After a hawkish six months driven by the Iran oil shock and the 5 May hike, the macro setup has shifted. April unemployment printed at 4.5%, above consensus of 4.3% and the RBA’s forecast trajectory, with employment falling 18,600 in the first monthly decline in five months. Bond yields have drifted lower since, and the June meeting now prices little chance of a follow-up hike.

This is not 2022. Then, the cash rate sat at 0.10%, real 10-year yields were minus 0.60%, and demand was overheating on reopening stimulus. Today the inverse holds: consumption is anaemic, the labour market is showing signs of cracking, the cash rate at 4.35% is already restrictive, and real 10-year yields at 2.5% sit at 15-year highs. Governor Bullock made the point explicit at the 5 May meeting, with the post-meeting statement and press conference guiding towards a pause. Unemployment is now at the RBA’s own NAIRU estimate of 4.5%, bringing the dual mandate back into focus, meaning that a cycle peak in yields, and possibly in the cash rate itself, is behind us.

For investors with cash to deploy, locking in today’s corporate bond yields before the next easing cycle is priced in presents a compelling opportunity. The newly launched 31BB 2031 Fixed Term Corporate Bond Active ETF allows just that.

Australia’s first Defined Income ETF range expands with 31BB

31BB extends Australia’s first Defined Income ETF range, which Betashares launched in May 2025 with 28BB, 29BB and 30BB. The four funds form a ladder of investment-grade Australian corporate bond ETFs maturing each May from 2028 through 2031, with current net-of-fee yields ranging from 5.13% to 5.37% p.a1. That sits well above comparable major-bank term deposit rates at the 4 and 5-year tenors (see the comparison table below).

The Defined Income ETF range was the first of its kind in Australia. The range is designed to fill a gap between traditional bond ETFs, which do not replicate the certainty of holding an individual bond to maturity, and alternatives such as term deposits and fixed-term annuities, which can come with limitations including illiquidity and lack of transparency. The format is well-established in the US, where it is widely used as an alternative to bank deposits for investors seeking predictable incomes and return outcomes without locking up capital.

The suite has also picked up external recognition. Betashares Capital is a finalist in the Innovation Award category of the 2026 Lonsec Fund Manager of the Year Awards for the Fixed Term Corporate Bond Active ETFs (finalists announced 4 May 2026)2.

How they work

Each fund aims to replicate the cash-flow profile of holding an individual bond to maturity, spread across a diversified portfolio of investment-grade Australian corporate bonds, in a single ASX trade. The funds currently hold between 36 and 49 bonds. Each fund has a fixed maturity in May of its designated year. At inception a target monthly distribution is set off the prevailing portfolio yield net of fees and costs, in much the same way a bond’s coupon is fixed at issuance. Distributions are paid monthly through the life of the fund. At maturity, unit-holders receive the NAV, just as a bond repays its face value or a term deposit returns capital.

Unlike a term deposit, which locks up capital and typically charges early-withdrawal penalties, units trade on ASX during market hours with T+2 settlement. Flexibility matters in a cycle where the next move in yields is genuinely two-sided.

Portfolio characteristics: Yield, duration, and credit quality

Defined Income suite snapshot

| 28BB | 29BB | 30BB | 31BB | |

|---|---|---|---|---|

| Yield to maturity (net of fees, % p.a.) | 5.13% | 5.13% | 5.27% | 5.37% |

| Fund maturity | May 2028 | May 2029 | May 2030 | May 2031 |

| Target monthly distribution ($/unit) | $0.08440 | $0.08570 | $0.09040 | $0.11179 |

| Modified duration (yrs) | 1.43 | 2.26 | 3.11 | 3.88 |

| Average credit quality | A | A+ | A | A- |

| Management fee (p.a.) | 0.22% | 0.22% | 0.22% | 0.22% |

Source: Betashares. 28BB/29BB/30BB as at 22 May 2026; 31BB as at 25 May 2026. Each Defined Income Bond ETF’s Yield to Maturity (YTM) is the weighted average of the Fund’s underlying holdings of fixed rate bonds. A bond’s YTM is the annualized total expected return of the bond if it is held to maturity, does not default, and coupons are reinvested. YTM is shown net of the Fund’s management fee. The target distribution may vary in certain circumstances. Please refer to the PDS. Credit ratings are opinions only and are not to be used as a basis for assessing investment merit. Ratings and yields are subject to change over time.

Comparable rates across major bank term deposits and the Defined Income suite (as at 25 May 2026)

| Issuer and product | 2yr | 3yr | 4yr | 5yr |

|---|---|---|---|---|

| CBA TD | 5.25% | 4.60% | 4.00% | 4.00% |

| Westpac TD | 5.00% | 4.60% | 4.00% | 4.00% |

| NAB TD | 5.20% | 3.80% | 3.80% | 3.80% |

| ANZ TD | 5.00% | 4.60% | 4.00% | 4.00% |

| Macquarie Bank TD | 3.60% | 3.65% | 3.80% | 3.80% |

| Betashares Defined Income ETFs (YTM, net of fees) | 5.13% (28BB) | 5.13% (29BB) | 5.27% (30BB) | 5.37% (31BB) |

Sources: Issuer websites; Betashares (fund yields, 22 to 25 May 2026). Bank rates are headline annual-interest-payment at the highest tier publicly advertised. Defined Income ETF yields are net of fees and assume the fund is held to its stated maturity.

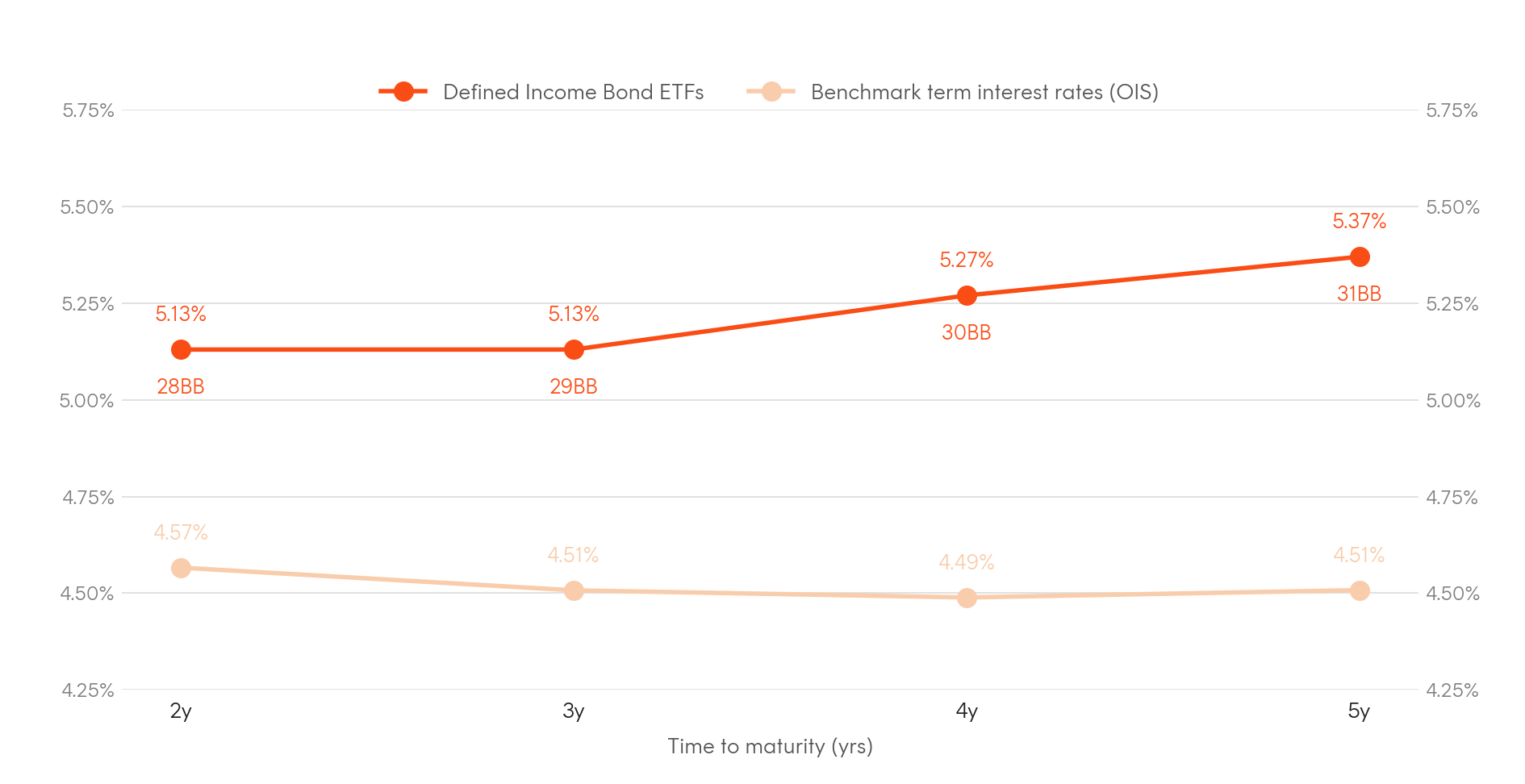

The table above compares the ETF yields against individual bank rates. The chart below broadens this comparison to include benchmark term interest rates, further illustrating the yield advantage on offer across all maturities. It should be noted that the Defined Income ETFs are not capital guaranteed and do not benefit from any government guarantee that applies to term deposits and are subject to risks, including market risk, interest rate risk and credit risk.

Source: Bloomberg, Betashares; yields shown net of fees; 28BB = 2y, 29BB = 3y, 30BB = 4y, 31BB = 5y, benchmark term interest rates shown reflected by AUD overnight indexed swap rates (OIS) over the relevant tenors; data as at 25 May 2026

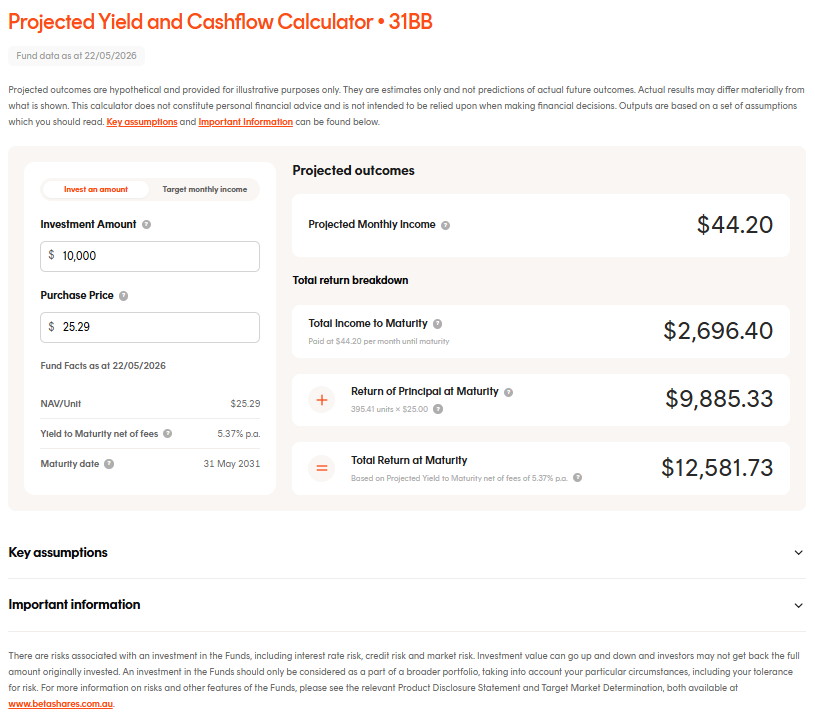

Modelling the cash flows

Each fund page hosts an interactive cashflow calculator. Enter an investment amount and the current portfolio YTM and it returns the projected monthly distribution, the total income paid through the fund’s life, and the terminal value at maturity. The output sequences the projected cashflows month by month, so advisers can show a client exactly what holding to maturity looks like in dollar terms.

This is genuinely novel infrastructure for an Australian fixed income ETF. It bridges the gap between the abstract YTM figure on a factsheet and the practical question an end client typically asks: how much do I receive each month, and what do I get back at the end? For advisers building income strategies into a financial plan, the calculator provides a convenient, mechanical basis for the income assumption rather than relying on a single yield number.

Visit the 31BB 2031 Fixed Term Corporate Bond Active ETF fund page.