David Bassanese

5 minutes reading time

Note: The Bassanese Bites Podcast will return on 2 February 2026.

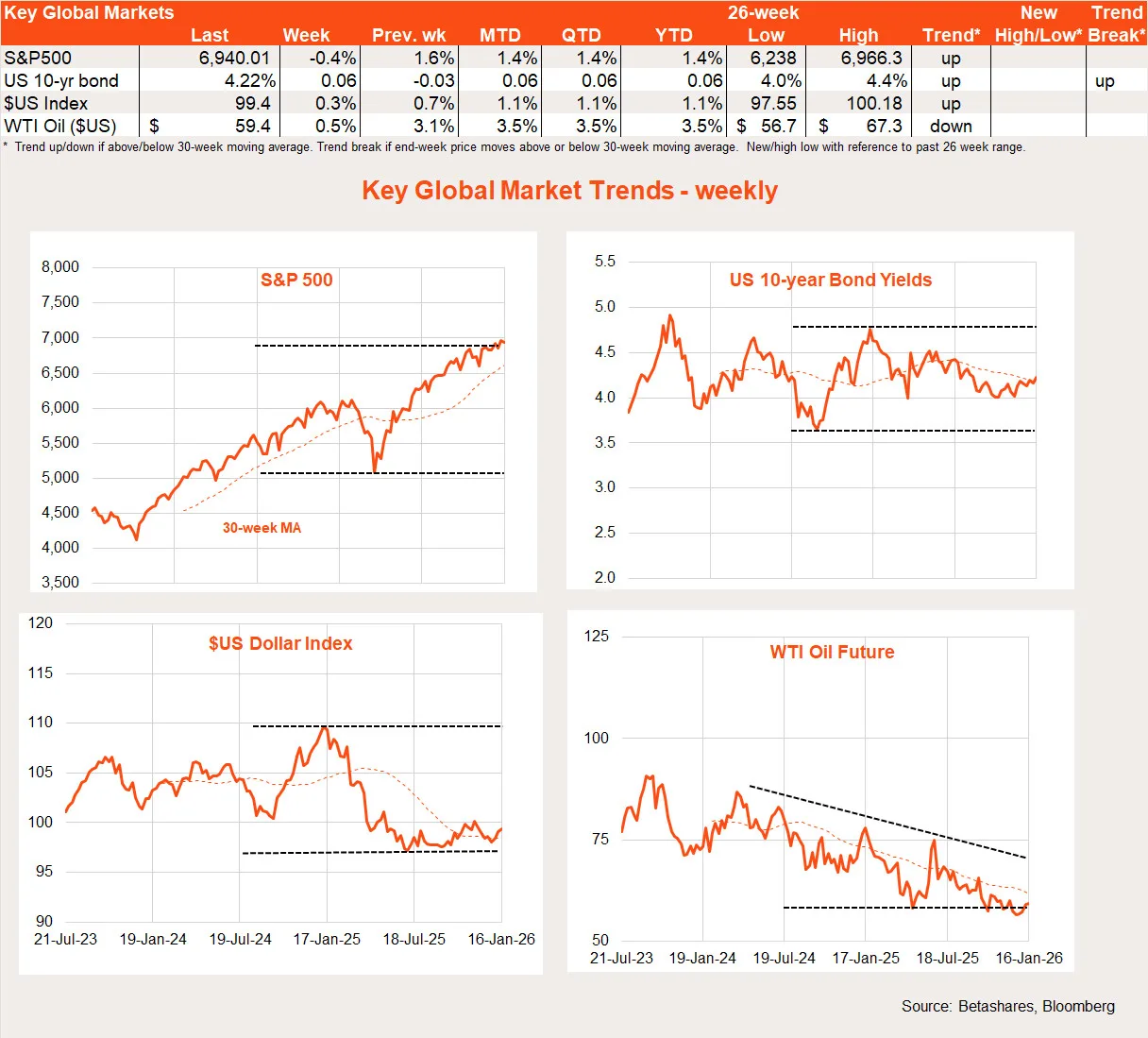

Global stocks edged lower last week, weighed down by geopolitical concerns despite still-encouraging US economic data.

Global week in review: Trump’s scatter gun

One year into his term, US President Donald Trump has started the year in fine form, with action in Venezuela, threats on Iran and Greenland and a criminal probe into the Federal Reserve.

Trump has also once again threatened tariffs on any country trading with Iran or any European country that says they are against America’s desire to buy Greenland. So much for last year’s carefully crafted trade deals!

Sadly, Trump still seems intent on throwing around tariff threats on the slightest whim. Markets are watching and waiting to see if the US Supreme Court allows him to keep wielding his tariff weapon with abandon. More broadly, markets appear to be learning to live with his various threats – taking each with a grain of salt and potentially just seeing them as ambit claims at the state of negotiations.

Either way, I suspect Trump’s threats toward Europe with respect to Greenland could ultimately backfire. For starters, it seems highly unlikely any self-respecting European country would give up on Greenland in the face of tariff threats alone. What’s more, further tariffs on major trading partners would only add to the risks facing the US economy – especially if Europe finally responds with trade retaliation of its own.

If Trump is ultimately forced to back down without acquiring Greenland, it could once again expose many of his threats as hollow, undermining all future negotiations.

Understandably, financial markets have started the year on a cautious footing, with the S&P 500 down 0.4% last week but up 1.4% year to date.

Meanwhile, US economic data has remained encouraging, with a softer than expected 0.2% gain in core US consumer prices in December. Annual core US CPI inflation edged down to 2.6% from 2.7%. November retail sales were also a touch firmer than expected, while weekly jobless claims stayed low. According to the Atlanta Fed’s GDPNow estimate, the US economy is on track to record blistering 5.3% annualised growth in Q4.

One potential warning shot, however, came from the Fed’s Beige Book report on the economy. It suggested more businesses were starting to pass on tariff increases into prices.

Outside of the US, the key news was that newly installed Japanese Prime Minister Sanae Takaichi announced early elections in a bid to capitalise on her ‘honeymoon’ popularity and potentially restore the Liberal Democratic Party’s (LDP) parliamentary majority. All this is continuing to fuel optimism of further pro-growth Japanese fiscal and monetary policy.

Global week ahead: US core PCED inflation

Following on from last week’s benign CPI report, a highlight this week will be the Fed’s preferred inflation measure – the private consumption expenditure deflator (PCED). Core prices are also expected to rise only 0.2%, which would see annual core PCED inflation ease to 2.7% from 2.8%. Markets still expect the Fed to leave rates on hold at the 28 January meeting.

Otherwise, focus will remain on the various geopolitical tensions simmering around the world – from Ukraine to Venezuela to Iran and Greenland.

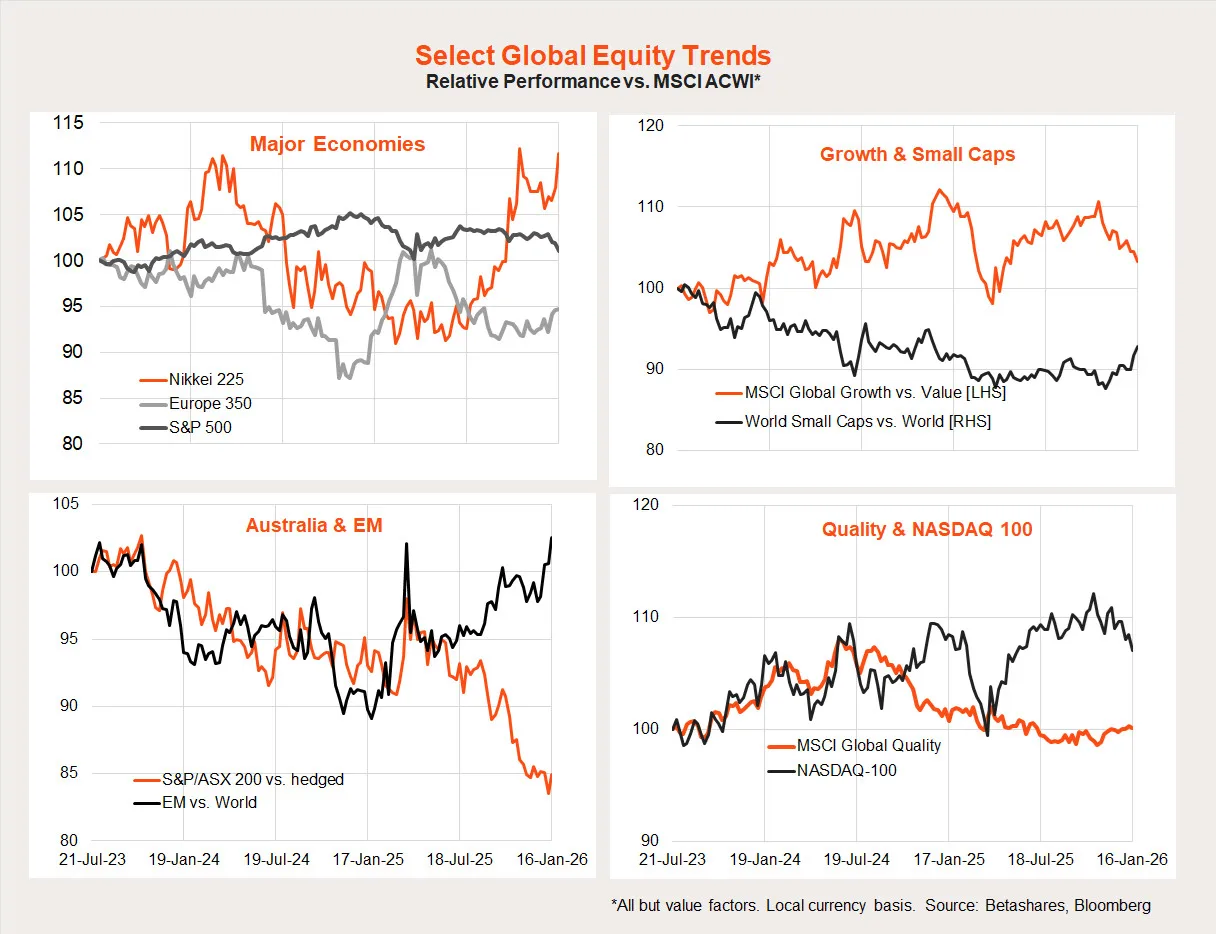

Global equity trends

Is the ‘great rotation’ finally underway? A notable recent trend has been the underperformance of growth/technology since end-October, replaced by strength in Japan, emerging markets and small caps. Sadly, Australia’s trend underperformance continues despite renewed optimism in the resources sector.

Australian week in review: Hawkish hold

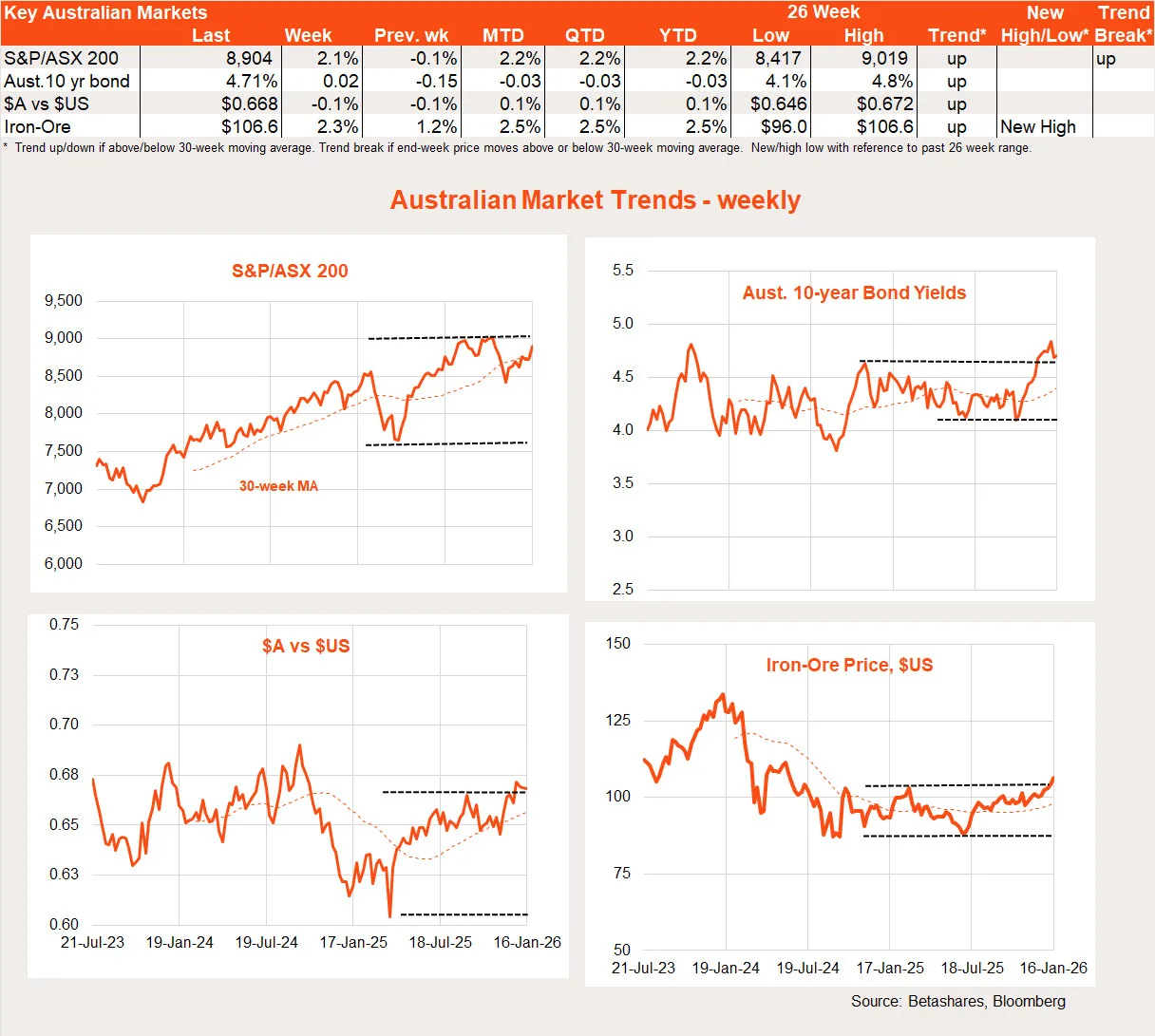

Australian shares enjoyed a healthy bounce last week, supported by a solid 3.9% gain in the materials sector. That said, even financials were up 1.9%.

The gain in stocks came despite mixed local economic news. Although the new household spending indicator revealed solid 1% growth in November, the Westpac measure of consumer confidence dropped back 1.7% in January.

A week earlier, the November monthly CPI still suggested underlying price pressures were firm, with the trimmed mean measure up another 0.3% in the month – though annual trimmed mean inflation eased to 3.2% from 3.3%. The focus remains on next week’s all-important Q4 CPI report, which will make or break the RBA’s interest rate decision at the February policy meeting.

My base case is the Q4 trimmed mean gain will be 0.8% or less, and that should be enough for the RBA to hold the line on rates. That said, I also concede the RBA could hike with a 0.8% gain or that the gain could be more than 0.8%.

Australian week ahead: December employment

The case for rate hikes would also weaken if the labour market turned down more clearly. Employment fell 21k in November, although the unemployment rate held steady at 4.3%.

Against this backdrop, Thursday’s December employment report will be important. With most employment indicators suggesting only a gradual weakening in labour demand, the market expects a decent bounce back in employment in December of around 25k. That said, consistent with gradual labour market softening, the unemployment rate is expected to edge up to 4.4% from 4.3%.

All up, results such as these mean the labour market should not be a barrier to a February rate hike from the RBA if next week’s Q4 CPI is on the high side.

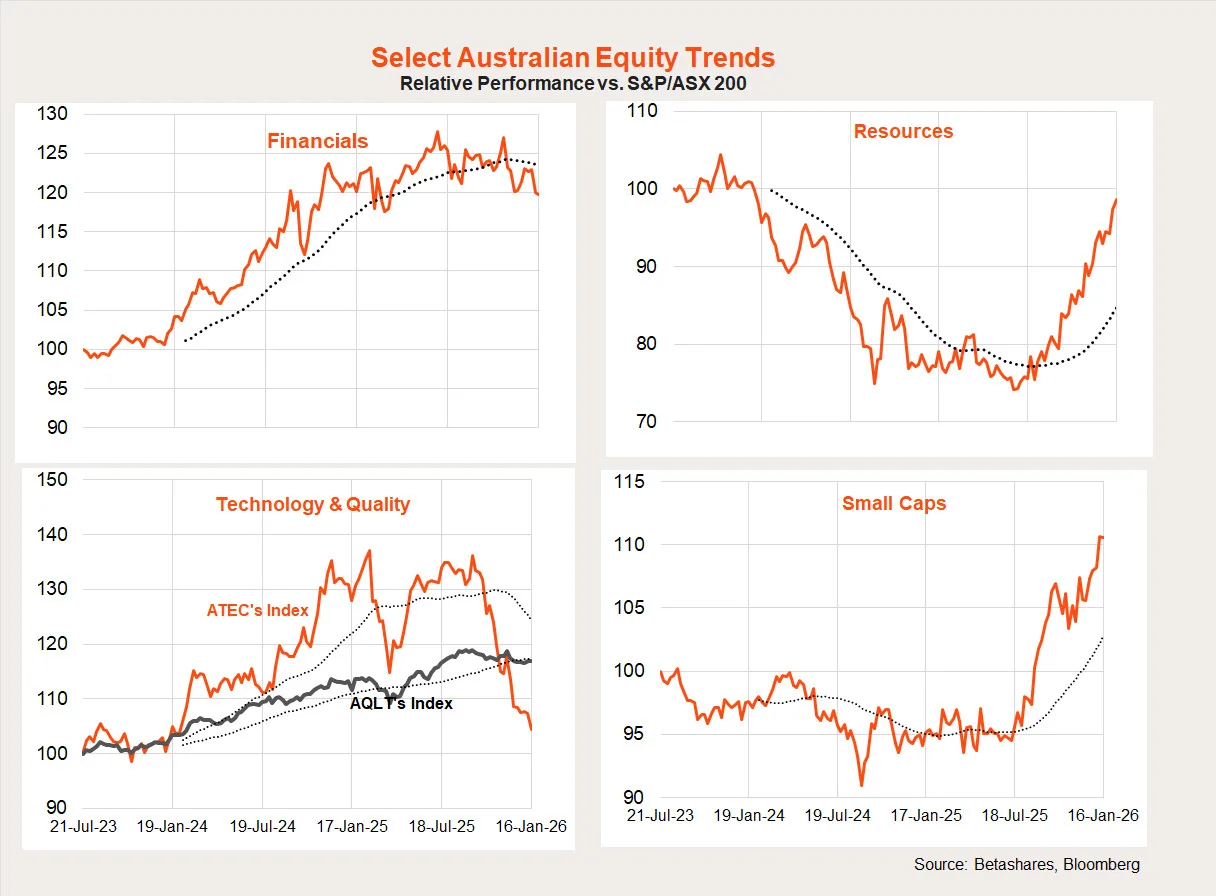

Australian equity trends

A rotation from financials/technology to resources and small caps has been clearly evident in the Australian market over recent months. Upgrades to resource sector earnings and general optimism around commodity prices appears to be supported by large and small cap resource companies.

Have a great week!

1 comment on this

Keep the good work going. I look forward to reading it every week.