Tom Wickenden

7 minutes reading time

David Bassanese is taking a well-earned two-week break from work. In his absence Betashares Investment Strategist, Tom Wickenden, will continue Bass Bites weekly commentary.

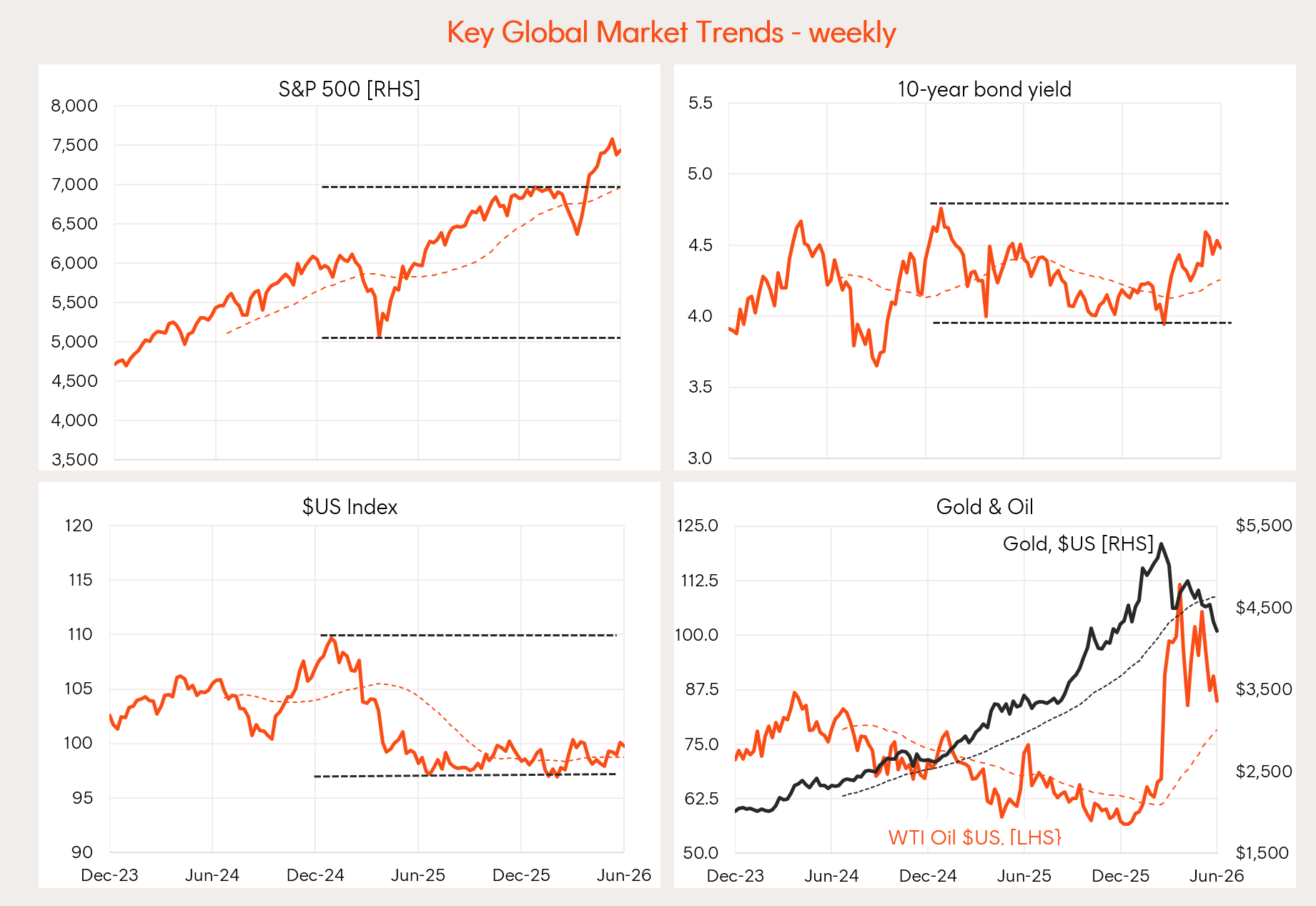

Global week in review: Cautious relief

US markets staged a modest recovery last week as US CPI came in line with expectations, oil eased on the potential for a peace deal to be signed this week, and SpaceX successfully IPO’d.

Source: Betashares, Bloomberg.

Markets rebounded to start the week before US CPI provided some relief, coming in line with expectations, even if at elevated levels. US May CPI rose 4.2% YoY, the highest since April 2023, with energy doing the heavy lifting rising 23.5% over the year, still reflecting the Iran supply shock. The result saw US bond yields pull back a little with no fresh hike panic.

Amongst other factors inflation at three-year highs sets up a pivotal Fed meeting this week, the first chaired by Kevin Warsh.

The major market event last week was SpaceX listing Friday on the Nasdaq, raising US$75 billion and marking the largest IPO in history. Shares closed the week up 19% making SpaceX the 7th largest publicly traded company in the world and Elon Musk a trillionaire.

The IPO marks the first of several AI-related mega-IPOs with Anthropic and OpenAI having filed to do so, although developments over the weekend have clouded the path forward for the AI rollout. The success of the IPO saw tech broadly rallying on Friday.

The major regulatory development over the weekend came when the US Commerce Department ordered Anthropic to suspend access of its recently released Fable 5 model for all foreign nationals worldwide, including those based in the US and even working at Anthropic, citing cybersecurity concerns. The suspension marks the first US export control applied to a commercial AI model and, if not resolved, will slow both the development and deployment of frontier AI models. The regulatory risk premium is now raised for AI and poses the most significant risk to date.

A final peace deal in the Iran war seems within reach as the most concrete framework to date, ‘Islamabad MOU’, has been circulating and acknowledged by Trump and Iran. The MOU’s headline terms include Iran reopening the Strait of Hormuz on its own terms while the US lifts its naval blockade within 30 days and temporarily waives sanctions, in exchange for Iran’s commitment not to pursue a nuclear weapon, with 60-day negotiations on enrichment to follow. Notably absent are Iran’s missile programme and proxy forces, and Israel is not party to the talks.

As of Monday morning, both sides have confirmed agreement. A formal signing ceremony is scheduled in Switzerland on Friday, with the Strait of Hormuz set to reopen the same day. Markets moved immediately: Brent fell more than 4%, US equity futures climbed 0.8% and Asian equities surged, Kospi up 5.3%, Topix +2.8%, ASX +1.3%. Implementation remains the key risk, but the direction of travel is clear.

Outside of the US, the ECB raised rates 25bps to 2.25%, its first hike since 2023, as policymakers moved to anchor inflation against the persistent energy price shock from the Iran conflict.

Global week ahead: Kevin Warsh’s debut and Islamabad MOU

Kevin Warsh will chair his first meeting at the Fed with the board’s interest rate decision due on Wednesday. While a hold is heavily expected for the meeting there are some key details that will start to shape the market’s expectations going forward. After Powell’s forward-guiding approach Warsh’s Fed may provide less guidance allowing the Fed to be more flexible. The first tell will come this week as the updated dot plots, Fed board members’ indication of where they think interest rates will sit in the future, are due.

With the deal now confirmed but not yet signed, attention turns to Friday’s signing ceremony and the implementation risks that remain, keeping the Islamabad MOU central to the global news cycle this week.

Elsewhere the Bank of Japan is widely expected to raise rates by 25bps to 1.0% on Tuesday as persistent yen weakness and Iran-driven energy inflation force the pace of normalisation. Combined with the RBA on Tuesday and the Fed on Wednesday, it is a rare triple central bank week, with three major economies navigating the same stagflationary crosscurrents from very different starting points. China retail sales and industrial production data also land this week, offering a read on the demand backdrop for commodities and iron ore in particular.

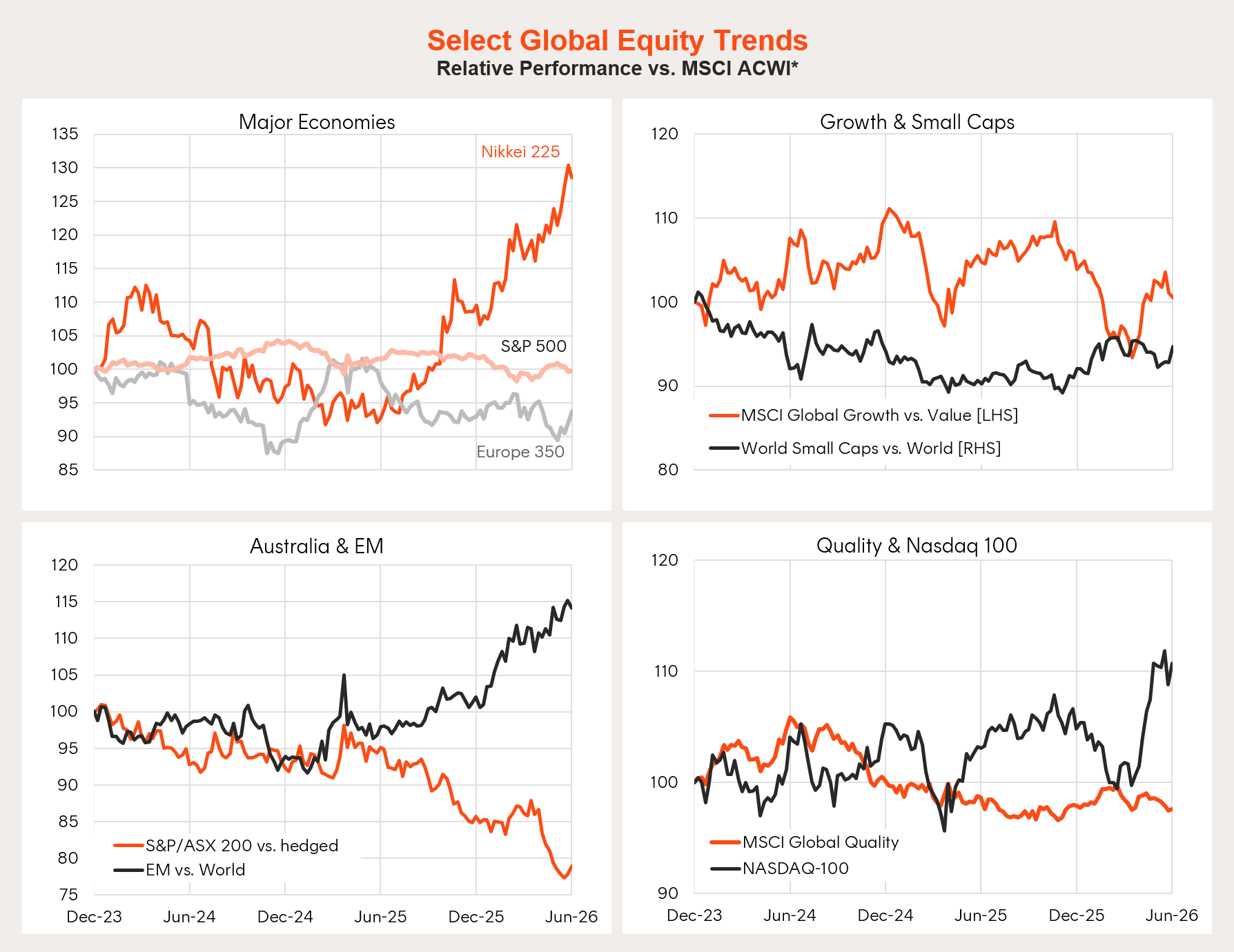

Global equity trends: Tech consolidation

Tech led the week’s recovery. Quality and Nasdaq names resumed outperformance through Friday as the market settles from the blowout payrolls report and in-line CPI removed more significant risk. The structural story remains intact however the Anthropic Fable 5 export ban introduces a meaningful regulatory risk to the AI trade that needs to be digested by markets.

Elsewhere, the Major Economies picture reflects the week’s risk-on tone. US led, Europe and Japan were more modest. Australia and EM ticked up but remain laggards on a relative basis; resource exposure means both are still sensitive to the Iran deal’s impact on oil and commodities.

*All but value factors. Local currency basis. Source: Betashares, Bloomberg

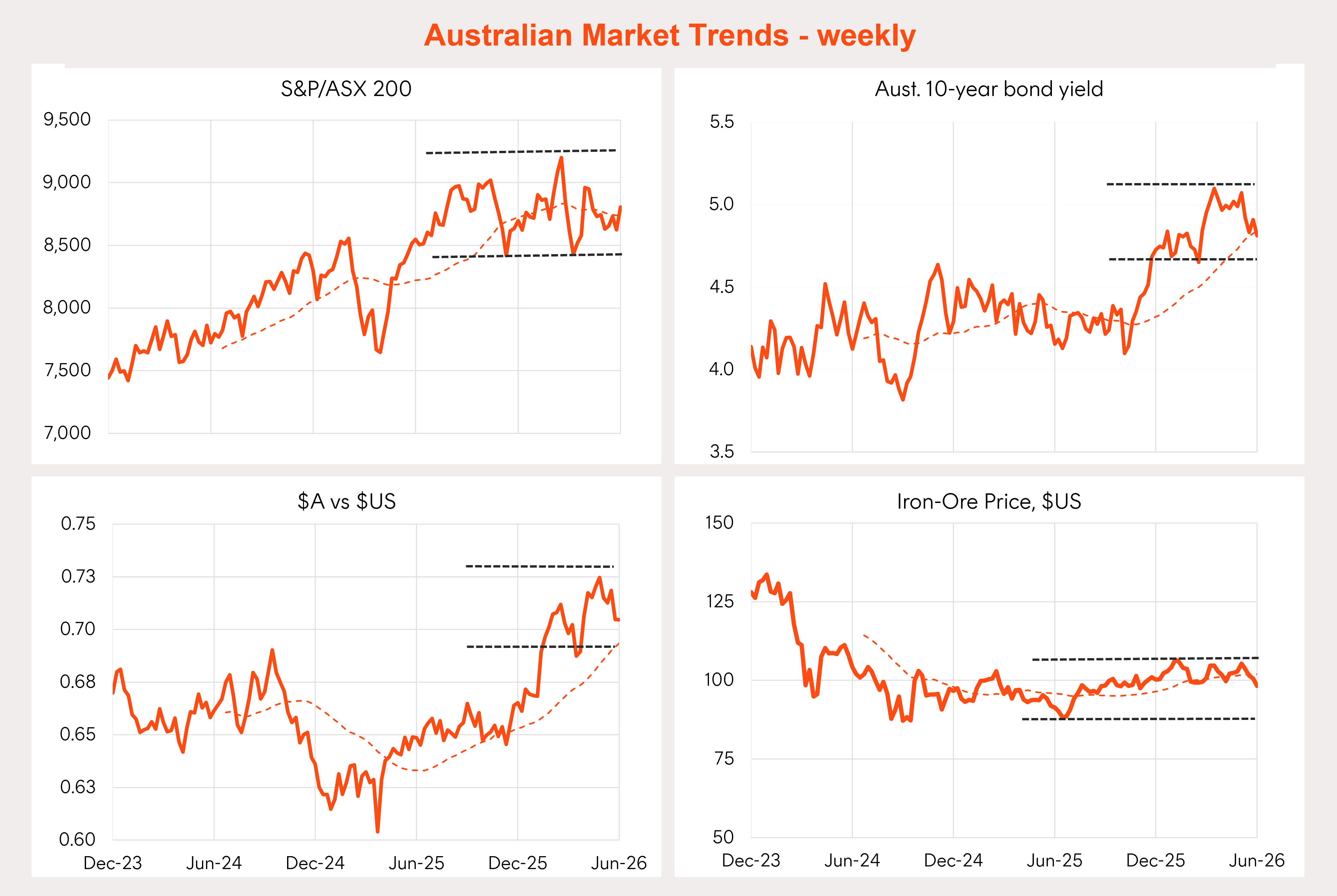

Australia week in review: Consumer sentiment near 50 year low

Australia’s market rallied 2.1% last week outpacing the US’ recovery however the consumer demand picture continues to soften as house price expectations fall.

Source: Betashares, Bloomberg.

The ASX 200 rallied 2.1% last week, outpacing the US recovery and fully recouping the prior week’s sell-off. Consumer Discretionary led the gains while Information Technology lagged with a rotation toward domestic cyclicals rather than the tech-driven narrative playing out in the US. The Australian dollar held steady at US$0.705 and the 10-year bond yield eased 10bps to 4.82%.

The RBA’s rate hikes seem to be doing the job as the demand picture softens. Consumer sentiment fell 2.9% to 80.6 in June, near its weakest in the survey’s 50-year history, with broad-based deterioration across components: family finances declined sharply, major purchase intentions remained weak, and house price expectations fell 14.9% month-on-month. The NAB Business Survey offered a modest lift in confidence.

The combination of three rate hikes and proposed budget changes has deflated the Australian consumer. One can only hope a peace deal in the Middle East and weakened domestic consumer can start to set a path towards rate cuts.

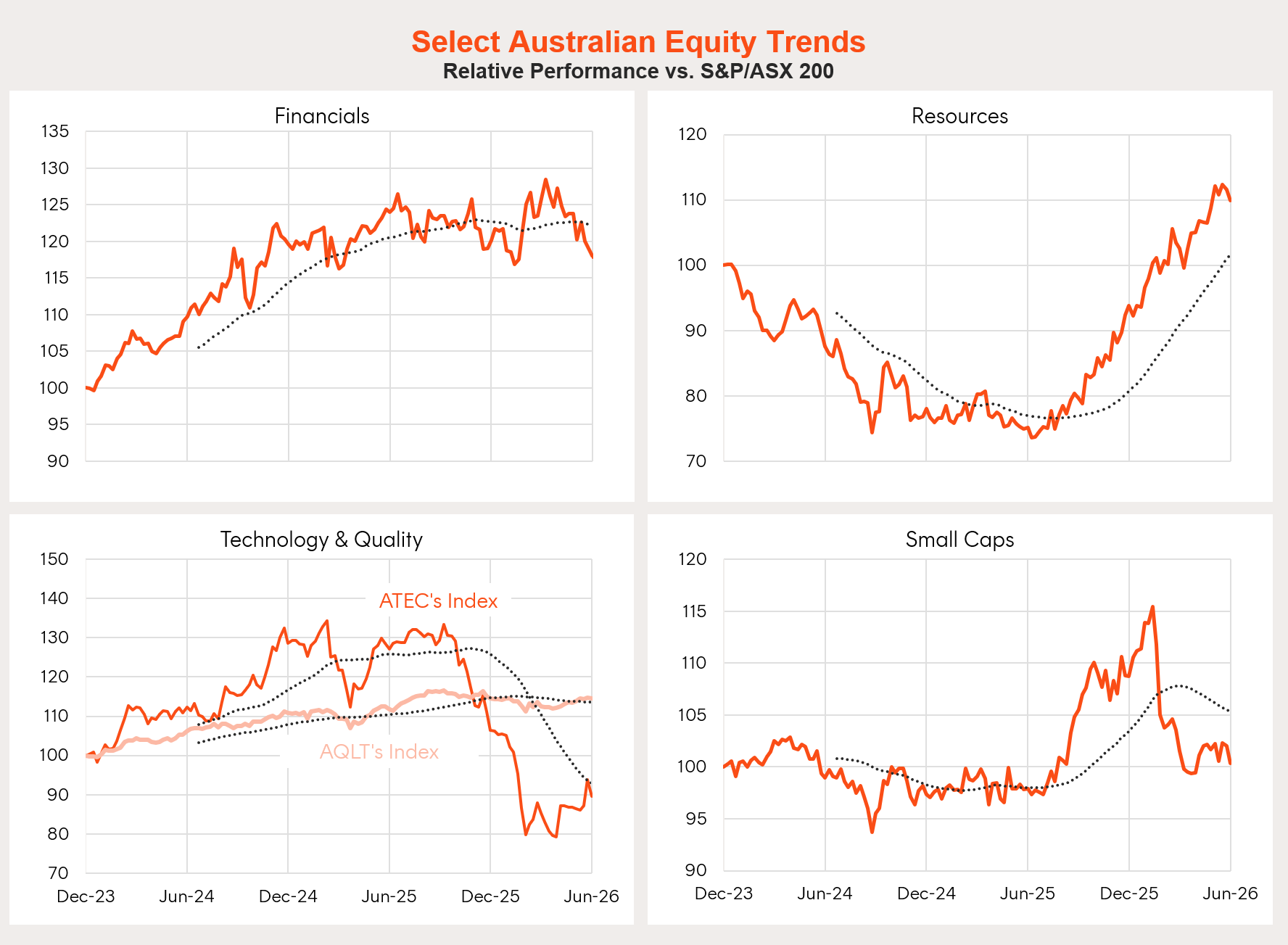

Local equity market trends: Rate relief drives the rotation

Last week’s ASX rally was driven by rate sensitive sectors as technology pared some recent gains. Consumer Discretionary, Consumer Staples and Property led the market higher as Australian 10yr bond yields fell 10bps.

Energy was effectively flat and Iran deal expectations priced in lower future oil prices, which weighed on domestic producers even as broader markets rallied. Materials and Financials both edged higher but underperformed the index, with iron ore’s softness from falling Chinese import volumes keeping a lid on the miners.

Source: Betashares, Bloomberg.

Australia week ahead: The RBA’s moment of pause

The RBA meets today and tomorrow, with the interest rate decision due at 2:30pm on Tuesday. Governor Bullock signalled as much in May, flagging that three consecutive hikes had given the board space to assess the incoming data. A hawkish bias is still expected with inflation remaining elevated however with a beaten up Australian consumer and a confirmed Iran peace deal now removing the key geopolitical overhang, this meeting could mark the start of a long pause for the RBA.

David will be back next week. Have a great week!

Tom