Cameron Gleeson

12 minutes reading time

Our 2026 investment outlook discusses why investors need to be paying attention to geopolitics again, given the escalating competition between the US and China. We now live in a world where trade and capital flows are increasingly being determined by governments’ strategy priorities, rather than market forces.

Below we highlight some investment opportunities that flow from a shift in government policies and increasing fiscal support for critical minerals, defence spending and AI hardware supply chains. We also make that case that gold’s rally may continue given the structural drivers remain intact, and discuss why the oil price might be set to rally despite a surplus of supply.

We expect USD weakness to drive Gold higher in 2026

Gold was the stand-out performer in 2025, returning 67.4% in US dollar (USD) terms. It continued to rally this year, reaching US$5,586 an ounce on 29 January, before Trump’s announcement of Kevin Warsh as the next Fed governor saw it tumble to as low as US$4,406 in a matter of days. Many investors are asking whether they have missed the boat. We continue to believe gold is a worthy addition to traditional multi-asset portfolios. However, the currency in which investors get their exposure to gold matters, particularly as the USD faces continued headwinds from likely Fed rate cuts, a ballooning US fiscal deficit and central banks switching their reserves from US Treasuries to gold.

In early February 2026, China warned its banks to rein in their holdings of US Treasuries, and the USD fell and gold rallied above US$5,000 again.

Gold has traditionally been viewed as a ‘safe haven’ against geopolitical shocks, but its primary driver since Trump’s inauguration has been the trajectory of the USD, as is clearly seen in the chart below.

Source: Bloomberg, 20 January 2025 to 10 February 2026. Past performance is not an indicator of future performance.

Our view is the USD will continue to weaken in USD for the reasons above, as discussed in more detail here. In this context, we believe investors should seek exposure to the USD gold price, as opposed to the AUD gold price.

-

QAU

Gold Bullion Currency Hedged ETF

- QAU provides investors with a return that tracks the performance of the price of gold bullion, while hedging against currency movements in the AUD/USD exchange rate, before fees and expenses.

- QAU is the largest currency hedged gold bullion ETF trading on the ASX, and was one of the best performing ETFs in 2025. Over the five years to 31 January 2026 QAU has returned 19.7% p.a.1

Is the world sleepwalking into another oil crisis?

At the time of writing Iran and the US have entered into talks to avoid conflict, against the backdrop of a US military build-up in the Middle East.

The first round of indirect discussions in Oman has been described as a “good beginning”, but defining the scope of negotiations and agreeing concessions will be a greater challenge. Iran wants to limit talks to just their nuclear program, however Israeli prime minister Benjamin Netanyahu is lobbying Trump to broaden negotiations to include Iran’s ballistic missiles, support for groups like Hamas and Hezbollah, and human rights abuses. Thousands of Iranians were killed in nationwide protests against their government after Trump told them, “Help is on the way”. Trump risks a loss of face. If he agrees to a more limited nuclear agreement, like the Obama Iranian nuclear deal he tore up in his first administration. Or at the other extreme, the potential for a prolonged military entanglement that would break his “no more wars” promise to the American public.

Any foreign strike on Iranian leadership would be viewed as an existential threat, provoking retaliation. Saudi and Iraqi oil production as well as Israel and the Strait of Hormuz would be the most likely targets. But even if Iranian retaliatory attacks were thwarted, regime change from a radical Islamic regime that has controlled Iran for almost half a century would be messy, and a disruption to Iran’s own oil exports inevitable. As OPEC’s fourth largest exporter, the shock to global oil markets would be immediate.

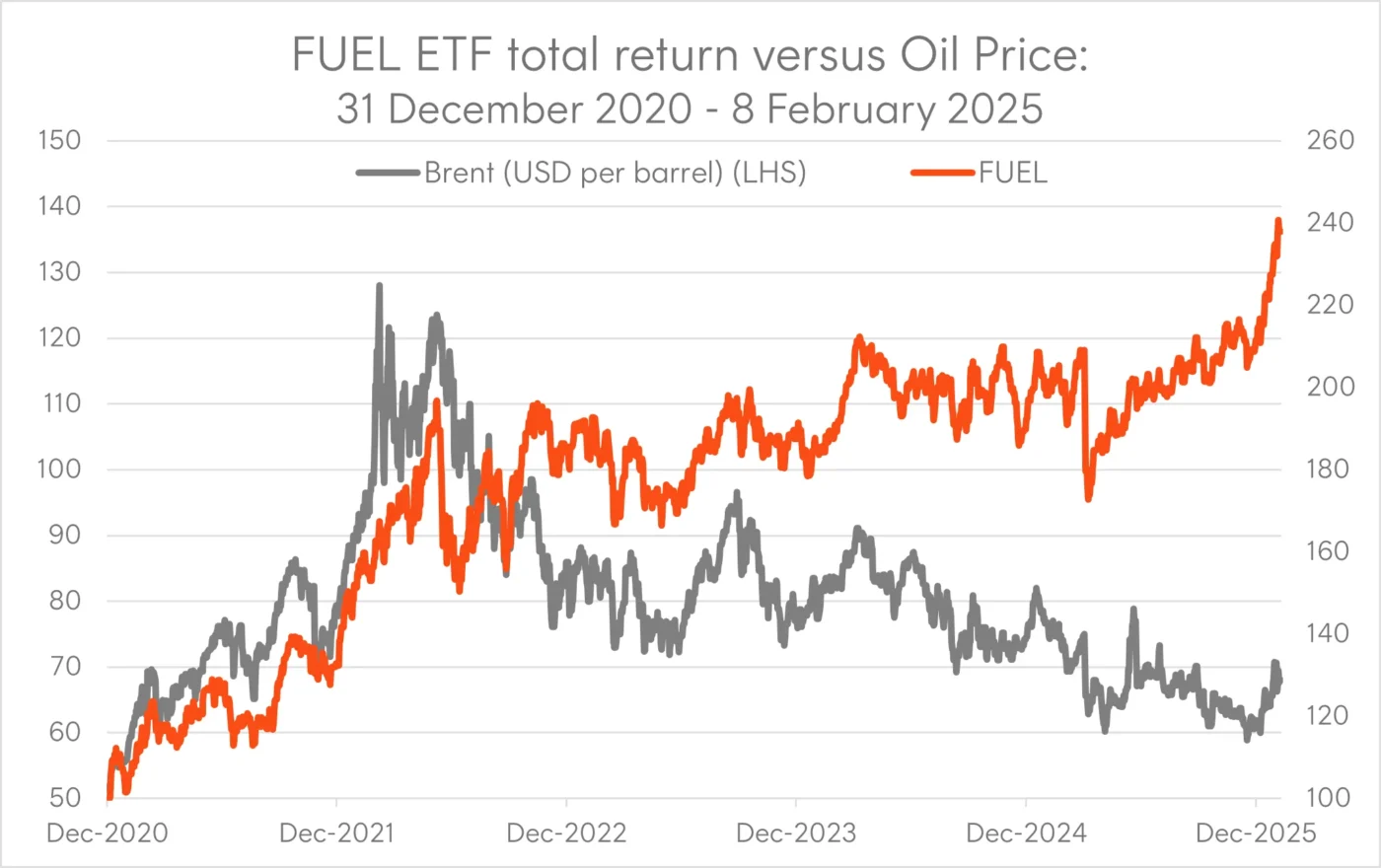

Global energy companies have underperformed the broader market over the last three years, due to excess supply keeping a lid on oil prices. However, they have broken out recently, with the risk that we see a jump in the oil price, like the one that occurred after Russia invaded Ukraine in 2022.

Source: Bloomberg, 31 December 2020 to 9 February 2026. FUEL is Betashares Global Energy Companies Currency Hedged ETF. FUEL returns are total returns rebased to a starting value of 100, assuming reinvestment of distributions and net of ongoing fees. Past performance is not an indicator of future performance.

Even without the threat of an oil crisis in the Gulf, energy company fundamentals appear to be turning a corner. Earnings growth for the sector has been weak for a number of years, but with expectations beaten down, energy has seen the largest positive revenue surprise of any sector so far in the US Q4 earnings season. Marathon Petroleum ($4.07 vs. $2.72), Valero Energy ($3.82 vs. $3.27), Baker Hughes ($0.78 vs. $0.67), and Phillips 66 ($2.47 vs. $2.15) have reported the largest positive EPS surprises, with some meaningful share price reactions on announcement.2

-

FUEL

Global Energy Companies Currency Hedged ETF

- FUEL provides access to a portfolio of the world’s largest energy companies (ex-Australia), including Chevron, ExxonMobil and Shell, in one ASX trade.3

- These global energy companies that are larger, more geographically diversified, and more vertically integrated than the Australian-listed energy companies.

Chokepoint in the AI supply chain – Asia Tech

Technology and the rise of AI have become a key driver of equity market returns for the last three years. Many mega-cap tech companies in the US are ploughing billions of dollars into AI-related infrastructure capex to build frontier models. This spending is supporting the broader semiconductor supply chain located in Asia, and includes companies such as Samsung, SK Hynix and Taiwan Semiconductor. These companies provide cutting edge logic and memory chips that are critical for the development of the leading US AI models. But as China’s AI capabilities continue to rise, we think investors should take a diversified exposure to the dynamic Asian technology theme.

For further details on this topic, please read insights piece titled, “Asian technology companies – the ultimate AI hedge?”

-

ASIA

Asia Technology Tigers ETF

- ASIA provides investors exposure to the 50 largest technology and online retail stocks in Asia (ex-Japan), including the companies mentioned above, Alibaba, Tencent and Baidu.

- As a theme, Asian technology generally trades much cheaper valuations than US technology; with Alibaba, Taiwan Semiconductor and SK Hynix priced at 1 year Forward PE ratios of 21.3x, 19.2x and 6.4x, respectively.4

A critical priority for the US administration in 2026

In the US, critical minerals have come into focus due their use in the AI data centres being built, as well as the grid, renewable energy generation and battery storage required to power those data centres. China’s own AI roll out together with a massive ramp up of EV exports (that use lithium, graphite, copper, rare earths) is also adding to global demand. In addition, certain critical minerals play a key role in defensive technology, making the US reliance on critical mineral imports a significant national security vulnerability.

In early February ministers from 54 countries, including Australia, discussed a US proposal to reduce their dependence on China for the supply of critical minerals, and ensure ongoing access to these key resources. In a seemingly rare show of multilateral cooperation the EU, Japan, Mexico and the US have agreed to create price support mechanisms and provide capital backing for critical mineral projects. And this comes after the establishment of critical mineral reserves by countries like the US and Australia.

Selected producers of these minerals from allied countries, like Australia, Canada, Peru and Chile, are likely to be key beneficiaries of this government support.

-

XMET

Energy Transition Metals ETF

- Within XMET’s portfolio includes 30 of the leading global producers of critical minerals, including copper, lithium, nickel, cobalt, graphite, manganese, silver and rare earth elements. This includes companies such as Southern Copper, Pilbara Minerals and MP Materials.5

- After going sideways for three years, XMET returned 96.27% over the 2025 calender year as critical mineral prices recovered, and has carried that momentum into early 2026. XMET has returned 24.14% p.a. since its inception in October 2022.6

Source: Bloomberg, 30 December 2022 to 31 January 2026. XMET is Betashares Energy Transition Metals ETF. XMET figures are total returns, assuming reinvestment of distributions and net of ongoing fees.. Past performance is not an indicator of future performance.

The US returns to nuclear, fuelling uranium demand

Momentum is also gathering for uranium, after it was added the US government list of critical minerals in late 2025 and the Secretary of Energy signalled the potential for a strategic reserve. Uranium miners received an additional boost when the US government provided US$900 million in funding to US uranium enrichment companies to kick start domestic enrichment capacity for their nuclear industry.

However, much of the future demand growth for uranium will come from emerging market countries. China is leading the world in new nuclear power plant construction, with dozens more reactors under construction, and India’s parliament has just passed a bill to end a strict state monopoly for nuclear in favour of a mixed, public-private model to accelerate capacity.

-

URNM

Global Uranium ETF

- URNM provides Australian investors access to access leading companies in the global uranium industry, including Australian-listed uranium miners and offshore companies like Cameco, Kazatomprom and Nextgen Energy.7

- URNM has returned [27.49%] p.a. since inception on 8 June 2022.8

Countries boost defence spending for a less certain world

Following a stellar year of performance in 2025 investors have been asking whether the rally in global defence companies can persist. It is worth remembering that Trump’s new world order, associated geopolitical tensions, and as a result, increased defence budgets tied to GDP are structural tailwinds.

Source: Stockholm International Peace Research Institute, April 2025.

Japan is on track to double its defence budget to 2% of GDP by 2027, and NATO committed to increasing defence spending to 5% of GDP by 2035. Already in 2026 Trump has demanded Congress increase defence spending by more than 50% to US$1.5 trillion for 2027. These factors make the defence sector investible for the foreseeable future.

-

ARMR

Global Defence ETF

- ARMR’s index currently includes the top 20 pure-play defence contractors in the world by defence revenue, headquartered in NATO-member and major NATO ally countries, including Lockheed Martin, BAE Systems, Rheinmetall, RTX, and Thales.9

- These companies are set to be some of the largest beneficiaries of governments implementing increased defence spending commitments.

Where geopolitics meets digital security

Cybersecurity remains an enduring investment thematic as the rise of AI and geopolitical fragmentation continues to expand the attack surface area across industries. More recently however, leading platforms such as CrowdStrike and Palo Alto have been caught up in a broader software led tech sell off that has prompted some cause for concern.

Despite these developments, cybersecurity should remain a resilient sector given security spending remains incredibly defensive in nature. Chief Information Officers (CIOs) surveyed by Morgan Stanley view security software as an area within IT budgets that will see spend increases in 2026.10 And while the rise of new AI agents is undermining the moats and margins of traditional SaaS vendors, these developments may likely accelerate the frequency and sophistication of cybersecurity attacks given the autonomous nature of these capabilities. This presents another tailwind for the cybersecurity industry with leading platforms within the space still forecast to deliver strong underlying earnings growth.

Alongside these drivers, capital market activity has also been supportive for continued deal flow into the sector.

-

HACK

Global Cybersecurity ETF

- HACK provides investors exposure to around 30 leading companies in the global cybersecurity sector, including CrowdStrike and Palo Alto but also Cisco and Broadcom which have both become major cybersecurity players through their acquisitions of Splunk, Symantec and VMware respectively.11

- HACK’s portfolio trades with a 1 year Forward PE ratio of 19.6x, with consensus earnings growth of 17.9% p.a.12

There are risks associated with an investment in the Funds, including market risk, sector risk, concentration and cybersecurity companies risk (for HACK), gold price risk (for QAU), emerging markets risk (for ASIA) and energy transitional metals risk (for XMET). Investment value can go up and down. An investment in the Funds should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please see the relevant Product Disclosure Statement and Target Market Determination, both available on this website.

Sources:

1. As at 31 January 2026. Past performance is not an indicator of future performance.

2. Source: Factset, Earnings Insight, 6 February 2026

3. No assurance is given that these companies will remain in the portfolio or be profitable investments.

4. Source: Bloomberg consensus earnings, as at 13 February 2026. Actual results may differ materially from estimates.

5. As at 31 January 2026, no assurance is given that these companies will remain in the portfolio or be profitable investments.

6. As at 31 January 2026. Past performance is not an indicator of future performance.

7. No assurance is given that these companies will remain in the portfolio or be profitable investments.

8. As at 31 December 2025. Past performance is not an indicator of future performance.

9. Source: Data for the Top 100 list comes from information Defense News solicited from companies, from companies’ earnings reports, from analysts, and from research by Defense News, the International Institute for Strategic Studies and SPADE Indexes. No assurance is given that these companies will remain in the portfolio or be profitable investments. ARMR provides exposure to up to 60 leading companies which derive more than 50% of their revenues from the development and manufacturing of military and defence equipment, as well as defence technology.

10. Source: Morgan Stanley Q4’25 CIO Survey. Published January 15, 2026

11. No assurance is given that these companies will remain in the portfolio or be profitable investments.

12. Source: Bloomberg consensus earnings, as at 13 February 2026. Actual results may differ materially from estimates.