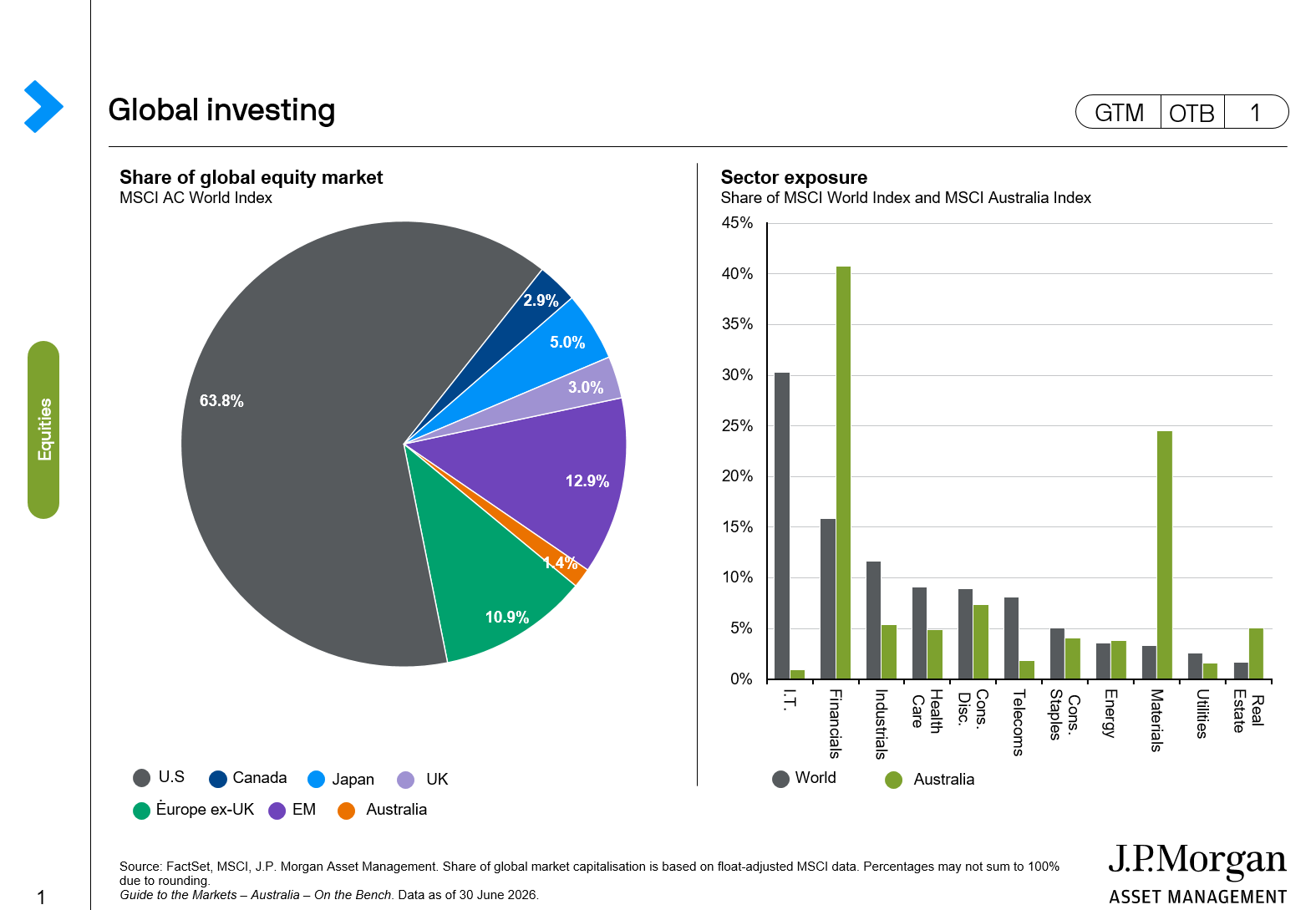

Australia represents just 1.4% of the global share market, yet many local investors allocate a large share of their portfolios to ASX-listed companies. That tendency is known as home bias and, while it’s understandable, it can also be limiting.

Investing close to home can feel reassuring: familiar brands, known businesses and local news you can follow. But familiarity is not the same as opportunity. Some of the world’s major growth themes are playing out in markets, sectors and companies that many Australian portfolios may not fully capture.

Source: FactSet, MSCI, J.P. Morgan Asset Management. Share of global market capitalisation is based on float-adjusted MSCI data. Percentages may not sum to 100% due to rounding. Guide to the Markets – Australia – On the Bench. Data as of 30 June 2026.

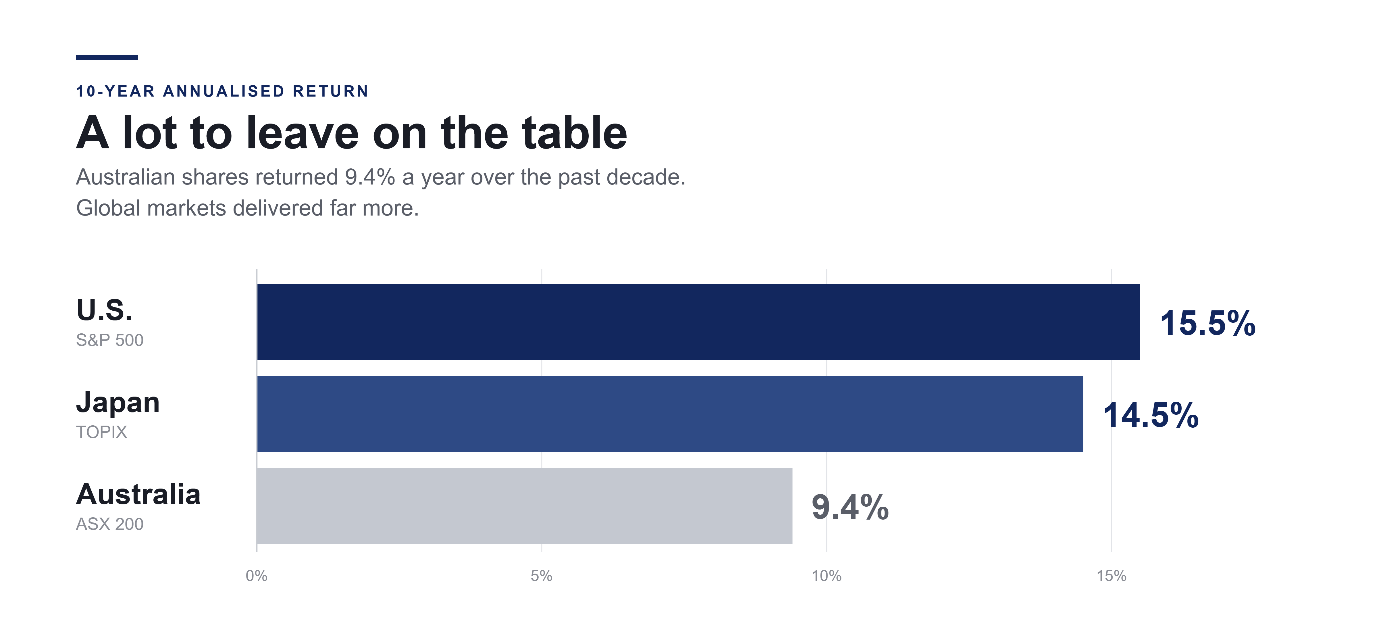

Being a small share of the global market wouldn’t matter as much if Australia was consistently outperforming. However, it made 9.4% annualised returns over the past 10 years, which sounds good until you realise that, over that same time period, the US returned 15.5% and Japan 14.5%. That’s a meaningful gap.

Source: FactSet, MSCI, Standard & Poor’s, TOPIX, J.P. Morgan Asset Management. Annualised return (Ann.) and volatility (Vol.) covers the period 31/03/2015 to 31/03/2025. Volatility is based on local currency returns. Japan: TOPIX first section; Australia: ASX 200 Index; U.S.: S&P 500 Index. All indices are total returns. Past performance is not a reliable indicator of current and future results. Guide to the Markets – Australia. Data as of 31 March 2026.

Not only that but, as an investor, it’s important to remember that buying equities is buying expected future earnings growth, and by focusing on Australia you may be missing out on some of the major growth themes in investing today. While the Australian market might have ridden high on the mining boom and trade links with China in the past, it has limited exposure to some of today’s key growth drivers.

Take AI. The opportunity is not only in US technology companies, but in the infrastructure behind them, including semiconductors, memory, data centres, power generation and electricity networks. Much of that spending flows through global supply chains, including markets like Korea, Japan and Taiwan, while Australia has only limited exposure.

Source: J.P. Morgan Asset Management; (Left) Bloomberg; (Right) Ethan Mollick “One Useful Thing,” Artificial Analysis AI, Epoch AI. *Hyperscalers are the large cloud computing companies that own and operate data centers with horizontally linked servers that, along with cooling and data storage capabilities, enable them to house and operate AI workloads. **Reflects cash flow before capital expenditures in contrast to free cash flow, which subtracts out capital expenditures. PhD level reasoning is measured by the GPQA score. Cost per million tokens refers to the average API price to process one million input and output tokens (weighted 3:1). The companies/securities included are shown for illustrative purposes only, the information stated should not be construed as offer, research, or recommendation to buy or sell. Guide to the Markets – Australia. Data as of 31 March 2026.

AI is perhaps the most obvious example, but it is far from the only growth opportunity sitting outside the Australian market. For example, European countries are spending heavily to secure reliable and sustainable energy supplies; Germany alone has announced a €500 billion package. At the same time, geopolitical tensions are driving higher defence spending across Europe.

As well as missing out on growth opportunities, investors should be aware the Australian share market is relatively concentrated in financials like major banks, and materials/mining. There is nothing inherently wrong with these sectors or businesses, but a well-constructed portfolio often seeks to diversify its sources of return across industries, economies, business models and growth drivers.

Familiarity is not the only driver of home bias. Currency has also traditionally been a barrier, but many investment products now offer hedged and unhedged options, allowing investors to reduce much of that currency risk if they choose. Then there’s the question of tax. Franking credits are often cited as a reason to favour Australian shares. They can provide a valuable income benefit, but investors should consider their objectives and be careful not to confuse income with growth. Franking credits may enhance returns, but they are not a growth strategy and do not provide access to the companies, sectors and themes driving global economic expansion.

Access has changed too. Modern investment platforms and ETFs provide broad exposure to global shares and other asset classes in just a few clicks, often at relatively low cost.

As these barriers have fallen, investors now have several practical ways to build global exposure. The question is where to start.

Investors can of course buy individual companies directly. However, with global indices such as the MSCI All Country World Index containing more than 2,000 companies, building a diversified portfolio this way can be challenging and time-consuming. It tends to make investors gravitate towards the brands that are familiar to them on the global stage, again leading to potential concentration risk.

A simpler approach is to invest through index funds or ETFs. These provide broad exposure to a wide range of companies and allow investors to seek market returns at a relatively low cost, offering far greater diversification than holding a handful of individual stocks.

While broad global index funds provide exposure to many of these opportunities, some investors may want to supplement this with a more active approach, particularly in areas where market leadership is changing rapidly and opportunities can emerge unevenly across sectors and regions. Markets are not static, and active managers seek to identify those opportunities and adjust portfolios as conditions change, rather than simply following the market.

Investors wanting a more active but still hands-off approach can invest in actively managed portfolios like the JPMorgan Growth Portfolio. This is designed for Australian investors who want professionally managed, globally diversified exposure without needing to select and rebalance individual holdings themselves – and it can be accessed through the Betashares Direct platform.

It combines exposure to Australian and international equities, alongside assets such as fixed income and alternatives, with allocations designed to support long-term wealth creation. Rather than maintaining a static allocation, the portfolio can adjust exposures as market conditions and opportunities evolve, providing investors with a professionally managed approach to global diversification.

Ultimately, home bias is understandable, but investors should ask themselves whether familiarity is causing them to overlook compelling growth opportunities. In a world where many of the most exciting opportunities are emerging beyond Australia’s borders, the cost of staying too close to home may limit long-term wealth creation.

Important Information

Diversification does not guarantee investment returns or eliminate the risk of loss. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors. Provided for information only, not to be construed as investment advice.