Vinnay Cchoda

9 minutes reading time

When we first explored the ’critical minerals arms race’ in early 2023, the dominant narrative centred on accelerating demand for the energy transition colliding with heavily concentrated supply chains, particularly in China.

Three years on, the premise remains valid but has gained new dimensions.

Prices for key battery metals have experienced wild swings, supply chain vulnerabilities have attracted growing attention and critical minerals have transitioned from a niche commodities theme to a central pillar of global industrial strategy and geopolitical competition.1,2,3 Governments are increasingly treating access to critical minerals as a matter of economic security, reshaping trade relationships through export controls, subsidies and strategic alliances.

Accelerating adoption of artificial intelligence (AI), expanding data-centre infrastructure and surging electrification are adding new layers to the demand equation. As underscored by our analysis in 2025, the convergence of AI expansion and the green transition may produce a historic ‘supercycle’ in critical minerals, reshaping industries worldwide and testing supply chains already stressed by renewable energy and electric vehicle (EV) growth.

For investors, the structural demand story remains compelling. But the means of capturing that value has shifted. The path to monetising this megatrend now runs through policy, geopolitics, supply chain diversification and industrial strategy as much as through geology.

What still counts as ‘critical’ – and why it matters now

Geoscience Australia defines a critical mineral as one that is essential to modern technologies, economies or national security – and whose supply faces significant risk of disruption due to geopolitics, trade policy or other factors.4

In practice, that list is expanding. Traditional energy transition materials including lithium, nickel, cobalt, graphite and rare earth elements remain at the core. These minerals underpin EVs, grid-scale batteries, wind turbines and solar PV.5 But policymakers are adding other inputs tied to semiconductors, defence and data centre buildouts, such as gallium, germanium and high-purity alumina.

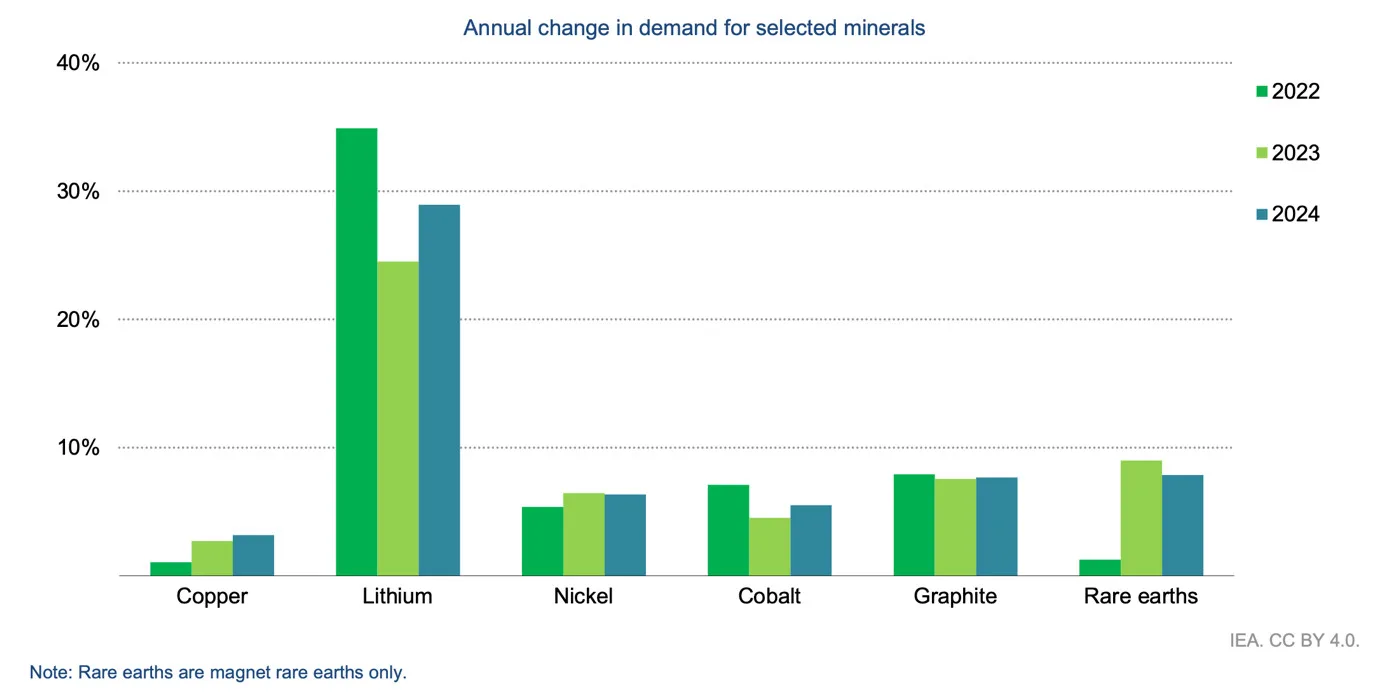

Annual change in demand for select critical minerals

Source: IEA Global Critical Minerals Outlook 2025

The International Energy Agency’s (IEA) Global Critical Minerals Outlook 2025 estimates that demand continued to grow strongly in 2024: lithium demand rose nearly 30%, while nickel, cobalt, graphite and rare earths demand grew 6-8%. This was largely driven by clean energy applications. IEA, in its base-case Stated Policies Scenario, forecasts lithium demand to grow roughly five-fold by 2040, with graphite and nickel demand doubling and copper demand rising by about 30%.6

In other words, the structural demand story remains robust. The more important question is where that supply will come from and on what terms.

Cycles within a supercycle

The last two years have delivered a sharp reminder that structurally rising demand does not guarantee a straight-line price chart.

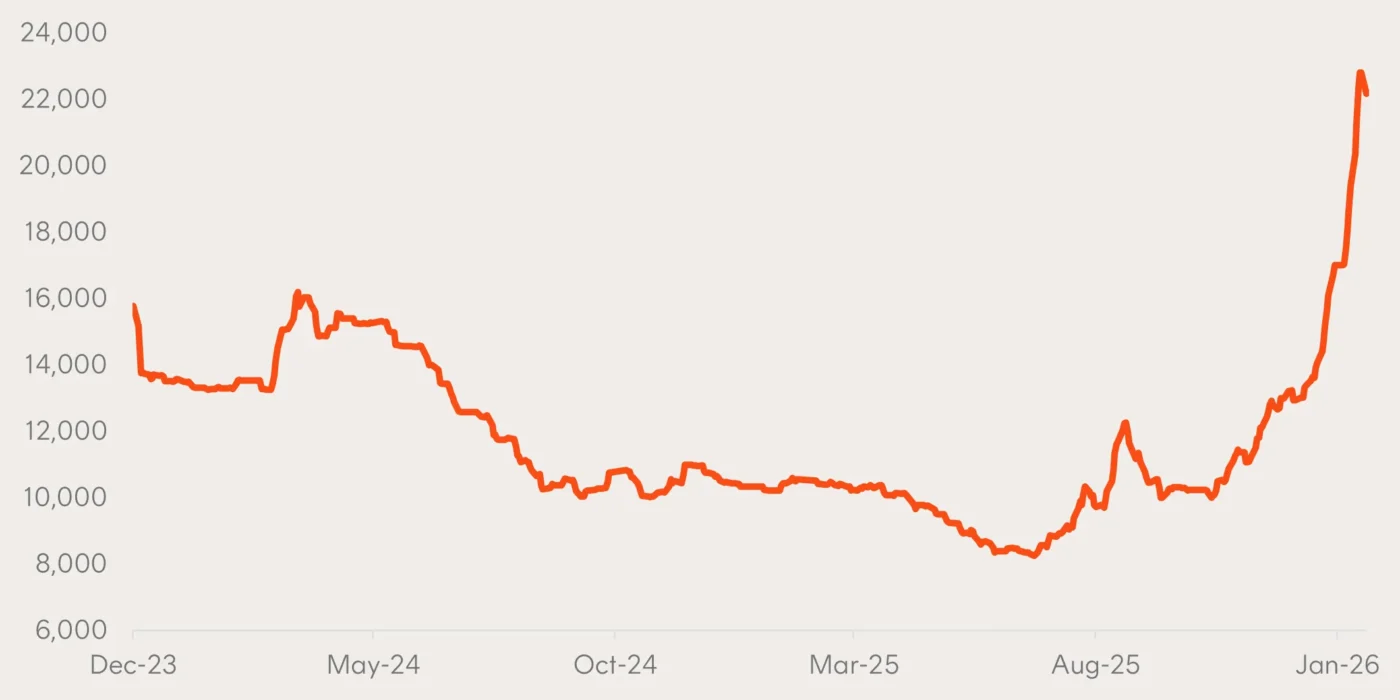

Lithium is the most visible case study. After a spectacular rally in 2021-22, lithium carbonate prices collapsed through 2023-24 due to new supply in China and South America coming online and policy uncertainty in the US. By early 2025, North Asia lithium carbonate prices had fallen below US$10,000 per tonne – their lowest level in four years, prompting production cuts and project deferrals.7

Since mid-2025, however, the market perception has shifted towards that of a recovery. Multiple analysts now say a medium-term deficit is emerging as storage demand accelerates and marginal projects are shelved. Lithium carbonate prices have rebounded materially year-to-date, supported by inventory drawdowns and ongoing growth in both EV and battery storage markets.8

Lithium Carbonate 99.5% Price (US$ per tonne)

Source: Bloomberg, as at 19 January 2026

Similar patterns are evident elsewhere.

Cobalt and nickel have wrestled with oversupply and substitution risk, while copper has rallied on expectations of grid expansion, data centre demand and electrification targets which look increasingly incompatible with current mine pipelines.9

Copper price trend (LME US$ per tonne)

Source: Bloomberg, as at 19 January 2026

For investors, the lesson is that critical minerals are not a single trade. They are a collection of markets, each with its own cost curve, technology risk and capital-cycle dynamics. In addition, those factors are often overlaid with policy decisions which could potentially change an investment case overnight. Diversification within critical minerals is essential to capturing the long-term supercycle while managing the short-term cycles which arise within it.

The AI multiplier effect

In 2023, the investment case for critical minerals was largely linear. Decarbonisation required more metals. Three years later, that narrative looks incomplete.

Artificial intelligence has emerged as a powerful second driver of demand. Hyperscale data centres, high-performance computing and the associated expansion of electricity grids are materially increasing the need for copper, aluminium and battery materials. AI does not displace the energy transition – it amplifies it by adding a technology-driven layer of demand to systems already under strain.

The scale of infrastructure required is significant. Data centres are energy-intensive assets that often require dedicated grid upgrades, backup power and substantial cooling capacity. Building and operating this infrastructure is metal-intensive, particularly for copper and silver. It is also increasingly reliant on battery storage to manage peak loads and reliability.

This creates a compounding effect. We are not merely building batteries for cars; we are now building the backbone of what comes after the internet.

Strategic realignment creates new investment opportunities

China controls roughly two-thirds of global nickel refining, close to 60% of lithium refining, about 70% of cobalt refining and most rare earth separation capacity.

As such, China has become a catalyst for a far-reaching realignment of global supply chains.

Since 2023, it has introduced export controls on natural and synthetic graphite, gallium, germanium and other dual-use materials, as well as advanced lithium-ion battery technologies and key manufacturing equipment. While some of these measures were later moderated during trade negotiations, the underlying message was clear: critical minerals are now instruments of geopolitical leverage.

Critical minerals refined production by country

Source: IEA Critical Minerals Outlook 2025

However, rather than inhibiting investment, these actions have accelerated diversification.

The US has raised tariffs on Chinese electric vehicles, lithium-ion batteries and processed minerals. It has also imposed anti-dumping duties on Chinese graphite and formally identified reliance on imported critical minerals as a national security risk. 10, 11 This assessment has prompted President Donald Trump to flag potential action under Section 232, including minimum import prices and targeted tariffs aimed at countering artificially low-priced supply from non-allied countries.12

Meanwhile, Europe’s Critical Raw Materials Act is setting binding targets for domestic extraction, processing and recycling, while limiting reliance on any single foreign supplier. 13 The US is also expected to convene allied foreign ministers in early February to coordinate efforts to reduce dependence on China.14 Collectively, these developments are redirecting capital toward allied jurisdictions with stable regulatory frameworks. These include Australia, Canada, Chile and Peru.

Australia’s position: From quarry to strategic partner

The Australian Government’s Critical Minerals Strategy 2023-2030 explicitly seeks to move the country up the value chain, using public financing and policy support to encourage processing, refining and downstream manufacturing, rather than relying solely on exporting raw ore.15

Canberra has backed this ambition with capital. In 2023, it doubled its Critical Minerals Facility to $4 billion, providing low-cost loans to miners and processors, building on earlier support for projects such as Iluka Resources’ Eneabba rare earths refinery in Western Australia.16

Australia has also leaned into strategic partnerships. The 2023 Australia-US Climate, Critical Minerals and Clean Energy Transformation Compact and the 2025 US-Australia Framework for Securing the Supply of Mining and Processing of Critical Minerals and Rare Earths seek to integrate parts of the two countries’ supply chains and provide clearer demand signals for Australian projects.17

Canberra’s Critical Minerals Strategy 2023-2030 makes explicit what had long been implicit: the aim is not just to export more ore, but to reposition Australia as a “secure, reliable and ethical supplier” and to move down the value chain into processing and advanced materials.18 The strategy is backed by the Future Made in Australia agenda and targeted public finance, particularly through the National Reconstruction Fund Corporation (NRFC).19

Taken together, these measures give Australia more than just the familiar role of ‘quarry to the world’. If executed well, Australia can become a core partner in allied industrial policy, not only by supplying raw materials but by hosting separation, refining and component manufacturing that are increasingly treated as strategic assets by the US, Japan, South Korea and the EU.

The path forward for investors

The energy transition is now firmly embedded in the global investment landscape, with critical minerals central to the technologies underpinning electrification, decarbonisation and digital growth.

Demand for copper, lithium, nickel and rare earths is expected to rise materially as renewable energy, EVs and AI infrastructure scale simultaneously. Data centres, grid upgrades and battery storage are placing additional strain on mineral supply chains already shaped by years of underinvestment and concentrated processing capacity. As these forces converge, supply constraints are becoming more visible, reshaping commodity markets and industrial strategy globally.

For Australian investors seeking exposure to this long-term thematic, XMET Energy Transition Metals ETF provides access to a portfolio of global producers supplying the metals critical to both the energy transition and digital economy. While still an emerging investment theme, XMET delivered a 95% return to investors in calendar 2025 and has returned 21% p.a. since inception in October 2022.

XMET Energy Transition Metals ETF focuses on ‘pure play’ critical mineral mining companies and producers that have at least 50% of their revenue generated from one of the eight key energy transition metals. Also included are companies involved in the exploration, recycling and processing of these minerals. The critical minerals XMET provides exposure to are copper, lithium, nickel, cobalt, graphite, manganese, silver and rare earth elements.

There are risks associated with investment in the Fund, including market risk, international investment risk, commodity price and ETM company related risks, and concentration risk. The Fund’s returns can be expected to be more volatile (i.e. vary up and down) than a broad global shares exposure, given its concentrated exposure. The Fund should only be considered as a component of a diversified portfolio, given its concentrated exposure. For more information on risks and other features of the Fund, please see the Target Market Determination (TMD) and Product Disclosure Statement, available at www.betashares.com.au.

Source:

1. https://www.reuters.com/world/asia-pacific/goldman-sachs-flags-risk-disruption-supply-rare-earths-key-minerals-2025-10-21/ ↑

2. https://www.gtlaw.com.au/insights/key-topics/beyond-transition/paradigm-shift ↑

3. https://iea.blob.core.windows.net/assets/ef5e9b70-3374-4caa-ba9d-19c72253bfc4/GlobalCriticalMineralsOutlook2025.pdf ↑

4. https://www.ga.gov.au/scientific-topics/minerals/critical-minerals? ↑

5. Solar PV (photovoltaic) is a technology that converts sunlight directly into electricity using semiconductor cells. ↑

6. https://iea.blob.core.windows.net/assets/ef5e9b70-3374-4caa-ba9d-19c72253bfc4/GlobalCriticalMineralsOutlook2025.pdf ↑

7. https://carboncredits.com/lithium-prices-crash-below-10k-hitting-a-4-year-low-will-the-market-rebound/ ↑

8. https://carboncredits.com/lithium-prices-surge-amid-strong-demand-forecasts-could-reach-up-to-28000-ton-by-2026-nili/ ↑

9. https://www.theguardian.com/business/2025/dec/29/copper-price-rise-shortage-renewable-energy-silver-gold ↑

10. https://www.reuters.com/markets/us/us-announces-details-higher-china-tariffs-some-start-aug-1-2024-05-22/ ↑

11. https://www.reuters.com/world/china/us-commerce-dept-sets-935-anti-dumping-tariff-chinese-anode-graphite-2025-07-17/ ↑

12. https://www.whitehouse.gov/presidential-actions/2026/01/adjusting-imports-of-processed-critical-minerals-and-their-derivative-products-into-the-united-states/ ↑

13. https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/critical-raw-materials/critical-raw-materials-act_en ↑

14. https://www.bloomberg.com/news/articles/2026-01-15/us-asks-allies-to-step-up-measures-on-chinese-critical-minerals ↑

15. https://www.rba.gov.au/publications/bulletin/2025/oct/the-global-energy-transition-and-critical-minerals.html ↑

16. https://www.betashares.com.au/insights/critical-minerals-arms-race/ ↑

17. https://www.whitehouse.gov/briefings-statements/2025/10/united-states-australia-framework-for-securing-of-supply-in-the-mining-and-processing-of-critical-minerals-and-rare-earths/ ↑

18. https://www.industry.gov.au/publications/critical-minerals-strategy-2023-2030? ↑

19. https://www.rba.gov.au/publications/bulletin/2025/oct/pdf/the-global-energy-transition-and-critical-minerals.pdf ↑