Jing Jia

6 minutes reading time

This email has been prepared for financial adviser use only. It must not be distributed or made available to retail clients.

Key points

- The RBA held rates steady as widely expected, though the tone from the governor and the statement was clearly hawkish

- Forward guidance was clear – rate cuts are off the table due to upside risks to inflation and strong domestic demand

- Markets are now pricing in two rate increases next year, although many economists continue to forecast the RBA will maintain rates at current levels for an extended period

- A February RBA hike is a “live” possibility, although May/June is when markets would have fully priced in one 25bps increase

- The RBA remains data dependent and will be closely watching the CPI data to be released in Jan (7th and 28th), labour force on Jan 22, and the household spending indicator on Jan 12

Market reaction

Tuesday (November 9) delivered a textbook hawkish central bank response in domestic bond and money markets, with short-end yields rising more than longer-end yields (bear flattening). Worth noting is the pronounced divergence over the past month between Australia and the US, with market pricing for the gap in terminal RBA and Fed rates widening by over 70bps since the previous RBA meeting. This likely also weighed on the performance of our equity and credit markets, with both trailing the US since the last RBA meeting.

|

Domestic |

Current level |

Prior close level |

1d change |

Last RBA meeting level (Nov 4) |

Changes between RBA meetings |

|

RBA cash rate |

3.60 |

3.60 |

0 bps |

3.60 |

0 bps |

|

1-Month BBSW |

3.55 |

3.55 |

1 bps |

3.55 |

0 bps |

|

3-Month BBSW |

3.72 |

3.70 |

2 bps |

3.64 |

8 bps |

|

6-Month BBSW |

4.09 |

4.04 |

5 bps |

3.87 |

22 bps |

|

3-year Aus Govt bond yield |

4.19 |

4.14 |

5 bps |

3.67 |

52 bps |

|

10-year Aus Govt bond yield |

4.79 |

4.76 |

3 bps |

4.35 |

44 bps |

|

Major bank 5-year senior credit spread |

72 |

71 |

0 bps |

70 |

1 bps |

|

Major bank 5-year T2 credit spread |

128 |

129 |

0 bps |

122 |

7 bps |

|

ASX 200 SPI futures |

8600 |

8590 |

0.12% |

8812 |

-2.41% |

|

US |

Current level |

Prior close level |

1d change |

Last RBA |

Changes between RBA meetings |

|

US Fed funds rate |

3.89 |

3.89 |

0 bps |

3.87 |

2 bps |

|

SOFR |

3.95 |

3.93 |

2 bps |

4.00 |

-5 bps |

|

UST 2-year yield |

3.61 |

3.58 |

4 bps |

3.58 |

4 bps |

|

UST 10-year yield |

4.19 |

4.16 |

2 bps |

4.09 |

10 bps |

|

US Investment Grade Credit Spread |

112 |

112 |

0 bps |

117 |

-5 bps |

|

S&P 500 |

6841 |

6847 |

-0.09% |

6772 |

1.02% |

|

NASDAQ |

25669 |

25628 |

0.16% |

25436 |

0.92% |

Source: As at 10 December, 2025. Bloomberg

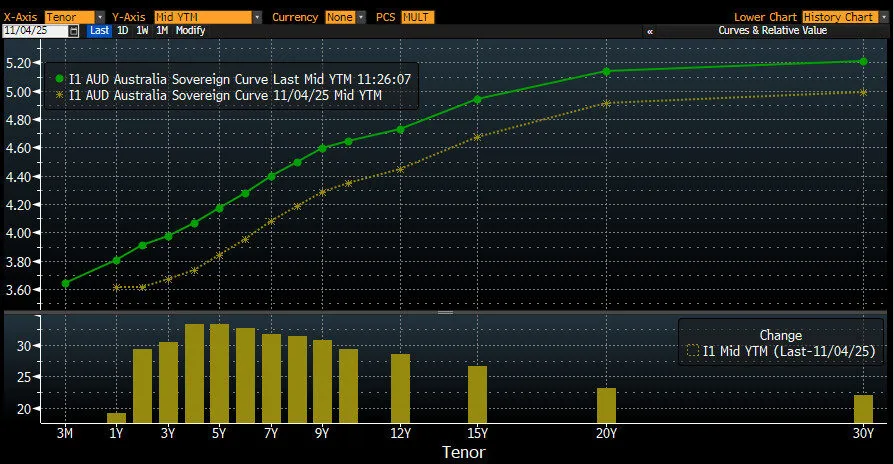

Australian government bond yield curve – 04/11/25 vs current

Source: As at 10 December, 2025. Bloomberg

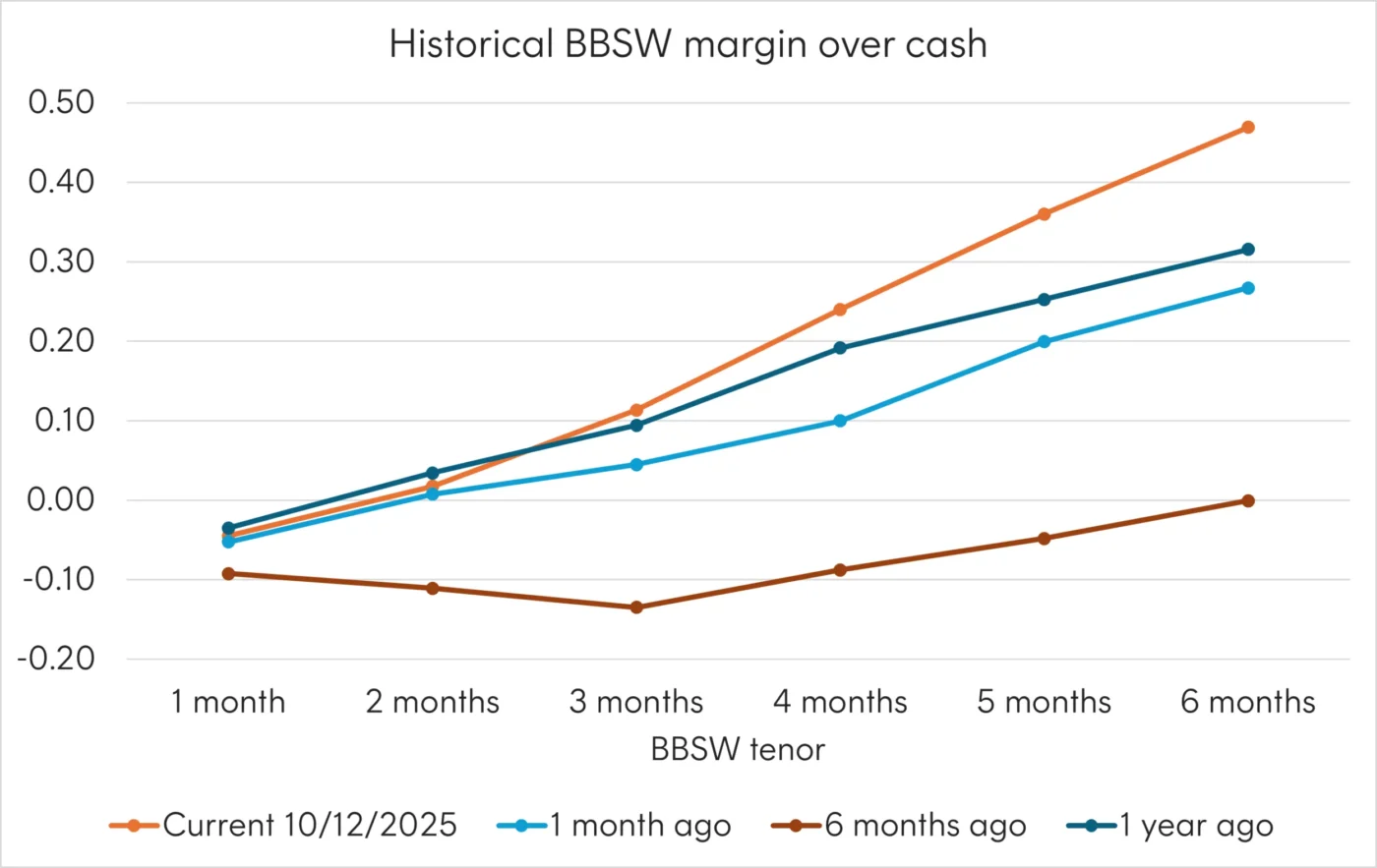

Australian BBSW curve – steepening over the past 6 months now providing attractive term premium in money markets

Source: Bloomberg

Implications for investors

Market expectations for a higher RBA terminal rate have pushed yields higher across the curve. Notably, yield curve “normalisation” at the front/short end creates better opportunities for investors to secure attractive levels of income. With a potential “RBA pivot” ahead, I want to highlight a simple but important consideration for investors: how to extract more value from cash. Specifically, how to capture the benefits of anticipated future rate hikes before they occur, rather than waiting for banks to pass on rate increases, which as we know is far from a sure thing.

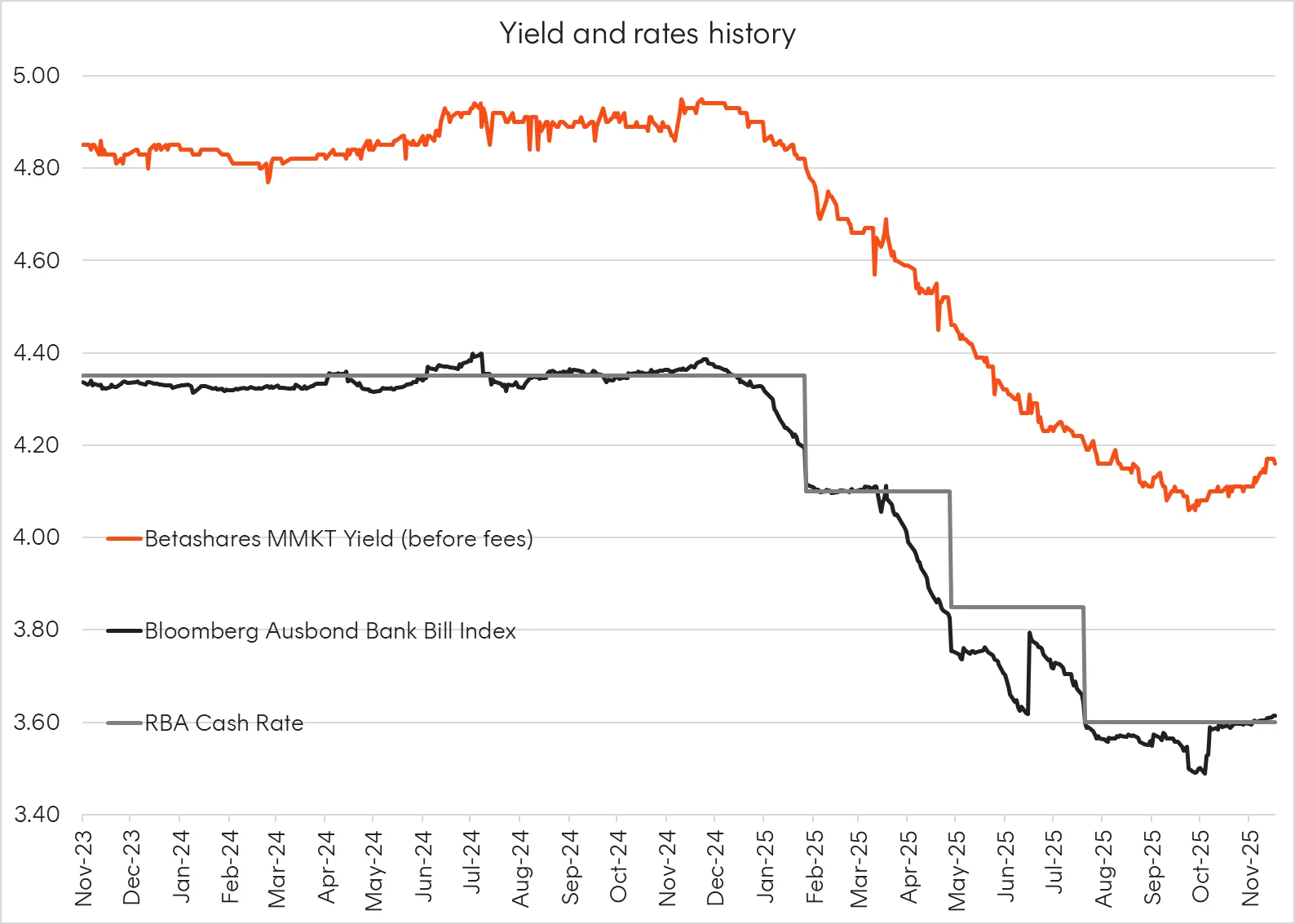

Regular readers of my notes will be familiar with my preferred cash solution: MMKT Australian Cash Plus Active ETF . Let me give you a quick refresher on the fund, which recently celebrated its 2-year birthday. Thanks to the repricing of Australian cash yields and the steepening of the BBSW curve, MMKT’s yield margin over the RBA cash rate is trending higher; it currently sits at 0.56%/0.38% before/after fees and climbing. This means investors in MMKT can potentially capture the benefit of expected RBA rate hikes before they actually happen, unlike bank deposit rates which have historically lagged increases to the RBA cash rate.

Yields and rates comparisons of MMKT and cash benchmarks

Source: As at 10 December, 2025. Bloomberg, Betashares. Yield will vary and may be lower at time of investment. MMKT MER is 0.18% p.a.. You cannot invest directly in an index. Past performance is not indicative of future performance.

Historical returns of MMKT versus cash benchmarks

|

|

MMKT |

Bloomberg Ausbond Bank Bill Index |

RBA Cash Rate Total Return Index |

|

3 months |

0.97% |

0.89% |

0.90% |

|

6 months |

1.99% |

1.83% |

1.85% |

|

1 year |

4.35% |

4.02% |

4.00% |

|

Since common inception (p.a. annualised) |

4.60% |

4.24% |

4.22% |

Source: Bloomberg. As at 9 December 2025. Performance shown since common inception of 22 November 2023, indexed to a starting value of 100 in the chart. MMKT returns are calculated in Australian dollars using net asset value per unit at the start and end of the specified period and do not reflect brokerage or the bid ask spread that investors incur when buying and selling units on the ASX. Returns are after fund management costs of 0.18% p.a., assume reinvestment of any distributions and do not take into account tax paid as an investor in the Fund. Returns for periods longer than one year are annualised. Current performance may be higher or lower than the performance shown. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Key facts and features of MMKT (as at 10 December 2025)

- AUM: $477 million, $304 million inflows YTD

- Estimated yield to maturity net of fees: 3.98% p.a.

- Distribution frequency: Monthly

- Holdings: Cash (overnight cash and TDs), Money Market Instruments (NCDs, CPs & Senior FRNs)

- Management fee: 0.18% p.a.

- Website: https://www.betashares.com.au/fund/australian-cash-plus-fund/

- Strategy: Systematically harvests best value risk premia available in money markets using a buy-and-hold strategy with no portfolio churning

- Liquidity: Provides constant liquidity, trades on the ASX with T+2 settlement

Disclaimer:

There are risks associated with an investment in MMKT, including interest rate risk, credit risk, and market risk. Investment in MMKT does not receive the benefit of any government guarantee. Investment value can go up and down. An investment in MMKT should only be made after considering your particular circumstances, including your tolerance for risk. For more information on risks and other features of MMKT, please see the Product Disclosure Statement and Target Market Determination, both available on www.betashares.com.au. Past performance is not indicative of future performance.