Tom Wickenden

6 minutes reading time

- Technology

After a strong recovery from a 2022 drawdown the Australian technology sector once again finds itself in a bear market.

Similarly to 2022 central bank policy has played a part in this sell off, along with major acquisitions impacting short term earnings and a broader global software meltdown.

We discuss each of these factors in analysing whether the dynamic and high growth Australian technology sector can rebound once again.

Is the worst already priced in

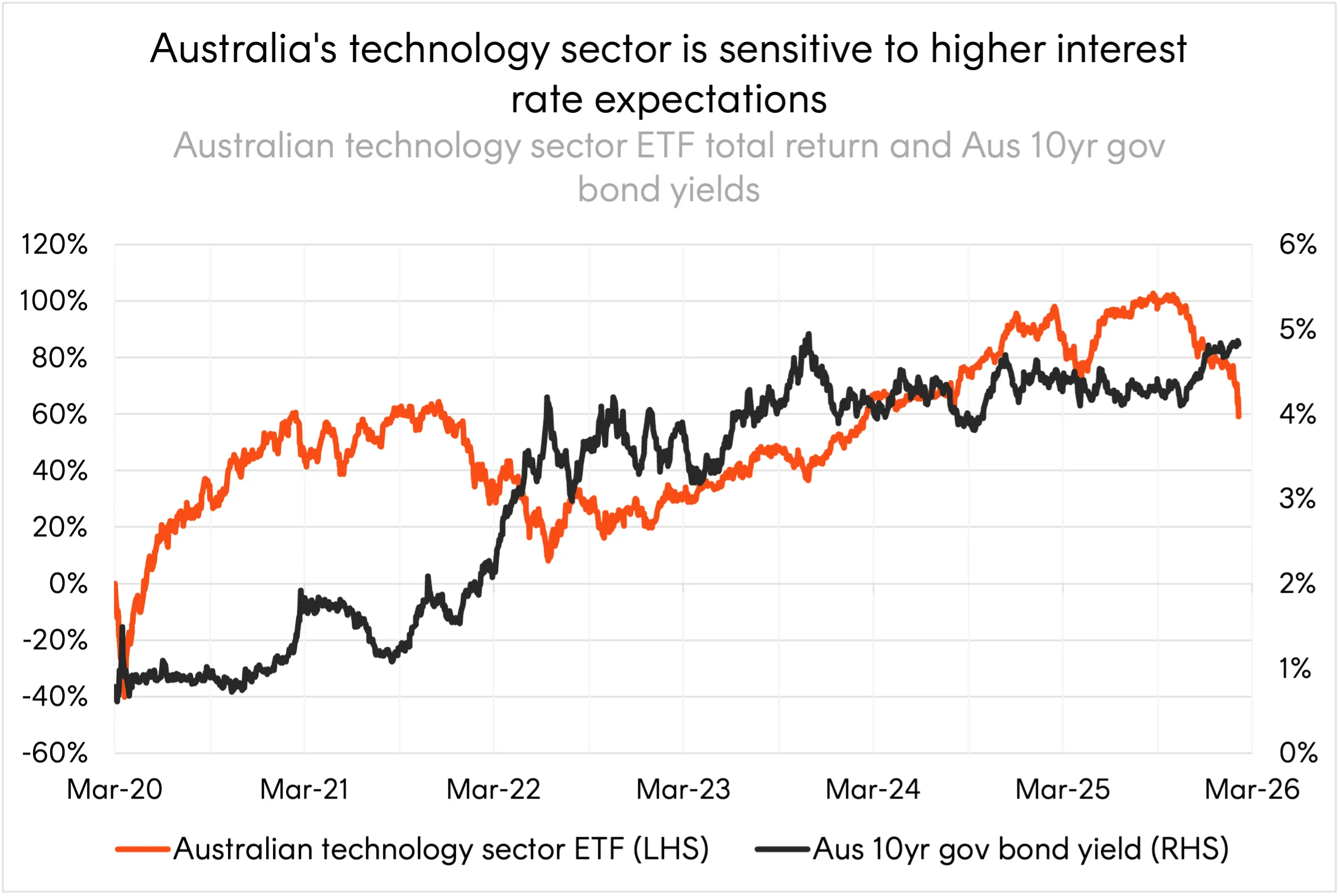

The Australian technology sector is no stranger to interest rate driven sell offs. During 2022 the realisation that rates would need to be raised significantly in Australia saw the local technology sector drawdown 44.6%1.

Attracting high valuations due to typically strong earnings growth expectations and future upside potential the Australian technology sector is sensitive to interest rates impacting funding, sentiment, and valuation calculations.

Source: Bloomberg. 5 March 2020 to 6 February 2026. Past performance is not indicative of future performance. Australian technology sector ETF represented by Betashares S&P/ASX Technology ETF (ASX: ATEC). ATEC’s inception date is 4 March 2020.

Since the fourth quarter of 2025 as investors began pricing in RBA rate hikes for 2026, the first of which came to fruition in February, the Australian technology sector has sold off over 30%2.

We believe the market has gotten ahead of itself in assuming a much higher long-term neutral rate in Australia relative to the US – as discussed further here. As such we expect the RBA will be able to cut rates to a more neutral level in the coming years which could once again be supportive of Australian technology returns.

While rate expectations have likely played a part, the severity of the current drawdown points to compounding factors for the current sell off.

Short term pain long term gain

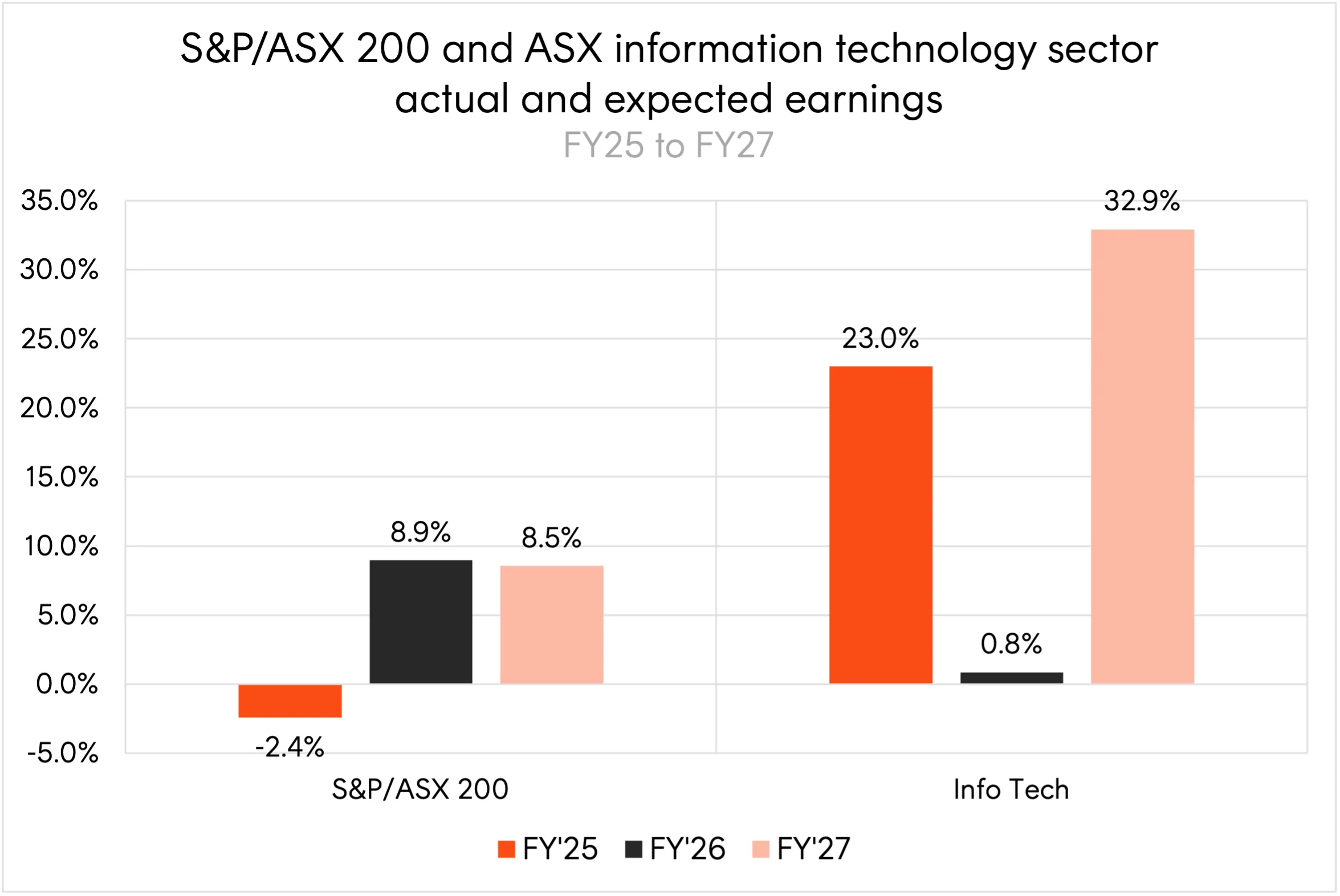

Just 5 months ago we wrote an insight promoting the high expected earnings growth for the Australian technology sector. Since then, the sector’s earnings expectations have collapsed from over 20% to near-zero for FY263, driven by downgrades to Xero and WiseTech Global, which together command high weights in the ASX Information Technology Index.

Source: Refinitiv. As at 13 January 2026. FY’26 and FY’27 include analyst forecasts. Actual results may differ materially from forecasts.

Xero’s US$2.5 billion acquisition of loss-making Melio is expected to materially reduce FY26 EBITDA as Melio is currently a loss-making business. Transaction and integration costs plus ongoing losses have prompted analyst earnings downgrades4. Shares have fallen 56% over twelve months5.

WiseTech’s US$2.1 billion e2open acquisition dilutes EBITDA margins due to e2open’s lower profitability profile and integration expenses. Analysts reduced revenue forecasts for FY26-28 in response to the margin compression. Compounding these operational challenges, governance concerns erupted after ASIC/AFP raids over alleged insider trading, prompting director resignations and AustralianSuper’s exit. Shares have fallen 60% from the 2025 peak6.

While these downgrades have compressed FY26 sector earnings, both companies are investing for future growth rather than experiencing fundamental deterioration. The market appears to recognise this transition period, with FY27 sector earnings expectations rebounding to over 30%7 as acquisition synergies and integration benefits are anticipated to materialise.

Software becomes first big victim of AI speculation

Software companies comprise a significant portion of the Australian technology sector, making them particularly vulnerable to current AI disruption fears that have gripped markets.

The narrative suggests that generative AI will allow new entrants to replicate complex software functionality at dramatically lower costs, eroding the competitive moats of established players.

However, in our opinion this sell-off appears overdone. While AI undoubtedly presents competitive challenges, it’s more likely to enhance rather than replace leading SaaS platforms. The value proposition of companies like Xero and WiseTech extends far beyond the software itself, it encompasses data integrity, regulatory compliance, ecosystem integrations, and continuous support. Small to medium-sized businesses, which form the core customer base for most Australian tech companies, have neither the resources nor desire to build and maintain their own software solutions. They’re seeking to outsource complexity, not manage bugs, updates, and system integrations internally. Low-cost competitors are nothing new in the SaaS space and historical evidence points to a cycle of companies switching on price competitiveness only to return to the dominant market players following integration and ongoing support frustrations.

We believe AI represents an opportunity for established platforms with sticky customer relationships and embedded workflows to deepen their value proposition rather than an existential threat.

Looking ahead

The current drawdown in Australian technology is not without reason. Higher expected interest rates, earnings downgrades, and a global software meltdown have all contributed.

However, the case for the sector to once again rebound is strong. Long term investors may see the current drawdown as an opportune time to enter with compressed valuations amid a potentially overdone sell off.

As with any high-growth sector, investors should expect significant volatility and be comfortable with substantial drawdowns like the current one.

For investment exposure, ATEC S&P/ASX Australian Technology ETF offers investors access to the S&P/ASX All Technology Index (before fees and expenses)8. The Index provides exposure to leading ASX-listed companies in a range of tech-related market segments such as information technology, consumer electronics, online retail and medical technology.

For more information on ATEC’s current holdings and historical performance visit the fund page here.

There are risks associated with an investment in ATEC, including market risk, technology sector risk and concentration risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

Sources:

1. Returns of S&P/ASX All Technology Index from 19 November 2021 to 17 June 2022. Past performance is not an indicator of future performance. You cannot invest directly in an index. ↑

2. Source: Bloomberg. As at 6 February 2026. ↑

3. Source: As at 6 February 2026. Refinitiv consensus estimates. Actual results may differ materially from estimates. ↑

4. Source: Bloomberg analyst estimates. Actual results may differ materially from estimates. ↑

5. Source: Bloomberg. As at 6 February 2026. ↑

6. Source: Bloomberg. As at 6 February 2026. ↑

7. Source: As at 6 February 2026. Refinitiv consensus estimates. Actual results may differ materially from estimates. ↑

8. You cannot invest directly in an index. ↑