Are you outsmarting yourself?

The best investors aren’t necessarily the busiest. Three common mistakes that could be costing you returns.

What does the perfect investor look like?

Do they read market research reports and tinker with their investments to adapt to every market movement? Do they constantly add new stocks and ETFs to keep up with the latest trends?

These investors exist. And despite all that effort, many of them still struggle to beat a simple index fund that follows a clear set of rules. Even professional investors find this hard: according to S&P Global data from 2025, only 13% of actively managed general Australian equity funds outperformed the S&P/ASX 200 over the past 15 years.

“Many investors still struggle to beat a simple index fund that follows a clear set of rules. ”

Building your investing knowledge and staying up to date on financial news are good practices, but there’s a difference between knowing a lot and doing a lot. Often, the best thing smart investors can do is stay out of their own way.

Here are three ways investors outsmart themselves and how to avoid them.

Trading too much

Our perfect investor is plugged into the news, and doing nothing in the face of major events can feel irresponsible. Social media and a 24-hour news cycle ensure we are bombarded with potentially tradeable news and, when your money’s on the line, the temptation to act is strong.

But in investing, more action doesn’t always mean better results. Transaction costs, poor timing, cash drag and emotional decisions all stand to reduce your returns.

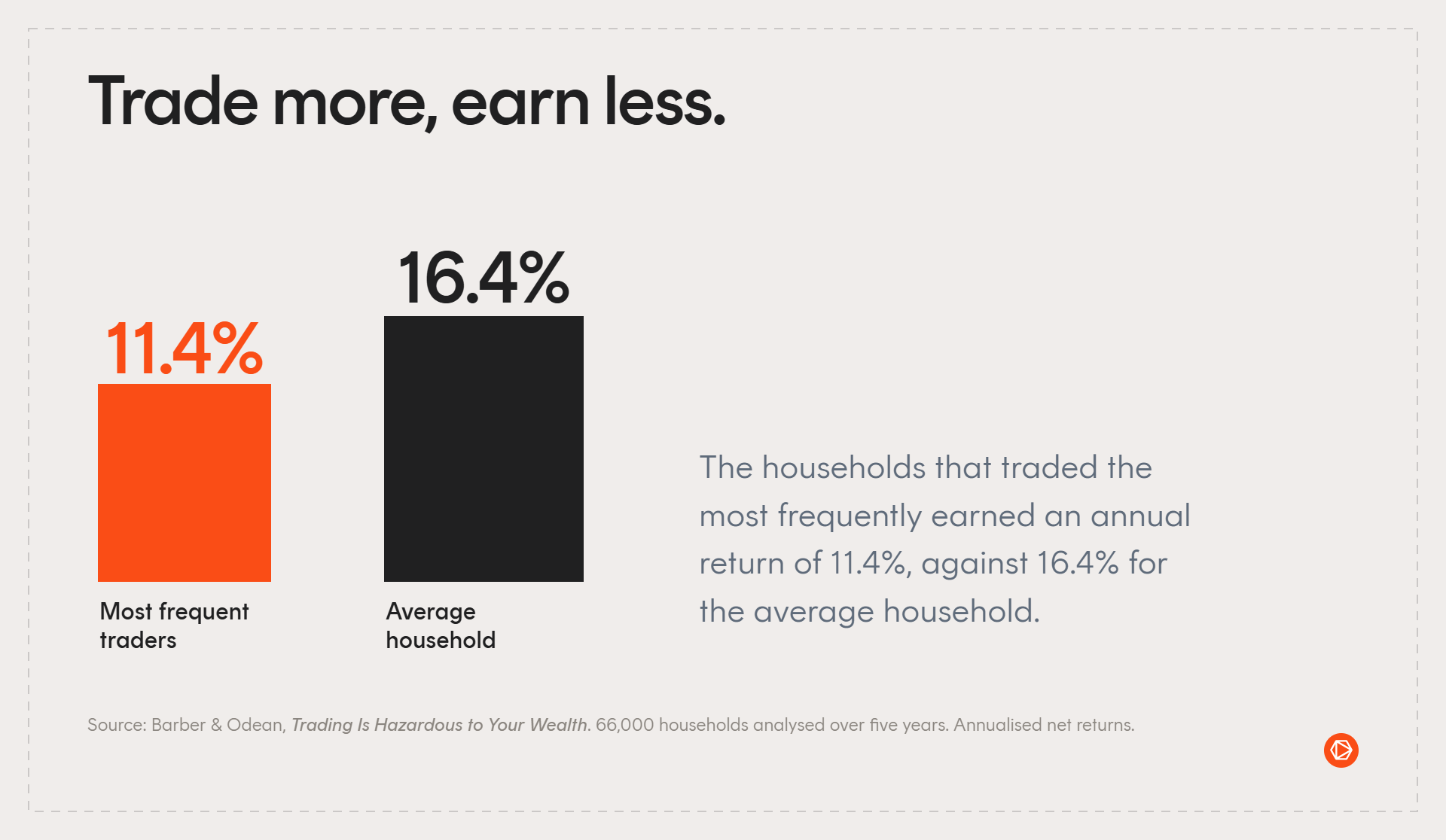

In the classic University of California study Trading Is Hazardous to Your Wealth, over 66,000 households were analysed over five years. Households that traded the most frequently earned an annual return of 11.4%, compared to the average household that earned 16.4%.

Morningstar in its 2025 Mind the Gap study even identified a ‘behaviour gap’, finding investors lost 1.2% a year due to emotional investing and behavioural impulses. These impulses show up as panic selling, buying into hype and other loss-making decisions.

Tinkering is effectively subject to the law of diminishing returns — every additional hour you spend investing produces less returns than the last hour, until eventually more time in fact earns less money.

So, figure out an investing schedule, automate it where possible and stay out of your own way.

Getting too fancy

Another problem with our perfect investor is they have a view on everything. They’ve picked up on every hot new theme and stock tip:

“Micron is up 40% this month.”

“Everyone online is buying the same stock.”

“This trading bot can beat the market.”

FOMO is a powerful force, and before long our perfect investor has a patchwork portfolio of bygone ideas. Diversification is good, but sporadically buying into trends is a flawed tactic for several reasons.

With limited money available to invest, every dollar spent chasing a trend is a dollar not spent dollar-cost averaging into a strategy. Adapting a strategy and consistently adding to a new position is one thing, but one-off hype-driven purchases can be more speculative than strategic. Adding new positions also adds the potential for overlap. An investor may end up heavily concentrated in one company or industry without realising it.

For most retail investors, complexity is a disadvantage. When in doubt, keep it simple enough to explain in a few sentences.

“Often, the best thing smart investors can do is stay out of their own way.”

Forgetting where the money really comes from

Our perfect investor may be able to tell you their portfolio’s returns down to the percentage point, but how many unused subscriptions do they have? How about long-lost gym memberships? Have they shopped around for better deals on their insurance? Are they consistently qualifying for the bonus interest from their savings account?

One of the most important parts of investing has nothing to do with investing.

As Morgan Housel puts it, saving is the gap between your ego and your income. Your savings rate is one of the most powerful wealth-building tools, yet many investors will spend far more time hunting for a couple extra percentage points in returns than they will hunting for savings in their daily life.

Making small improvements to your savings rate over time can have a major impact on your wealth thanks to compounding. Assuming a return of 9% a year, $1 today would be worth around $6 in 20 years.

A $10 subscription you don’t use may not feel like much. Buying a $150 shirt over a $25 shirt may not feel like much. But if that money could be invested instead, the long-term gains could be high. Human brains are built to think in the moment, not two or three decades from now.

Investing is the second half of the battle — saving money to invest must be the first. The more you can consistently put to work, the more chance your portfolio has to do what it is designed to do.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Future outcomes are inherently uncertain. Actual outcomes may differ materially from those contemplated in any opinions, estimates or other forward-looking statements given in this article.