, and reveal persistent regime.

Source: Bloomberg. December 1969 to January 2026 Monthly 3 year rolling relative returns of the S&P 500 Index and the MSCI World ex US Index. Past performance is not an indicator of future performance.

Source: Bloomberg. December 1969 to January 2026 Monthly 3 year rolling relative returns of the S&P 500 Index and the MSCI World ex US Index. Past performance is not an indicator of future performance.

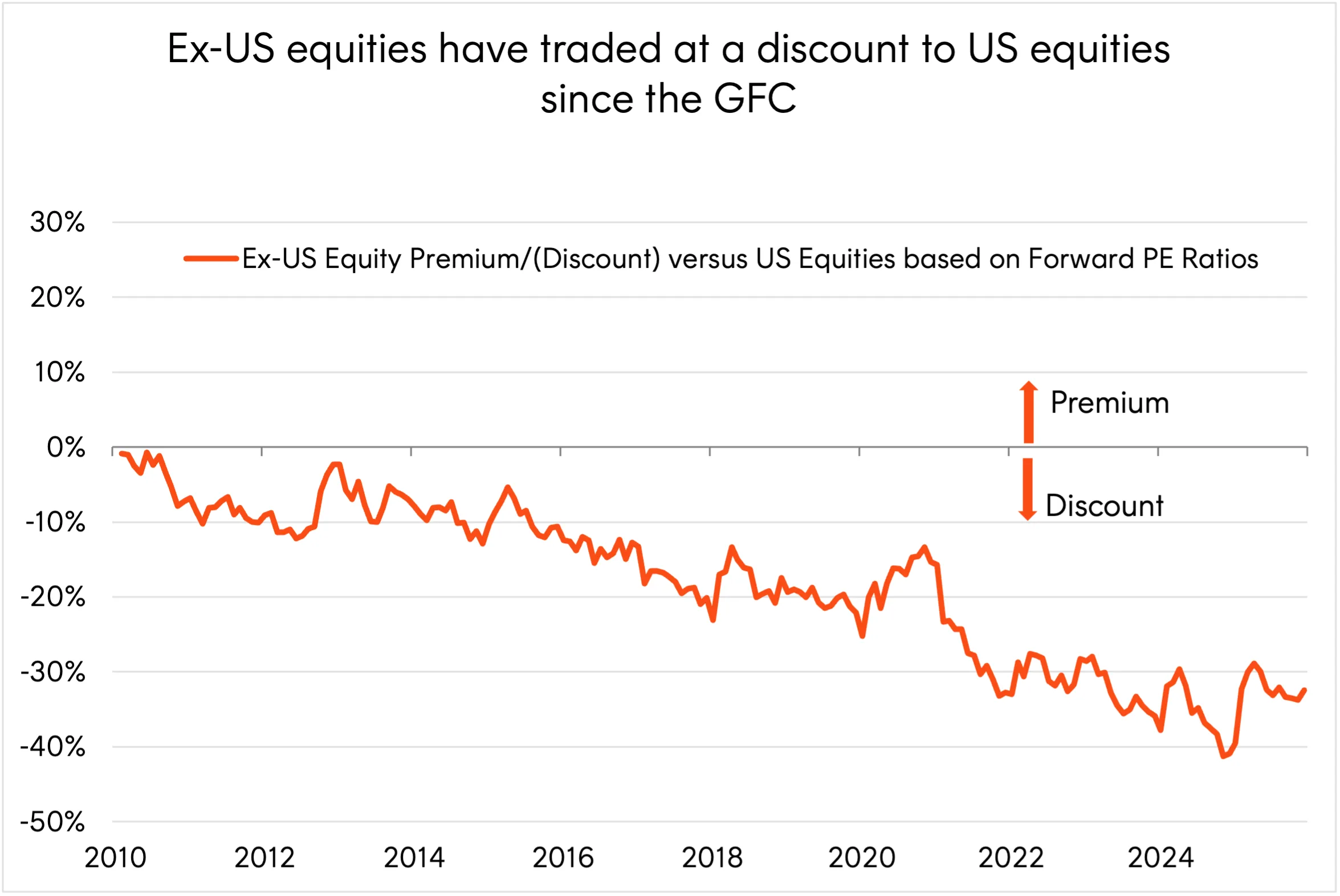

Since the GFC, the rest of the world has underperformed the US due to weaker earnings growth and less multiple expansion. This US dominance has driven US equities to make up over 70% of broad global indices weight and trade at a 30% price to earnings premium to the developed ex-US equities.

Source: Bloomberg. 1 January 2010 to 31 December 2025.

Source: Bloomberg. 1 January 2010 to 31 December 2025.

A key question for Australian investors in 2026 and beyond is whether ex-US equities will continue to outperform and what the most efficient way to gain exposure is if they do.

Europe and Japan’s earnings potential

Outside of the US, developed market equities are predominantly made up of Japanese and European markets – both of which have positive growth catalysts for the year ahead.

In Japan, Prime Minister Sanae Takaichi’s LDP secured the largest lower house election victory in Japan’s post-war history. Together with coalition partner Ishin the ruling bloc holds a two-thirds supermajority, allowing it to override the upper house and pass its fiscal agenda — including tax cuts, increased defence spending, and broader stimulus – without obstruction. As a protégé of the late Shinzo Abe, Takaichi is carrying forward Abenomics with renewed focus on corporate governance reforms now working through Japanese boardrooms. While Japan’s longer-term consensus earnings growth looks modest compared to the US, these structural reforms and fiscal stimulus measures could spur greater than expected growth and support outperformance.

Europe’s outlook has improved following Germany’s critical 2025 fiscal reset to boost infrastructure and defence spending. 2026 should see this increased government spending filter through to improved corporate capex, alongside increasing clarity over US tariffs and trade. The fiscal package also includes consumer-friendly measures such as a permanently lower VAT rate on restaurant bills and energy bill subsidies.

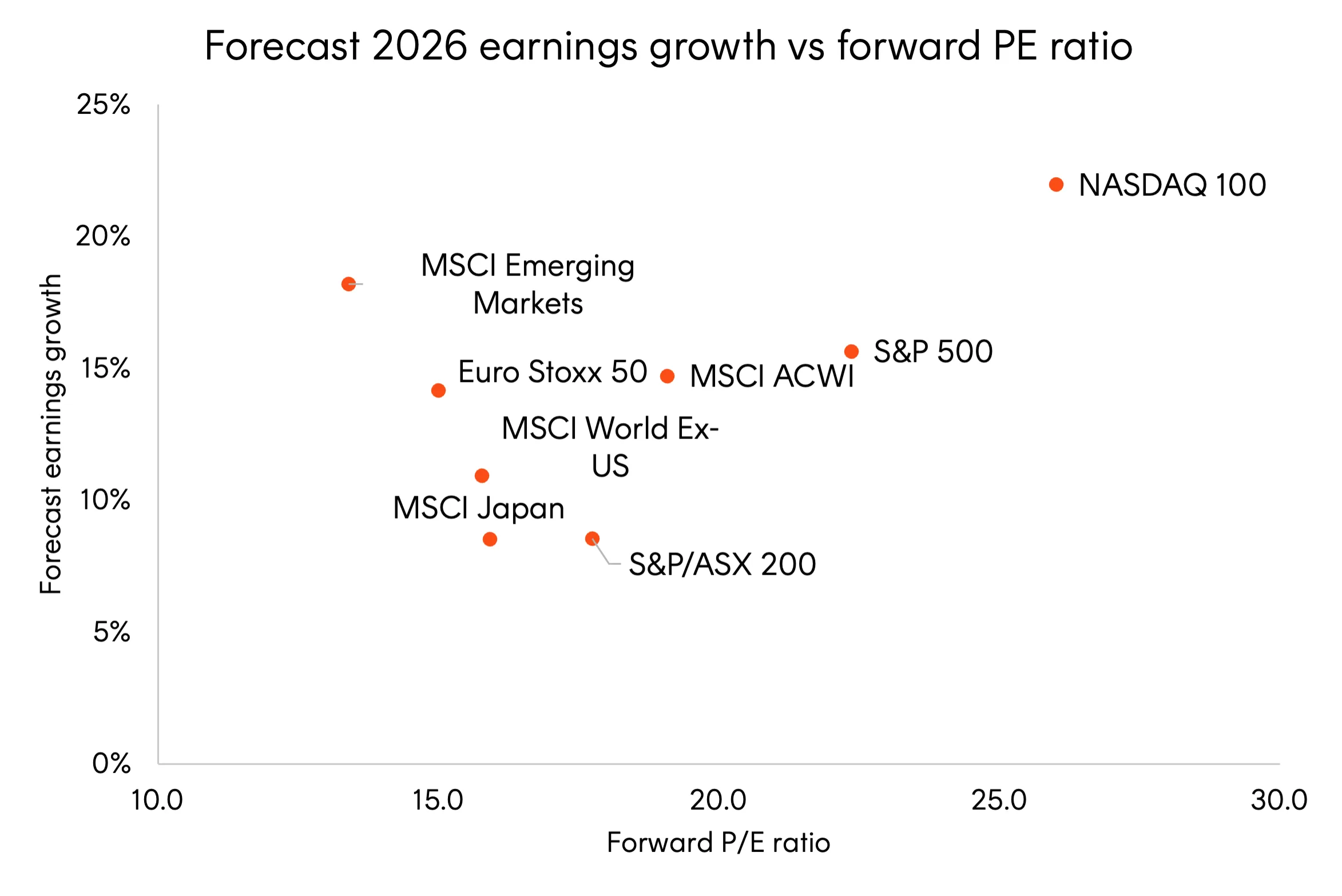

These developments see the Euro Stoxx 50 Index offering similar forward earnings expectations as the US’ S&P 500 Index in 2026 at much lower valuation levels3.

Source: Factset, forecast 2026 earnings growth is based on analyst consensus. As at 13 January 2026.

Source: Factset, forecast 2026 earnings growth is based on analyst consensus. As at 13 January 2026.

The potential for earnings upgrades, undemanding valuations, and our expectation of USD weakness, lead us to believe that ex-US developed markets can outperform US equities in 2026 in AUD terms (on an unhedged basis).

Within this context, EXUS Global Shares Ex US ETF provides a thoughtfully constructed ETF designed specifically for Australian investors, offering exposure to developed markets excluding the US and Australia.

An ETF built for the Australian allocator

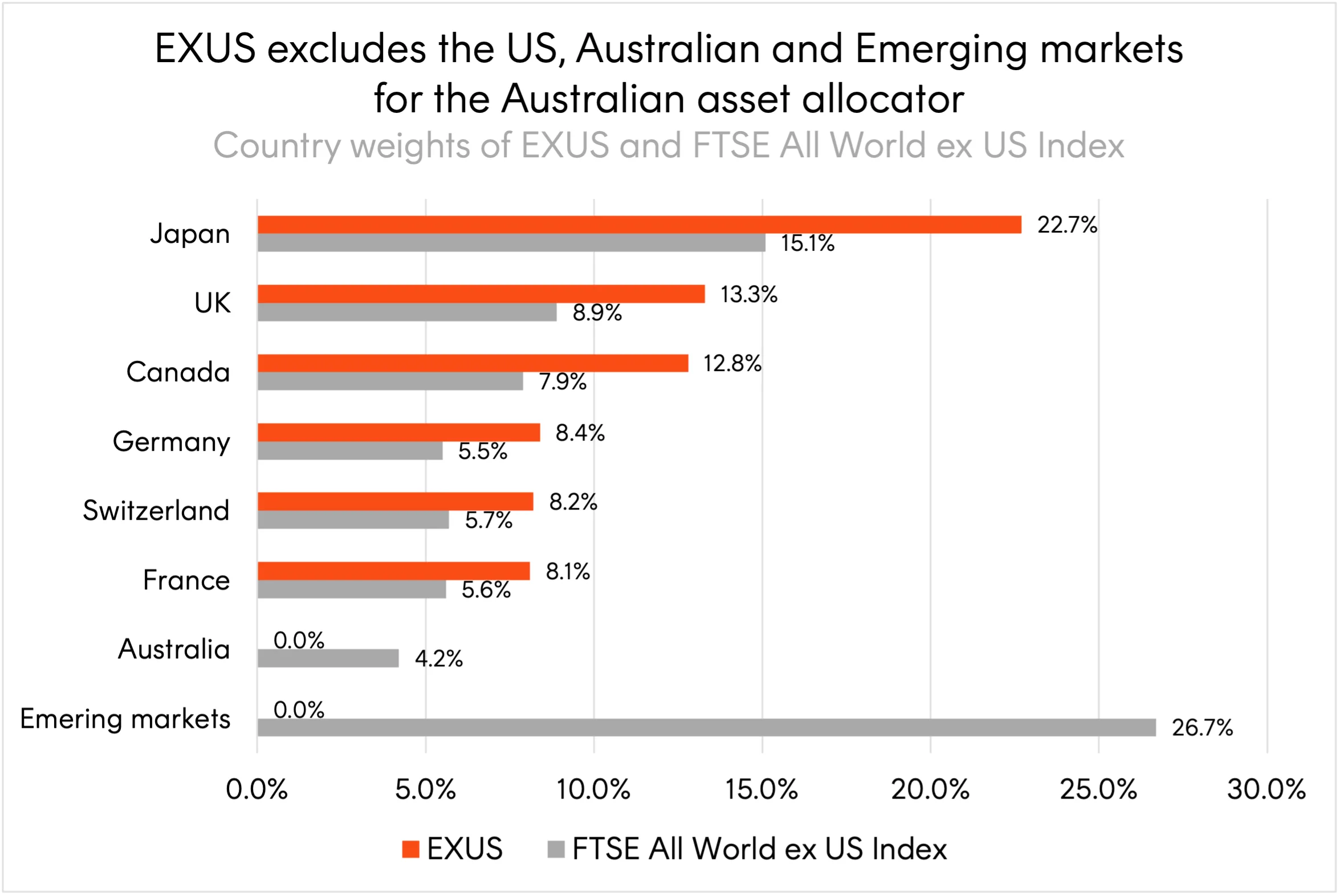

The index EXUS aims to track is designed to provide exposure to the world’s largest developed market companies, based on their free-float market capitalisation, excluding both Australia and the US.

The exclusion of Australian equities, alongside the US, is unique for a broad global ex-US ETF in the Australian market4 and reduces holdings overlap for Australian investors. By comparison, in the FTSE All-World ex US Index, Australia is the 8th largest country allocation and CBA and BHP are the 16th and 27th largest individual holdings respectively5.

Source: Solactive, Bloomberg. As at 31 January 2026. EXUS is Betashares Global Shares Ex US ETF. Constituents are subject to change.

The Index also invests only in companies incorporated in developed markets6, excluding emerging markets from its allocation. By comparison, emerging markets currently make up 27% of the FTSE All-World ex US Index7.

This is done both to remove the limitations of practical index tracking that arises with emerging market equities as well as to allow allocators greater control over their strategic allocation to emerging markets.

An efficient fund structure for the Australian market

In launching EXUS, Betashares also took the Australian investor into consideration when choosing the fund’s structure.

EXUS is an Australian domiciled ETF that invests directly in underlying companies. As is typical for a fund of this nature and structure, EXUS will use a sampling strategy with the aim of efficiently tracking the Index.

By directly investing in underlying companies, EXUS entitles investors in the ETF to receive withholding tax (WHT) credits associated with relevant foreign dividends8.

This may sound like a given for an Australian ETF however alternate ETFs listed on the ASX but domiciled offshore forgo dividend WHT credits which are not passed through to Australian investors.

The value of the lost tax credits depends on an individual tax payer’s tax rate, however, by comparison, the quantum for an ETF of this nature can be greater than a typical low-cost index tracking ETF’s management fees9. Not all Australian investors will be able to claim the foreign income tax offset.

Investment implications

With the potential for developed ex-US market outperformance to continue and the current high levels of concentration of US equities in broad market indices, investors should be considering how their portfolios are positioned.

EXUS represents a core asset allocation building block purpose built for Australian investors. Alongside other well-constructed core building block ETFs, EXUS can help to create the foundations of a diversified, low cost, efficient portfolio.

For more detailed information you can read EXUS’s investment brochure here.

Or visit EXUS Global Shares Ex US ETF .

There are risks associated with investment in the Fund, including market risk, international investment risk, medium sized companies risk and currency risk. Investment value can go up and down. An investment in the Fund should only be made after considering your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available at www.betashares.com.au.

Sources:

1. Source: JP Morgan. International equities: Global structural changes driving narrowing U.S. earnings growth exceptionalism ↑

2. Source: Bloomberg. As at 31 January 2026. Since available index data for S&P 500 and MSCI World ex US Index. ↑

3. Source: Factset, forecast 2026 earnings growth is based on analyst consensus. As at 13 January 2026. ↑

4. As of 31 October 2025. ↑

5. Source: Bloomberg. As at 27 October 2025. Country and single security allocations are subject to change. ↑

6. Eligible companies are assigned to their respective country, based on their country of primary listing/country of incorporation. If a company is incorporated and listed in different countries, Solactive will consider the company’s country of domicile and country of risk to determine the appropriate country classification. ↑

7. Source: Bloomberg. As at 31 January 2026. Emerging markets allocations are subject to change. ↑

8. Where an Australian domiciled ETF invests directly in companies listed in a foreign country with which Australian has a double taxation agreement. Not tax advice. ↑

9. Based on Betashares’ analysis of the distributions and associated WHT credits between between July 2024 and June 2025 for an ASX listed ETF, which is a CHESS Depository Interest in a US domiciled ETF, with similar underlying holdings to EXUS. Calculations assume the same distribution yield applies to both the Australian ETF and US domiciled ETF. ↑