David Bassanese

7 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

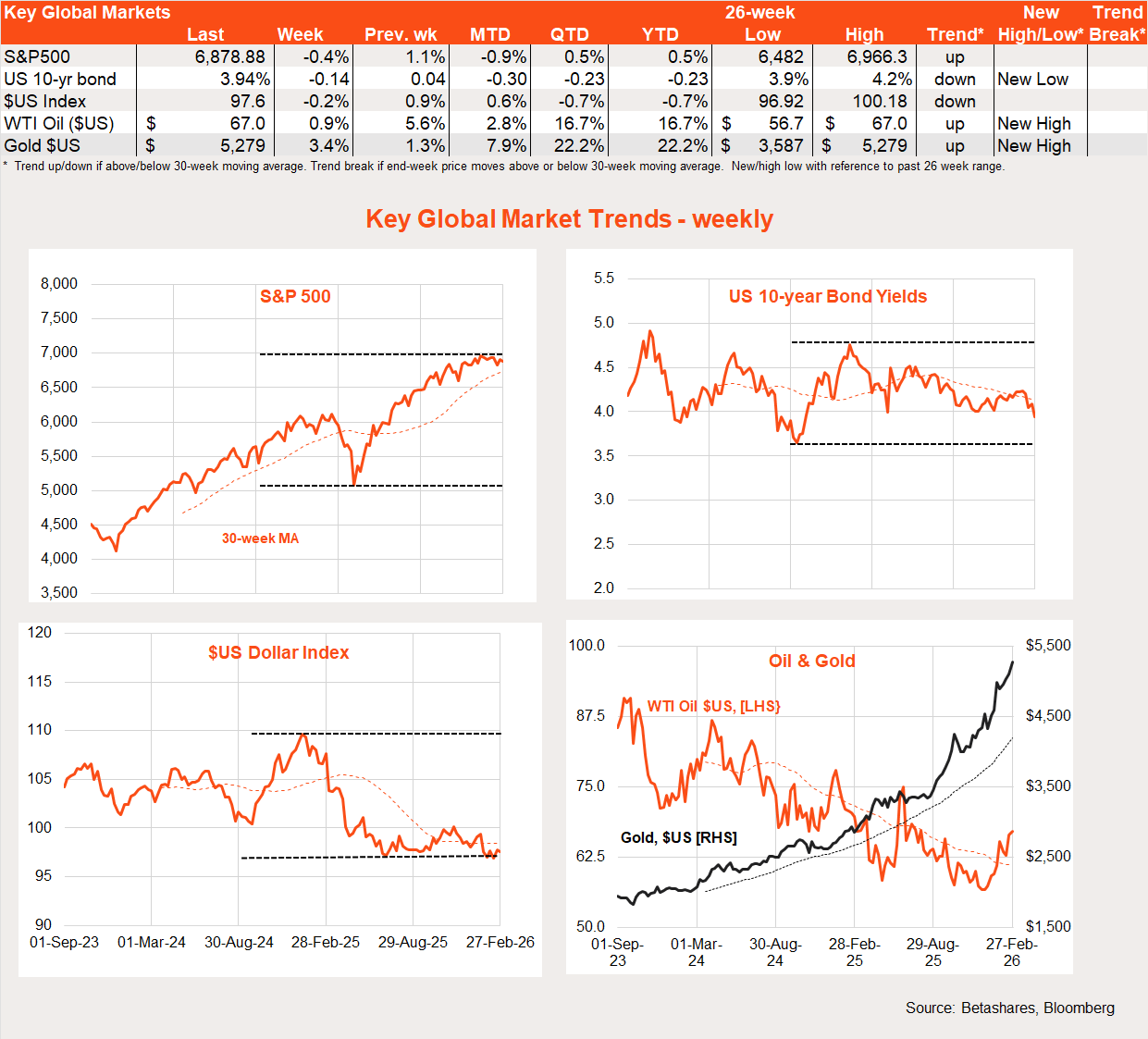

Before the attack on Iran, US stocks edged lower last week, reflecting lingering AI disruption fears.

Global week in review: AI fears persist

There was little in the way of major global economic news last week, with equities generally on the defensive after a nervous bounce higher over the previous week.

US economic data was generally upbeat – a welcome bounce was seen in US consumer confidence in February (albeit from still low levels) along with a higher-than-expected producer price report. Fed rate cut expectations barely flinched.

Markets generally remained fixated on the AI fallout. Nvidia (NASDAQ: NVDA)‘s earnings result was much better-than-expected once again, although it was not good enough to avoid a 5% post-result share price decline. Investors fretted over the sustainability of the surge in AI-related data centre/chip demand. In related news, Meta has agreed to buy US$60 billion of rival chip maker AMD’s offerings, whilst also taking a 10% ownership stake in the company. This has been seen by the market so far as a general vote of confidence in the AI boom.

Outside of the US, the Japanese Government’s appointment of two academic ‘monetary doves’ to the Bank of Japan board raised some concerns over whether the BOJ will remain diligent in containing inflation. The Japanese 10-year bond yield briefly dipped on the news, although it ended the week unchanged at 2.12%. The market still expects two further rate hikes this year, with the next one in July.

Of course, the big news of the week was the US missile strike on Iran over the weekend, which in early Monday trading triggered a not entirely surprising fall in equity prices and bond yields.

At the time of writing, S&P 500 futures were off 1% while the S&P/ASX 200 was down 0.5%. Oil and gold prices have lifted 13% and 1.6% respectively, while the US dollar has also caught a safe-haven bid at the expense of the Australian dollar, which has dropped to 70.64 US cents.

Global week ahead: Iran & payrolls

The coming week is likely to be dominated by the Iran conflict – will it be quickly contained, with Iran agreeing to a deal, or will it spread with Iran digging in and launching more devastating counter-attacks than the ones seen to date?

Judging by events in Venezuela, Trump may not insist on regime change per se, given how difficult it is to engineer without placing boots on the ground – especially if Iran quickly rolls over and agrees to a new nuclear deal. Iran’s counter attacks so far have been relatively limited, suggesting it may only be able to put up limited resistance, which may encourage the US to continue pressing its advantage.

One near-term risk is a blockade of the Strait of Hormuz, where 20% of global oil supply flows through. Iran has reportedly declared the trade route “closed“, although effective enforcement remains unclear – especially with the US targeting Iranian warships. Even without a formal blockade, however, oil-related transport costs are likely to rise given shipping companies may re-route to alternative, more expensive routes and freight insurance costs are likely to surge.

Likely of secondary importance this week will be Friday’s US payrolls report, with a modest 58k gain in jobs during February expected, which should keep the unemployment rate steady at 4.3%.

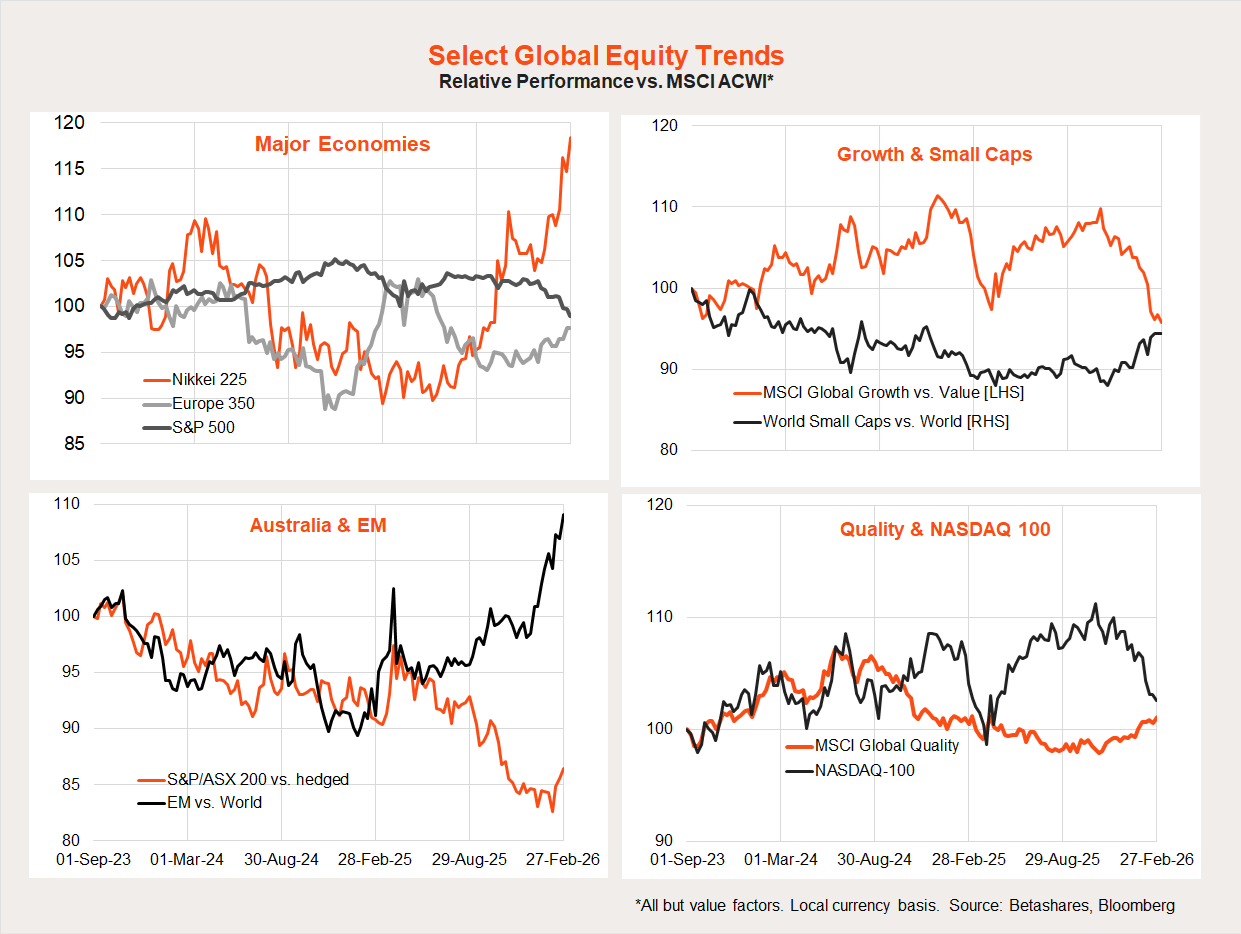

Global equity trends: the great rotation continues

The MSCI All-Country World Equity Index rose 0.3% last week, modestly outperforming the US market – led by solid gains in Japan and emerging markets. The NASDAQ-100 slipped 0.2%, slightly less than the S&P 500.

That said, the great rotation remains in place. Since the end of October 2025, we’ve seen underperformance of US/growth/technology, replaced by strength in Japan, emerging markets and small caps. There are also tentative signs of a bottoming out in the underperformance of the Australian market. Despite the US tech underperformance, global quality (among factors) is also holding up reasonably well.

As we saw in 2022, if a global energy shock plays out, there may be a further rotation from interest rate-sensitive cyclical and technology sectors into more value-orientated defensives and resources.

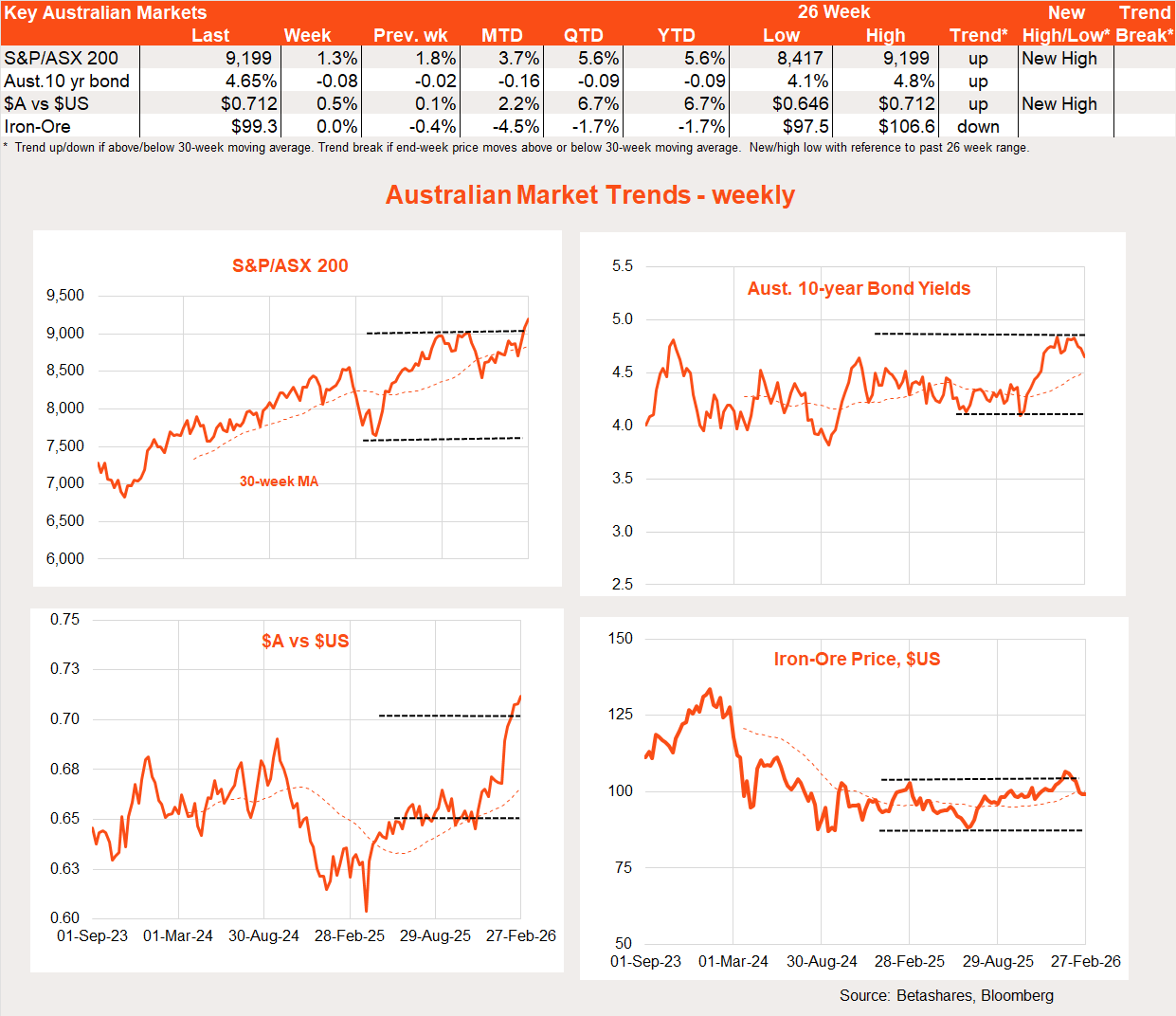

Australian week in review: still firm employment

Despite local interest rate fears, Australian shares enjoyed another decent bounce last week, with the S&P/ASX 200 further moving north of the 9,000 level. Defensive companies and resources generally fared best, with materials and consumer staples returning 7.4% and 5.0% respectively. That said, the beaten-down technology sector bounced for the second week in a row.

The main news last week was another firm monthly consumer price index (CPI) report, with annual trimmed mean inflation edging up to 3.4% from 3.3%. As I argued last week, while the monthly figures need to be taken with a grain of salt, the apparent broad-based firmness in prices does not bode well for a benign Q1 CPI report in late April.

Other economic data was also generally firm:

Total Q4 construction spending was weaker than expected, although this reflected a winding down in several public infrastructure projects offset by ongoing strength in private residential and non-residential building.

Meanwhile, private Q4 capital spending was firmer-than-expected – strength in non-mining construction activity was partly offset by a pullback in data centre related spending on machinery and equipment.

All up, housing and business investment appears to have held up well in Q4.

Australian week ahead: Q4 GDP

Hot off the press this morning, national capital city house prices rose a further 0.7% in February, although the most strength is being seen in the cheaper cities outside of Sydney and Melbourne. The RBA’s rate hike last month is likely to see a broader cooling in prices in the months ahead.

The local highlight this week will be Wednesday’s Q4 GDP report. The market anticipates a solid 0.7% gain following the 0.4% Q3 gain, with signs of ongoing broad-based strength in private demand (consumer spending, housing and business investment).

Given the RBA’s intense focus on capacity constraints, further evidence of solid Q4 domestic demand (which rose 1% in Q3) will add to the pressure for another rate hike – although I still see the next move in May (after the Q1 CPI report) rather than this month.

With regards to the Iran conflict, implications for the RBA would be fairly mixed – higher global energy prices would be a negative for consumer spending and sentiment, while also placing upward pressure on headline inflation (fuel accounts for 3% of the CPI). On balance, however, heightened geopolitical tensions – if they persisted and escalated – would tend to make the RBA less likely to hike rates amidst such uncertainty.

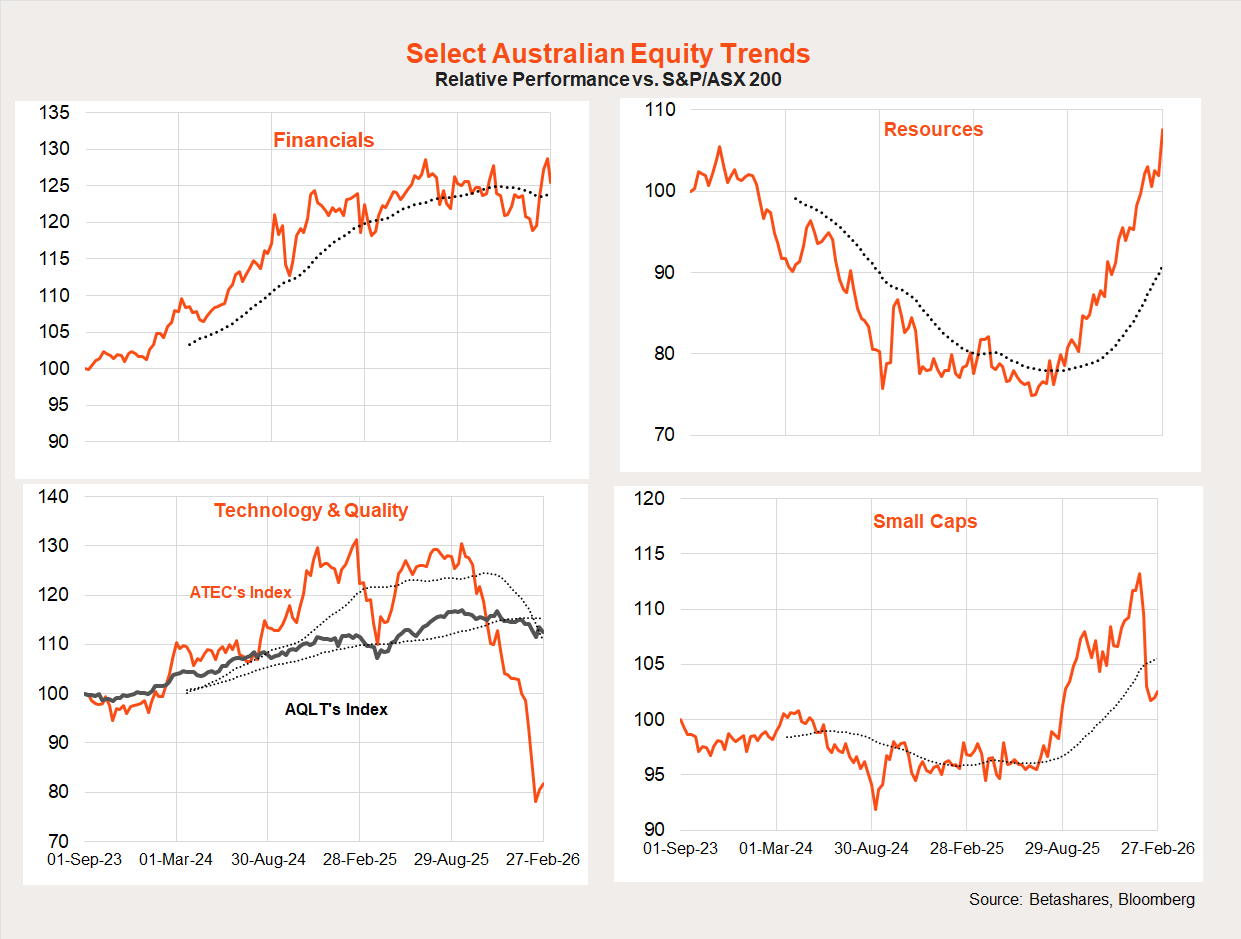

Australian equity trends

Resources continue to go from strength to strength in the local market, with financials experiencing a range bound relative performance. We’ve seen a tentative bounce in the (likely oversold) technology and small cap space in recent weeks, likely reflecting bargain hunting among stocks judged to have been unfairly sold down by AI disruption fears.

Have a great week!