David Bassanese

7 minutes reading time

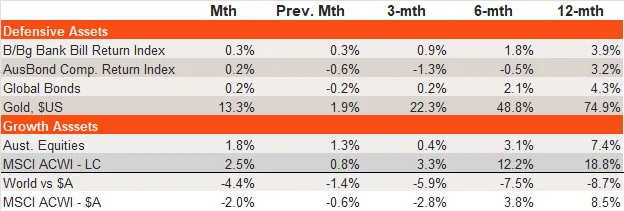

Major asset class performance

- Global and local equities produced further positive returns in January, supported by a solid earnings outlook and still reasonably steady bond yields. However, a rising Australian dollar hurt global equity returns in unhedged AUD terms.

- Among defensive assets, more modest gains came from fixed-rate bonds while gold enjoyed another strong month.

- An upsurge in various geopolitical risks – from Venezuela to Iran and Greenland – dominated the headlines but quickly died down as markets reacted. Despite some slowing in the labour market, US economic growth remains robust and inflation still broadly steady.

- The US Federal Reserve held rates steady in January, although the market still expects further rate cuts later this year.

Source: Bloomberg, Betashares. Cash: Bloomberg Australian Bank Bill Index; Australian Bonds: Bloomberg AusBond Composite Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged); Gold: Spot Gold Price in $US; Australian Equities: S&P/ASX 200 Index; Global Equities: MSCI All-Country World Index in local currency and $A currency (unhedged) terms. Past performance is not indicative of future performance.

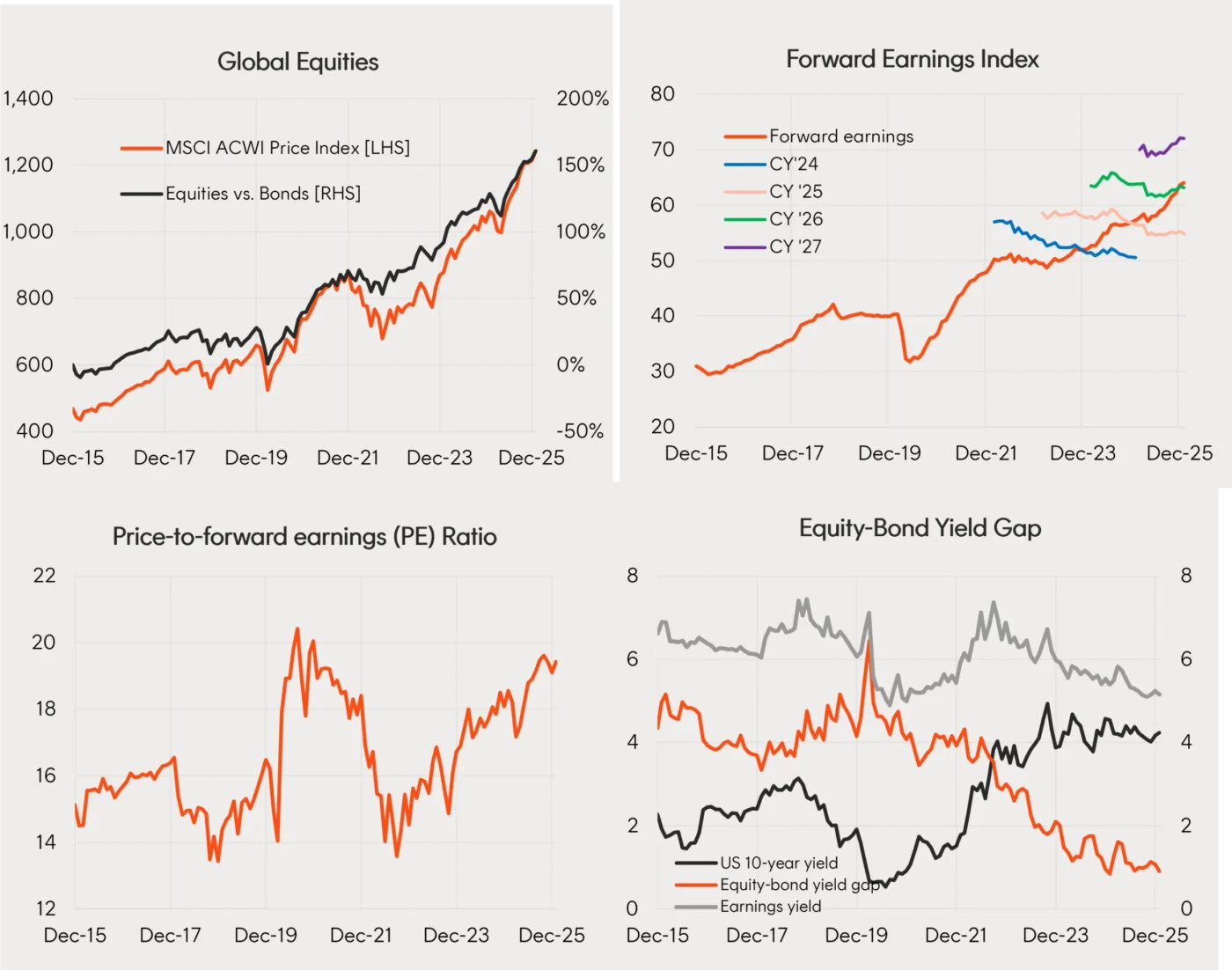

Global equities

- Global equities have started 2026 on a solid footing, with the MSCI All-World Equity Index returning 2.5% in local currency terms, after a 0.8% gain in December. The gain reflected further 0.7% lift in forward earnings and a 1.7% rise in the price-to-forward earnings ratio to 19.4.

- Equity valuations were supported by relatively steady bond yields, with US 10-year bond yield up only 0.07% to 4.25%.

- Reflecting strength in the Australian dollar, however, global equity returns in unhedged Australian dollar terms declined by 2.0%.

- Earnings expectations remain upbeat, with 12.5% expected growth in forward earnings by end-2026.

- With valuations elevated, continued market gains are still possible, provided bond yields don’t rise much and/or the current bullish earnings outlook remains in place.

Source: Bloomberg, LSEG, Betashares. Global Equities: MSCI All-Country World Index. Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged). You cannot invest directly in an index. Past performance is not an indicator of future performance.

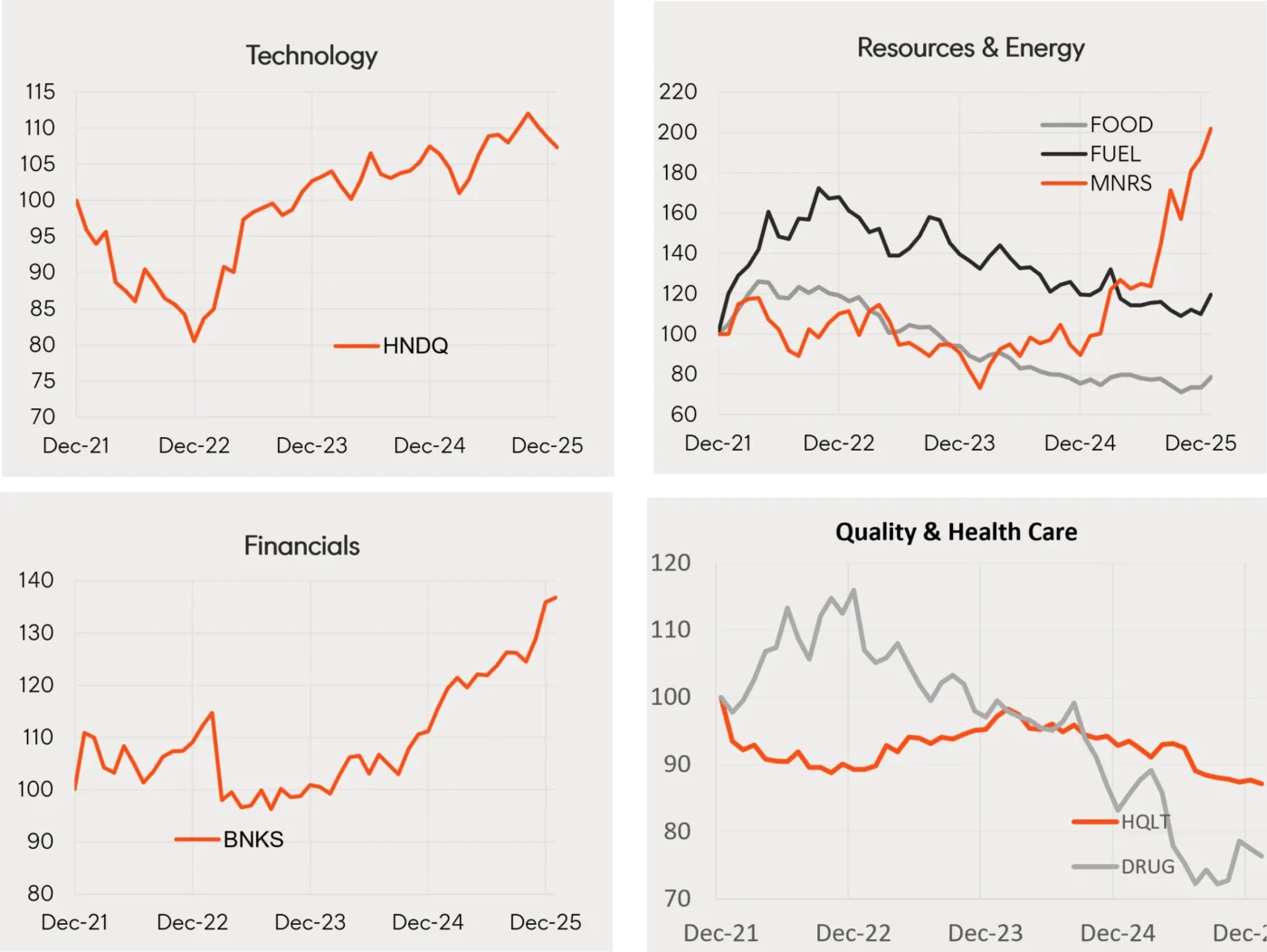

- Within global equity markets, a rotation in relative performance from US/growth/large cap/technology stocks into non-US/value/small cap stocks has been evident in recent months. Japan and emerging markets have performed especially well, along with resource and energy stocks.

- Among select Betashares global equity ETFs, global gold miners (MNRS) and banks (BNKS) are performing well, with a pull back in relative performance of the Nasdaq-100 (HNDQ) in recent months.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the MSCI All-Country World Index (local currency terms) for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.

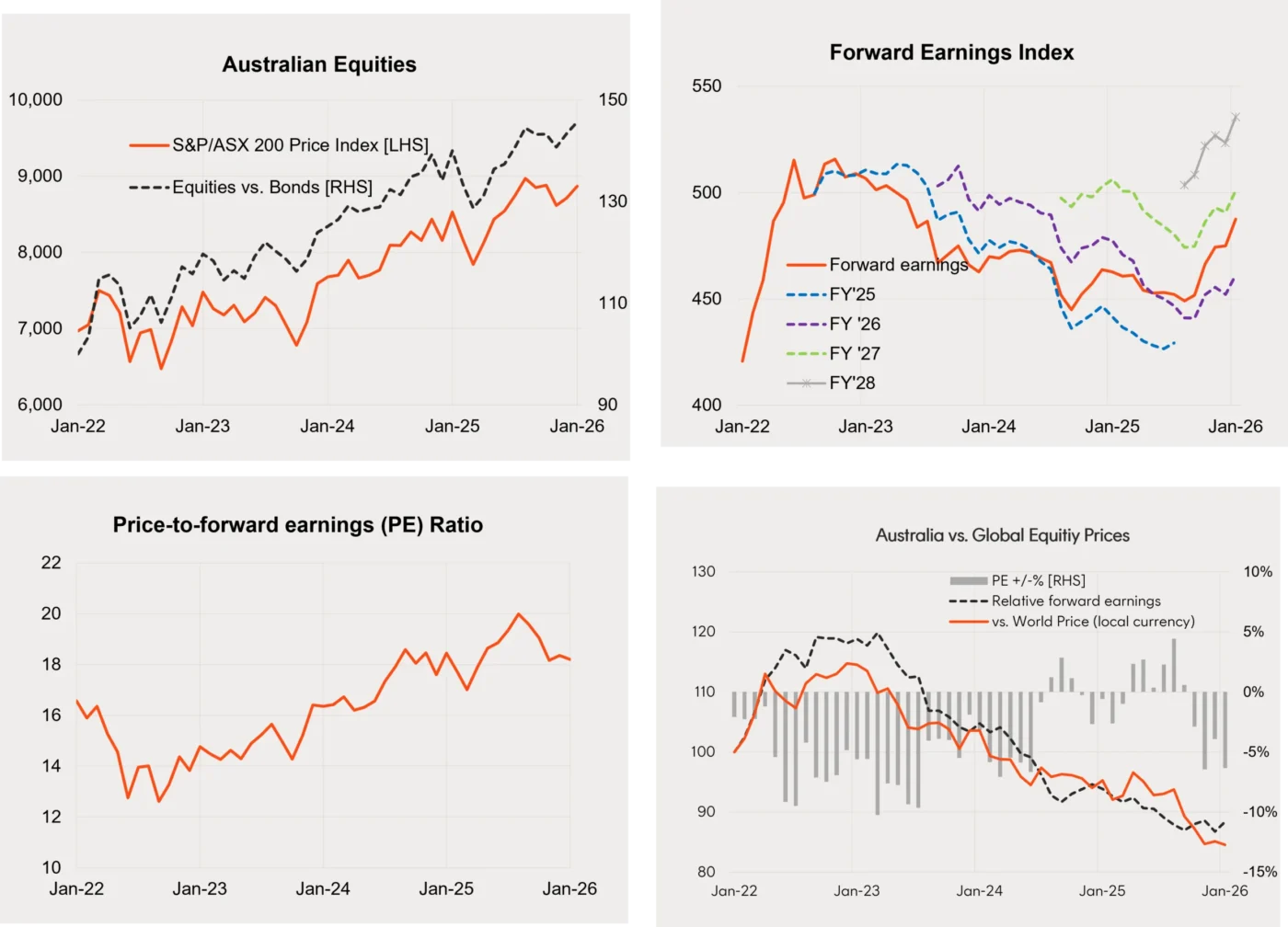

Australian shares

- Australia shares modestly underperformed local currency global equity returns in January, with the S&P/ASX 200 returning 1.8%. Despite a solid 2.6% gain in forward earnings, market gains were held back by a 0.9% decline in the price-to-forward earnings ratio to 18.2. Pessimism around a possible RBA rate hike likely hurt investor sentiment.

- January saw a further lift in earnings expectations. Current earnings expectations imply 6.3% growth in Australian forward earnings by the end of 2026 – which is about half of what is expected for global earnings. Weaker expected earnings growth in the financials and energy/materials sectors compared to global peers are the main local drags.

- Australian equities ended the month trading at a modestly cheap 6.2% discount to global equities.

- Despite the weaker earnings outlook, the now-cheaper relative valuation for Australian equities has improved their year-ahead relative return outlook to a more neutral setting.

- That said, while the return outlook appears more encouraging, the RBA’s tightening bias is a counterweight.

Source: Bloomberg, LSEG, Betashares. Australian Equities: S&P/ASX 200 Index. Australian Bonds: Bloomberg AusBond Composite Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

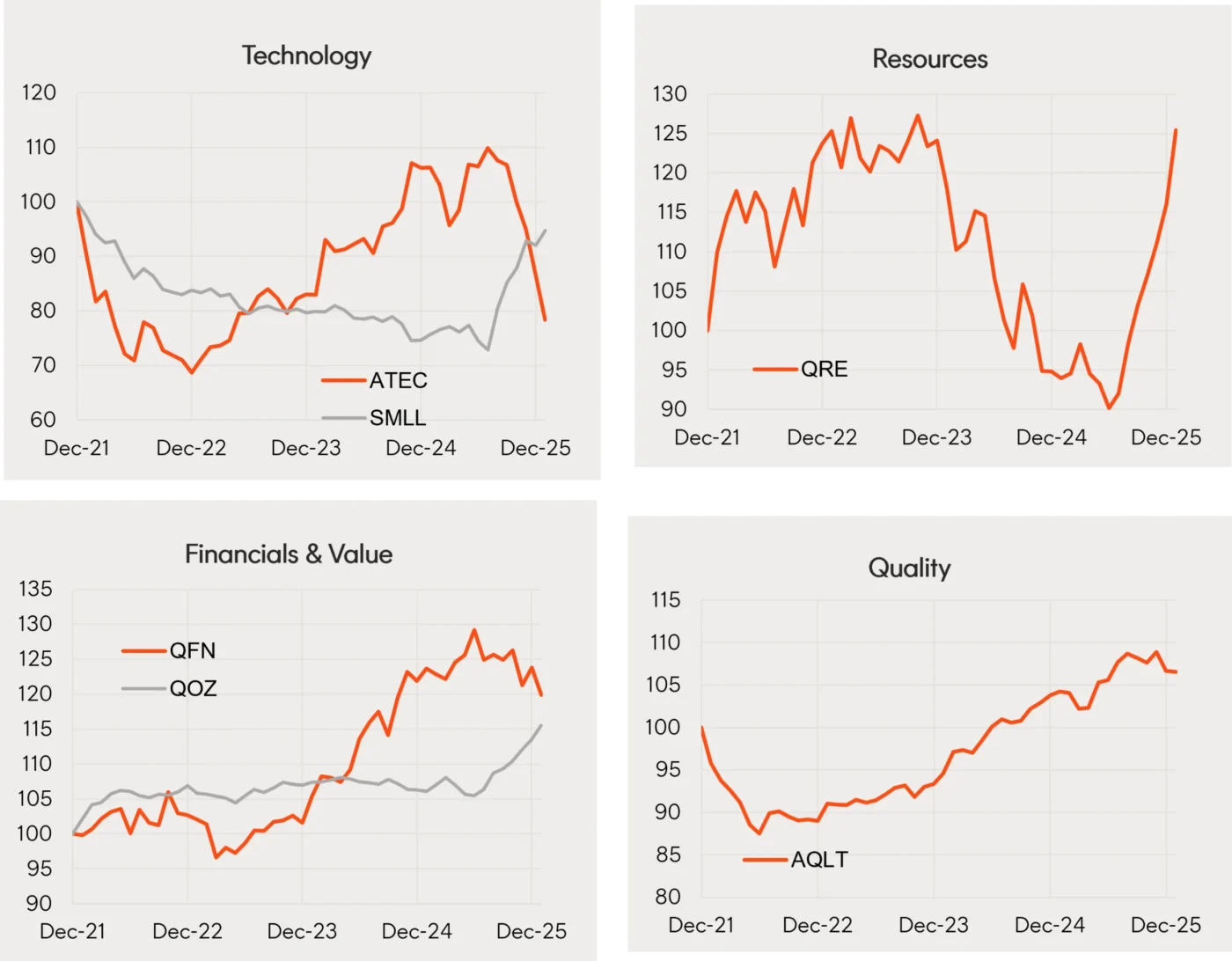

- Diminished local rate cut expectations and global AI jitters again hurt the high-beta technology sector (ATEC) in January while small caps (SMLL) held up well.

- More broadly, the rotation toward resources (QOZ) and away from financial stocks remained evident. Quality (AQLT) continues to hold up reasonably well.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the S&P/ASX 200 Index for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.

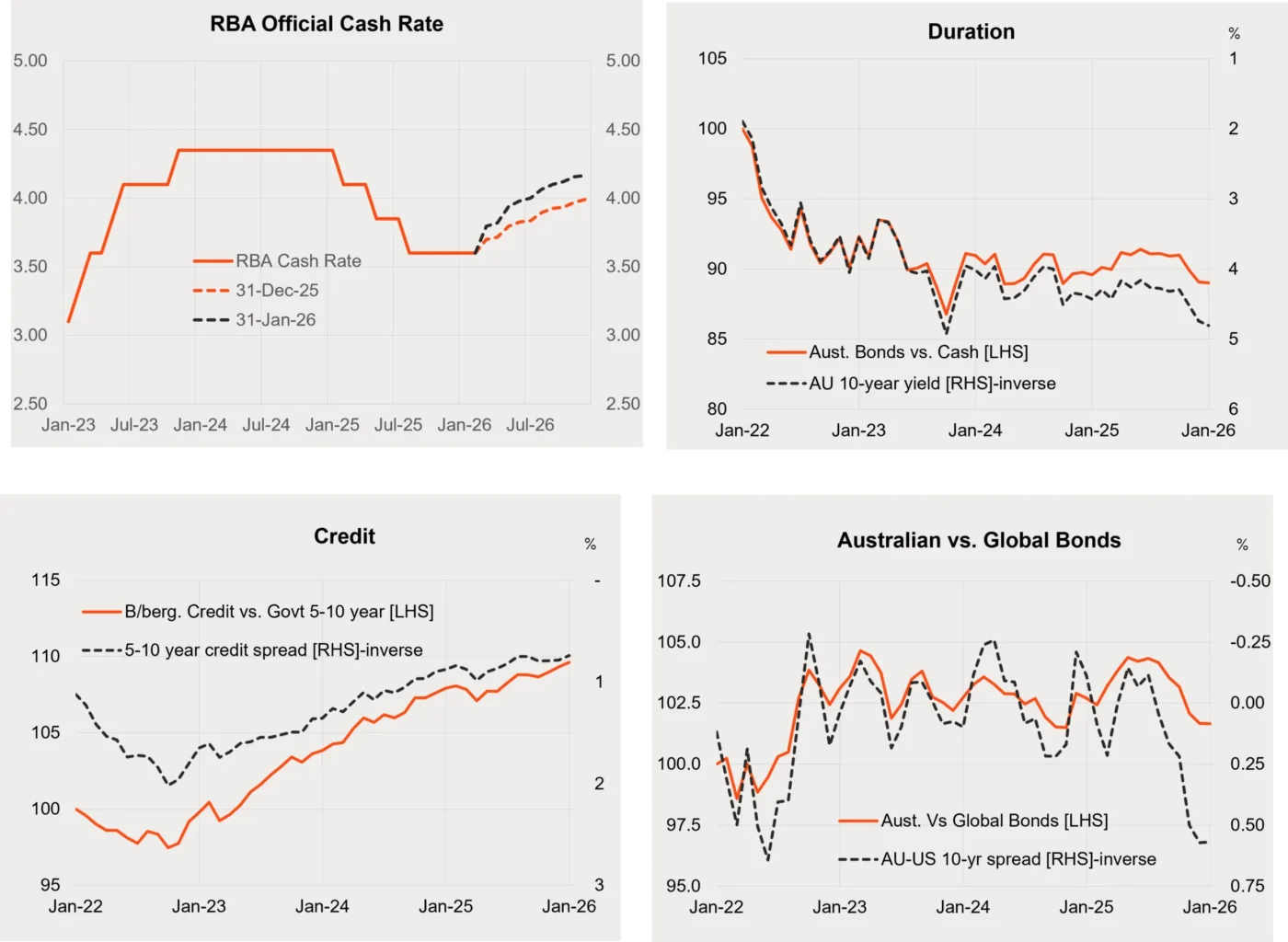

Fixed-rate bond trends

- Local rate cut expectations shifted up further in January, following the firm Q4 CPI report and December labour market report. Two rate hikes (with a modest chance of a third) are currently priced for this year.

- In the US, by contrast, rate cut expectations shifted only marginally, with two rate cuts still expected for this year.

- Local 10-year bond yields rose only 0.07% to 4.24%, however, and remain in the range they’ve held since early 2024. This has resulted in choppy relative performance of bonds relative to cash returns over this period.

- Longer-term credit spreads have levelled out in recent months, allowing corporate bonds to continue to modestly outperform government bonds.

- A widening in Australian versus global bond yields in recent months has seen local bonds underperform their global peers, although relative performance has been in a choppy sideways range for two years.

Source: Bloomberg, Betashares. Australian bonds: Bloomberg AusBond Composite Bond Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged).

Australian dollar

- Firmer iron-ore prices, a weaker US dollar and a notable widening in the short-term interest rate differential against the US have all helped push up the Australian dollar over recent months.

- The 12-month forward expected cash rate in Australia – relative to that expected in the United States – has moved from -0.6% in July last year to +1% by the end of January 2026. Over the same period, the US Dollar Index against major global currencies has eased 2.6%, while the iron ore price rose 6.7% to US$104/tonne.

- As a result, the Australian dollar has rallied from 64.3 US cents in July last year to 69.6 US cents by the end of January.

- More US rate cuts and the still relatively expensive US dollar suggests the Australian dollar could strengthen further in coming months.

Source: Bloomberg, LSEG, Betashares. Australian Equities: S&P/ASX 200 Index. Australian Bonds: Bloomberg AusBond Composite Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.