Parker Guan

4 minutes reading time

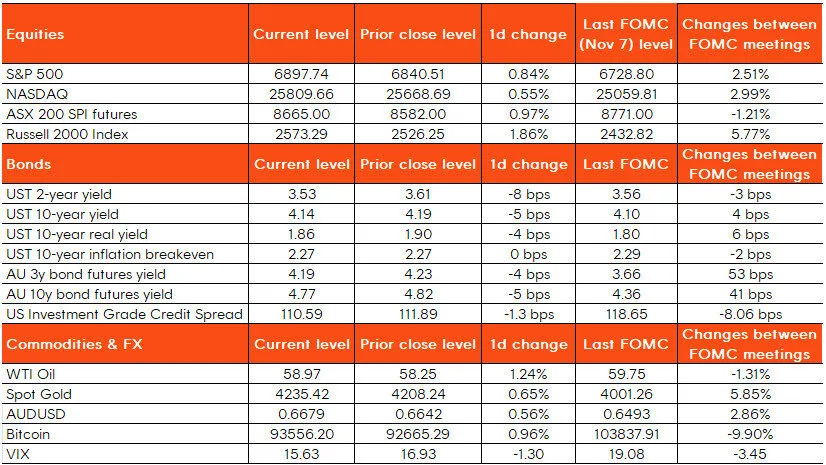

- The FOMC cut the benchmark interest rate by 25 basis points to a target range of 3.5%-3.75% in a 9-3 vote.

- The decision saw a rare three dissents: Governor Miran favoured a larger 50-bp cut, while regional Reserve bank presidents Jeff Schmid (Kansas City) and Austan Goolsbee (Chicago) dissented for holding rates steady.

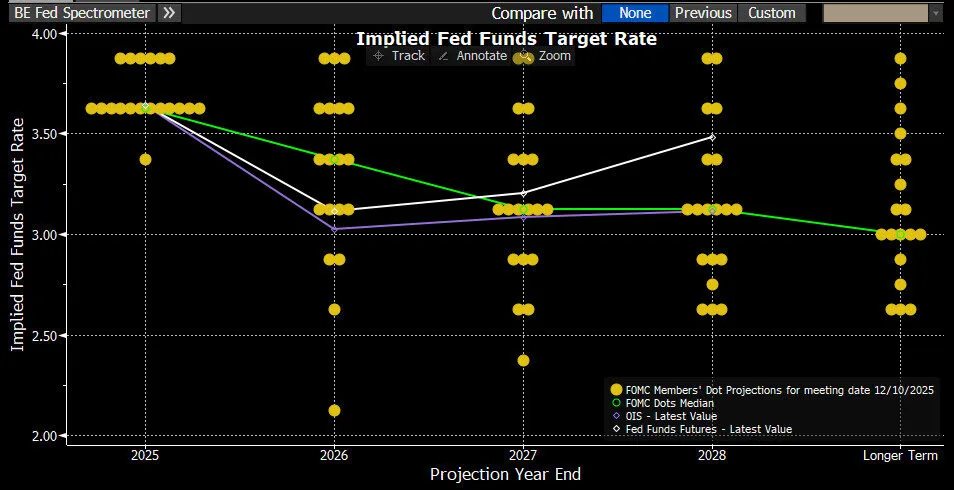

- The updated official “dot-plot’s” median projection forecasts one additional quarter-point cut in 2026, while the bond market continues to price in two cuts by end of 2026.

- The statement was tweaked to say the committee will consider the “extent and timing” of future adjustments, keeping a more neutral stance while opening the opportunity to hold rates steady if data deteriorates.

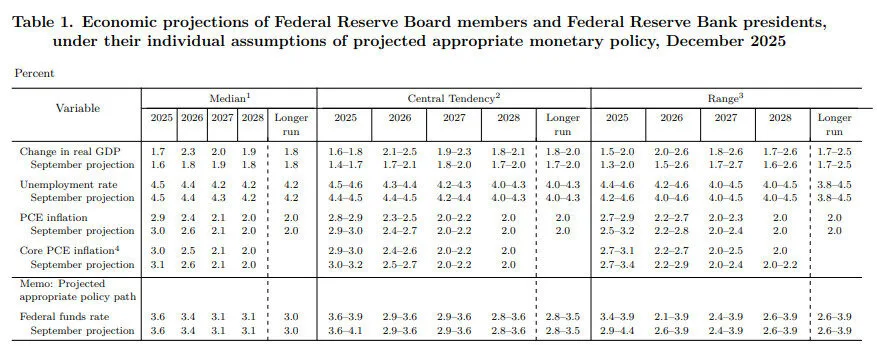

- In the new economic projections, the committee significantly upgraded its 2026 GDP growth forecast (from 1.8% to 2.3%) while also lowering inflation forecast (from 2.6% to 2.4%), suggesting a “Goldilocks” outlook.

- The Fed will immediately begin purchasing short-term Treasury securities on 12th December to maintain ample bank reserves. However, Powell clarified in multiple occasions that this is not a monetary policy signal but a liquidity management move.

Market reaction

Desk Commentary

While there were no surprises in the action-packed December FOMC meeting, the key takeaway is the dovish tone from Powell’s comments during the Q&A session. It is clear that Powell is more concerned about further labour market weakness and less so about inflation accelerating, while remaining hopeful about productivity gains. In his comments, he suggested the labour market’s payroll increases are likely to be overstated, while also attributing the elevated inflation to “temporary” tariff impacts. The risk tilting toward labour market weakness is probably the key driver for today’s rate cut.

Where does this leave us? It will be interesting to see if US Treasuries can defy global reflation trends, with countries such as Canada, Japan, NZ, and Australia all pricing in rate hikes in 2026. Investors may hold different views on where US yields go from here. For investors who are believers of Fed’s dovishness, US10 could be the preferred exposure to benefit from further rate cuts. If investors are more worried about a “policy-error” where inflation might over-shoot, UTIP might be a better exposure in addition to recent moves in yields have been driven by real yields.

Another key theme to keep an eye on is the downward pressure on the USD. This could support AUD-hedged products. As the Fed becomes the standout in continuing its easing cycle, the broad USD could suffer from further depreciation pressure, and the AUD/USD hedging carry is also soon due to become positive.

Figure 1: December 2025 ‘dot plot’

Figure 2: December 2025 economic projections

Figure 3: AUD showing momentum against USD weakness

Figure 4: US 10yr real yields have been the main driver for recent yield movements