Despite the ongoing war in the Middle East, many share markets are at all-time highs.

This dichotomy may not seem intuitive at first. The closure of the Strait of Hormuz has lifted oil prices, dragging on economic growth through reduced consumer spending and fuelling inflation through higher input costs.

These effects are playing out: the IMF downgrading global growth expectations1 while headline inflation in Australia and the US has reached multi-year highs. Historically, this ‘stagflationary’ undertow is bad for stocks and bonds as we saw during the 1970s and again in March.

Yet it is worth noting that the stock market is forward looking and reflects future expected earnings and economic growth, meaning it can often ‘price in’ a different scenario to what the real economy is experiencing.

The AI capex juggernaut rolls on

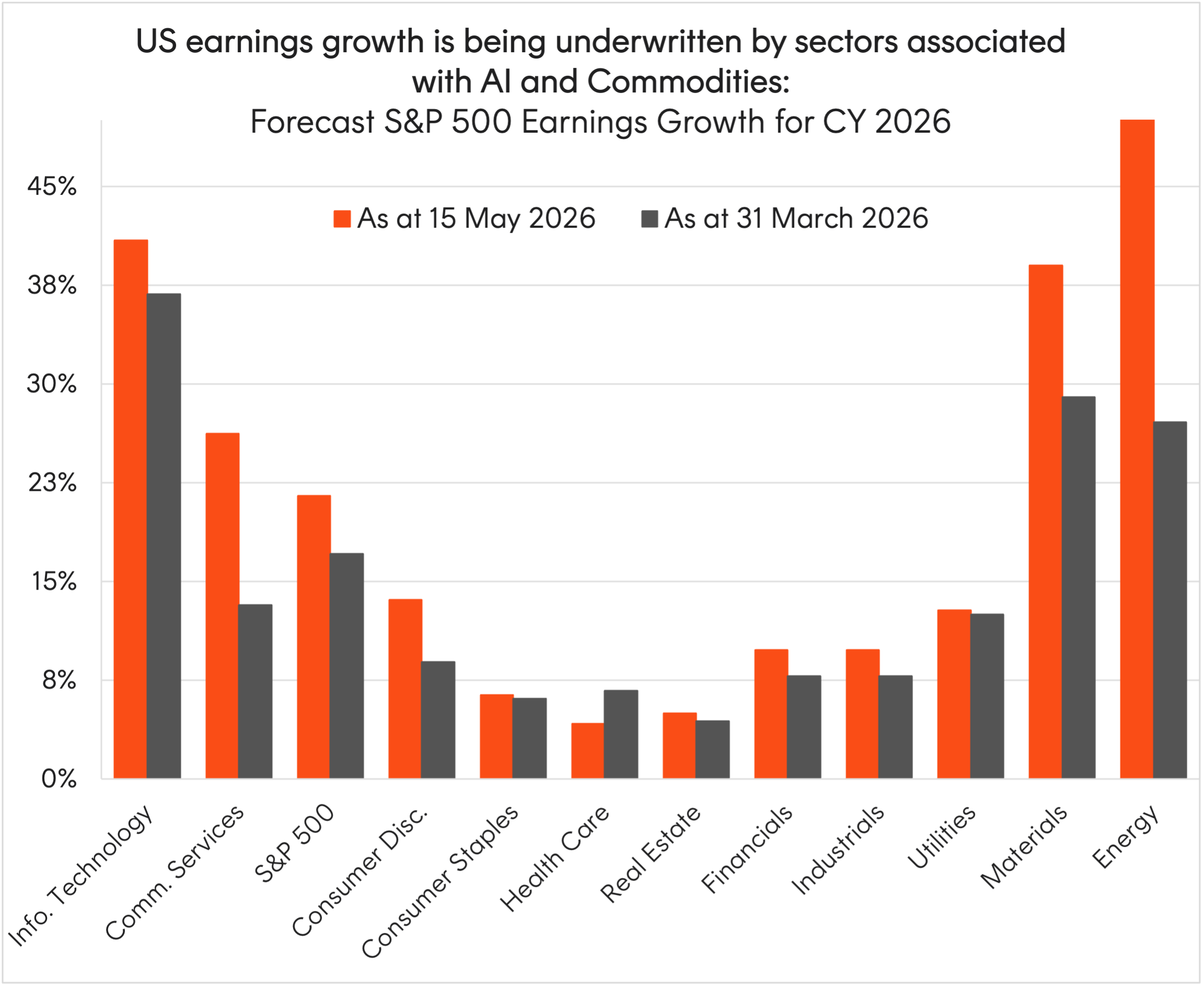

Much of the optimism priced into equities can be attributed to renewed strength in the AI theme, particularly driven by the hardware and semiconductor sub-sectors. Companies like Nvidia and Micron delivered strong EPS beats, contributing almost half of the IT sector’s 53% year-over-year earnings growth.2

Nvidia grew revenues by 85% to US$81.6 billion for the first quarter, driven by strong demand for its Blackwell architecture and AI infrastructure deployments. Importantly, revenue guidance of US$91 billion is a sign that US big tech spending is here to stay and buoy markets in the interim.

Source: Factset. As at 15 May 2026.

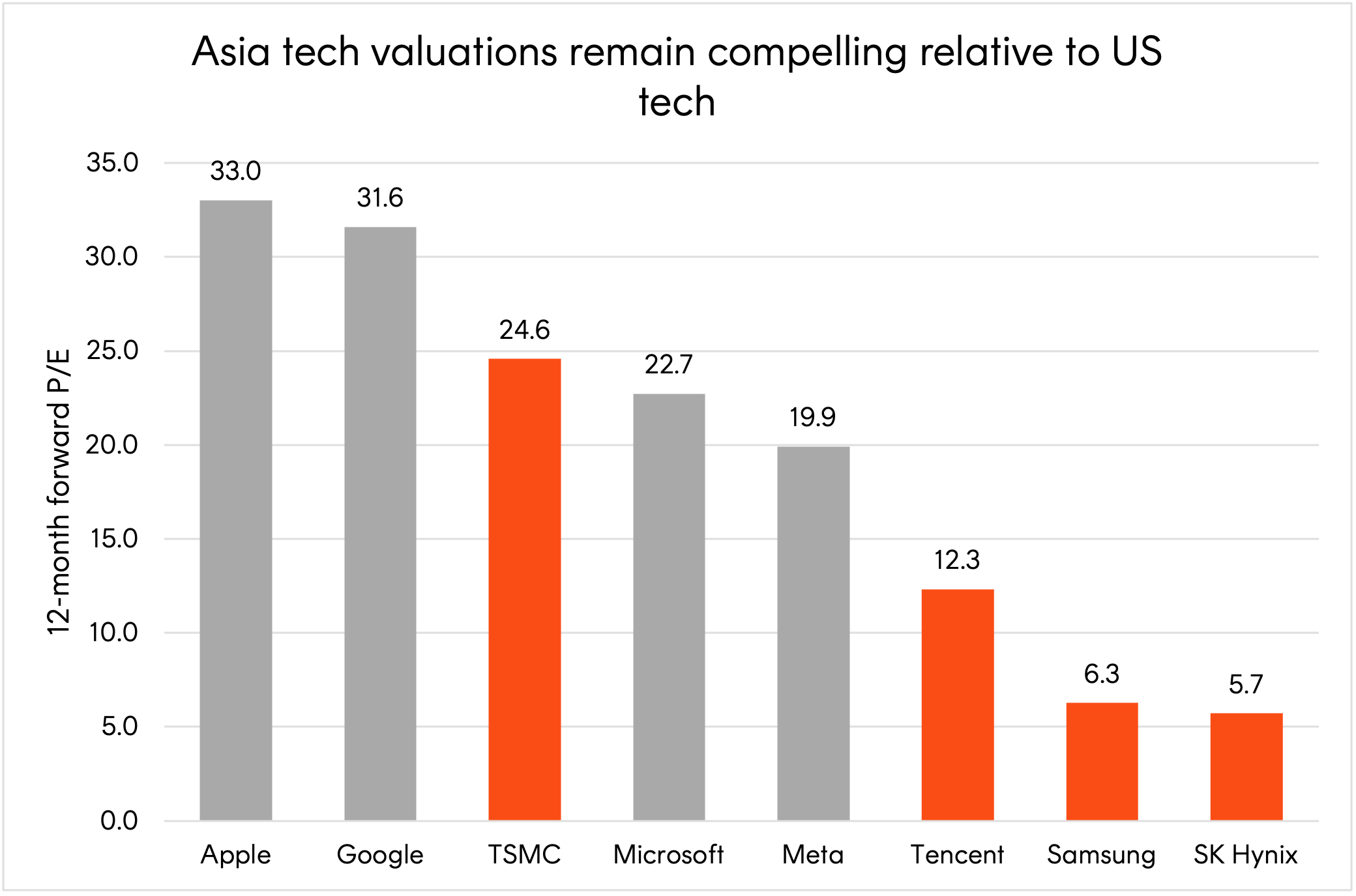

Abroad, the impact is also being felt by South Korean memory chip manufacturers Samsung and SK Hynix which have both experienced massive windfalls in recent months due to the squeeze in HBM (high-bandwidth memory) prices. On their own, these two companies have been large contributors to South Korea’s stock market rise with the local KOSPI index up threefold in just 12 months. Despite the rally, Samsung and SK Hynix shares are trading at forward price to earnings valuations of just 6.3x and 5.7x respectively3.

Source: Bloomberg. As at 18 May 2026.

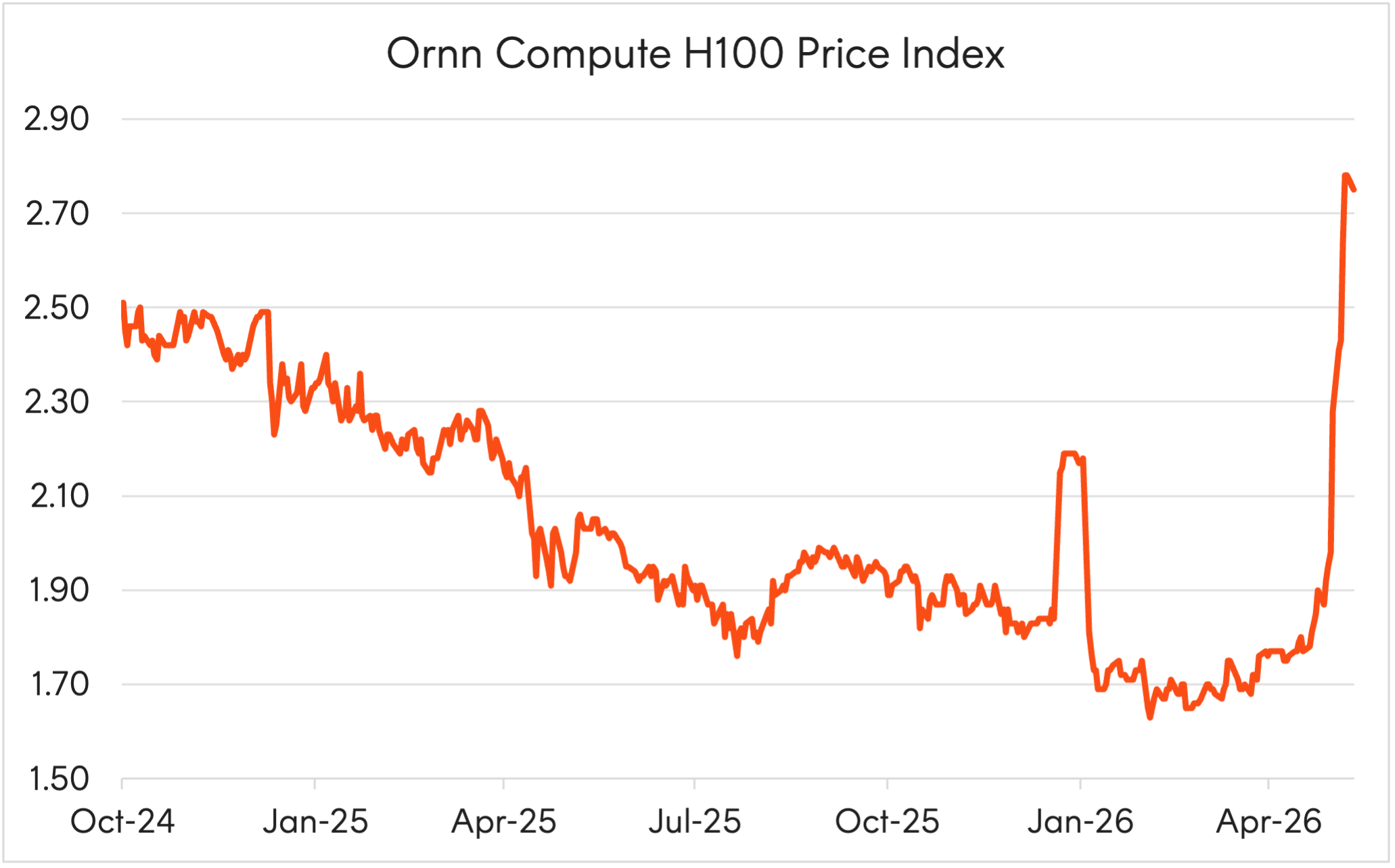

The results speak to AI technologies maturing into new use cases, with users moving away from simple chatbot queries to agentic AI tools that can autonomously execute tasks. These agents are far more token-intensive, driving a surge in demand for compute capacity – as reflected in the following chart showing rental rates on Nvidia’s previous-gen H100 GPUs skyrocketing in recent months.

Source: Bloomberg. As at 11 May 2026.

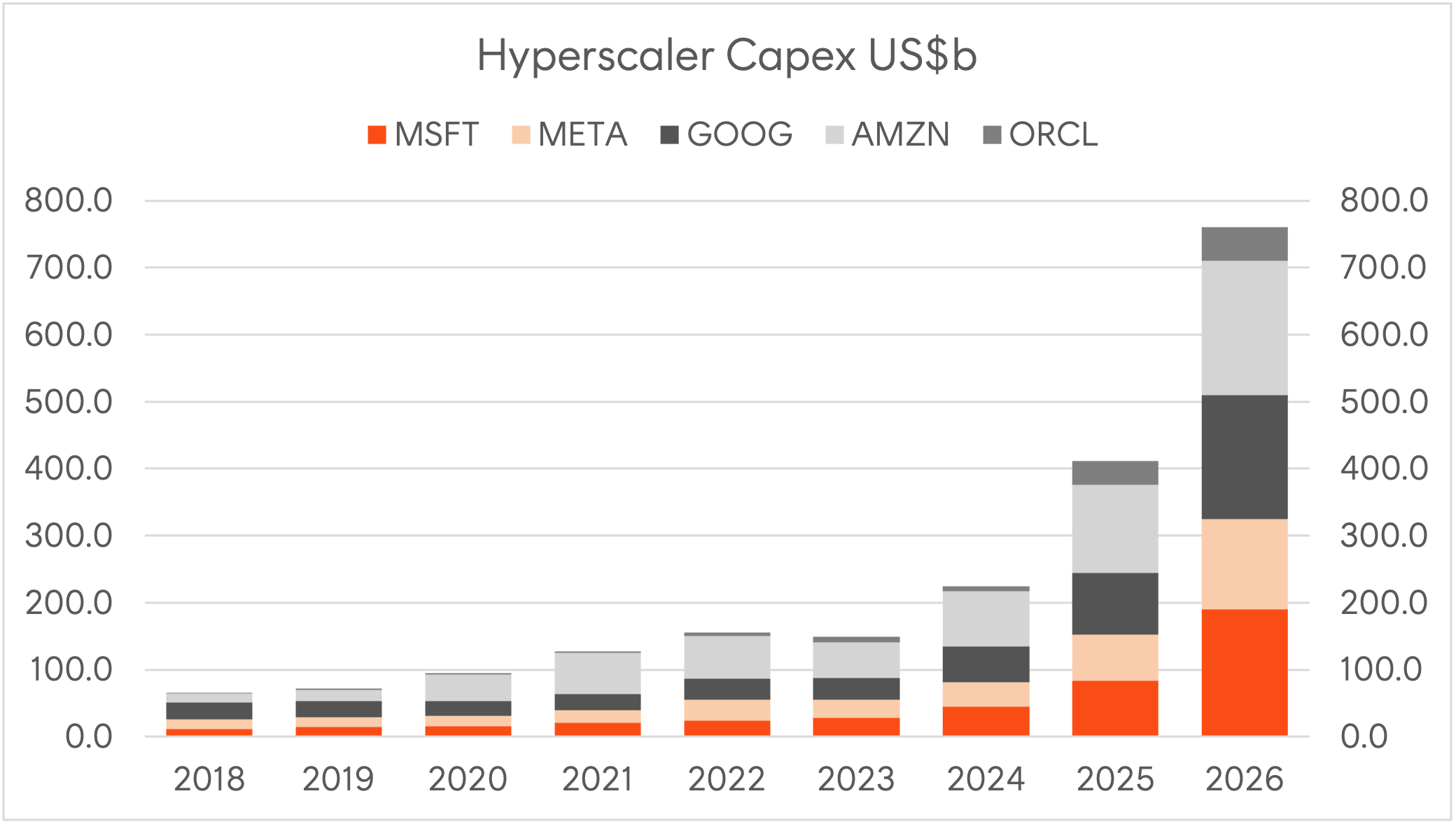

US megacap tech companies, or hyperscalers, then need to devote an ever-increasing amount on capital expenditures to expand compute capacity through data centres. Together, they are forecast to spend north of US$750 billion this year on continuing this AI infrastructure build out.

Source: Company filings. As at 17 May 2026.

This massive infrastructure investment is already paying off. The cloud computing units of Microsoft (Azure), Alphabet (GCP) and Amazon (AWS) – which sell that compute capacity to external customers – are generating close to US$370 billion in annualised revenues while also delivering some remarkable rates of reacceleration during the Q1 2026 period. For example, Google Cloud revenues grew 63% to US$20 billion, while expanding operating margins from 9.4% a year ago to 32.9%.

This positive earnings impulse has likely abated concerns around a capex bubble forming for now, but risks are mounting as AI infrastructure spending continues to be a net drag on free cash flows and has forced the US hyperscalers to tap the debt markets.

That said, these companies remain well capitalised and have some of the most robust balance sheets in the world. Rather than the capital markets, perhaps the bigger constraint may be found in the power and energy markets.

Commodities: the physical backbone of the AI boom

AI data centres are voracious consumers of power, requiring as much electricity as 100,000 households4, and this insatiable demand will likely only continue. Increasingly complex AI workloads—including agentic AI and video generation—drive infrastructure expansion, while efficiency innovations driven by the likes of DeepSeek’s R1 model make advanced capabilities more cost-effective and accessible to deploy.

As a result, there has been an unprecedented shift in energy procurement strategies among the US hyperscalers, with many signing multi-decade contracts for reliable baseload power including:

– Microsoft’s US$16 billion deal with Constellation Energy to restart Pennsylvania’s Three Mile Island nuclear plant

– U.S. utility provider Talen Energy to supply Amazon up to 1,920 megawatts of electricity from its Susquehanna nuclear plant,

– And Google’s multi-pronged approach spanning nuclear SMR technology with Kairos Power and renewable energy deals to offset their carbon footprint and drive down long-term energy costs.

Beyond the popularity of nuclear technologies given their ability to provide consistently high baseload power, other commodities like copper, lithium and liquefied natural gas (LNG) are crucial inputs found within AI data centres. Each stage of the AI compute stack – from power generation and grid connection to backup and cooling – depends on a different commodity with its own supply constraints.

– Copper: Modern AI data centres are highly copper-intensive, requiring roughly 27 to 47 metric tons of copper per megawatt of installed capacity. In addition, decades of underinvestment and Grasberg delays have pushed copper prices to record highs.

– Lithium: Lithium-ion batteries provide backup and buffering power for AI GPU clusters, aiming to keep power stable during sudden load spikes and outages that could interrupt training or inference workloads. With companies building larger clusters such as Huawei’s 10,000-card cluster in Shenzhen5, more lithium-ion batteries need to be deployed.

– LNG: Liquefied natural gas is increasingly being used to power AI data centres given its ability to be stored and transported. With pressure on existing grid infrastructure, LNG can help provide dispatchable power in markets that need faster buildout.

Securing these inputs has become a matter of national strategy – the US Department of Energy’s Critical Minerals and Materials program is one example of governments moving to rebuild domestic supply chains across lithium, copper and rare earths, recognising that AI leadership is inseparable from control over the physical resources that power it.

Investing in a multipolar world: the AI-commodities barbell

In a world increasingly driven by geopolitical events, investors are seeking ways to build more resilient portfolios in this new paradigm.

The fallout of the Iran war highlighted two key themes:

1. Investors are shifting back to the AI and technology hardware theme given the market’s view that companies within this space would either be unaffected or bolstered by the oil supply shock.

2. Energy security has become an even more important consideration particularly for oil-dependent nations in Southeast Asia. Building and securing dominant supply chains beyond fossil fuels in the commodities powering renewable energy like copper, lithium and rare earths is paramount.

But beyond the oil supply shock, these themes are becoming highly interconnected as the US and China shape international trade policy through export controls over rare earth metals and advanced semiconductor chips.

A barbell strategy combining AI hardware exposure with commodities may offer investors access to structural growth themes, while helping anchor portfolios against risks from AI-led disruption and geopolitical shocks.

Rather than concentrating solely in technology, this approach pairs the upside of the AI infrastructure build-out with the physical resources underpinning it – providing a degree of diversification across two sides of the same structural trend.

The following Betashares ETFs offer exposures that may be used by investors to implement an ‘AI-commodities barbell’ approach to portfolio construction:

Please note any information provided is not a recommendation or offer to make any investment or to adopt any particular investment strategy. You should consider seeking financial advice before making an investment decision.

| Artificial Intelligence | Commodities |

|---|---|

| Betashares Nasdaq 100 ETF (NDQ) – provides exposure to 100 largest non-financial companies listed on the Nasdaq market, including many of the the world’s leading AI companies, hyperscalers, and semiconductor manufacturers. Nasdaq has introduced a fast entry rule to accelerate the inclusion of likely new listings from SpaceX, Anthropic and OpenAI shortly after their IPOs. | Betashares Energy Transition Metals ETF (XMET)– provides diversified exposure to global producers of copper, lithium, nickel, rare earths and other critical minerals powering the energy transition and AI infrastructure build out. |

| Betashares Asia Technology Tigers ETF (ASIA) – provides exposure to the 50 largest Asian technology companies (ex-Japan), capturing the semiconductor supply chain including chip manufacturers and AI hardware suppliers across South Korea, Taiwan and China. | Betashares Global Uranium ETF (URNM)– provides exposure to leading uranium miners and physical uranium holders, tapping into the resurgence of nuclear energy as hyperscalers sign multi-decade contracts for reliable baseload power to fuel AI data centres. |

| Betashares Global Energy Companies Currency Hedged ETF (ASX: FUEL)– provides exposure to leading global energy companies. With the Middle East conflict as yet unresolved, the energy sector is being used by some investors as a ‘geopolitical hedge’. Energy is one of the cheaper sectors within the S&P 500, with a 1 year forward PE ratio of 14.5x.6 |

There are risks associated with an investment in the Funds, including market risk, sector risk, concentration risk, international investment risk and oil and gas risk (for FUEL), emerging markets risk (for ASIA), energy transitional metals risk (for XMET) and . Investment value can go up and down. An investment in the Funds should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please see the relevant Product Disclosure Statement and Target Market Determination, both available on this website.

1. https://www.imf.org/en/publications/weo/issues/2026/04/14/world-economic-outlook-april-2026

2. https://www.factset.com/earningsinsight (As at 21 May 2026)

3. Source: Bloomberg. As at 18 May 2026.

4. https://www.iea.org/reports/key-questions-on-energy-and-ai

6. Source: LSEG Datastrea, Yardeni Research (as at 22 May 2026)