Hugh Lam

5 minutes reading time

Emerging market equities were a standout in 2025, driven by Asian technology companies’ central role in the US AI capex cycle and a weaker US dollar. The broad MSCI Emerging Markets Index outperformed the S&P 500 by 13.4% p.a. for the full calendar year, in local currency terms, despite weakness in India.

No longer are emerging markets reliant on traditional sectors such as agriculture and cheap goods manufacturing but have instead transitioned to become leaders of the new world in domains covering technology and finance.

While investor positioning has historically been light to these regions, we saw a resurgence in interest last year as allocators seek to diversify US-centric global equity allocations. We believe strong earnings growth and a re-rating higher in valuations could see significant emerging markets outperformance continue in 2026, particularly in Australian dollar terms.

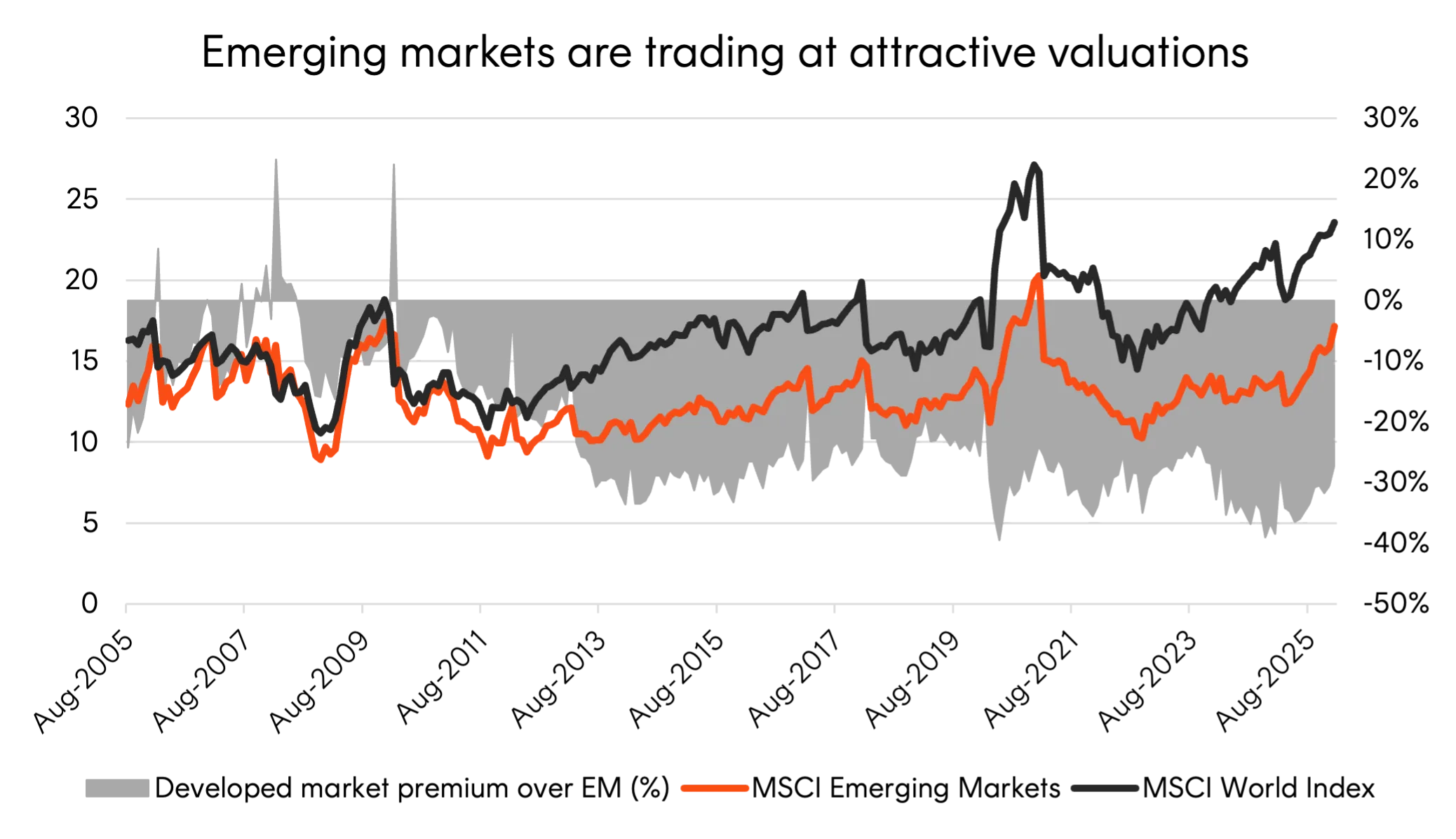

Valuations, earnings growth and structural support align

The MSCI Emerging Market index currently offers higher earnings growth potential than developed markets while trading at a near 30% discount – in terms of PE multiples.

Source: Bloomberg. As at 30 January 2026. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Much of that earnings growth is being driven by Asian based technology companies that can offer a cheaper way to play the AI trade compared with the US megacaps. For example, Taiwan Semiconductor Manufacturing Company (TSMC) and Korea’s SK Hynix and Samsung remain central suppliers to the US data centre build-out, while Chinese internet platforms like Alibaba and Tencent have re-emerged as rising contenders to the incumbent US AI leaders.

Meanwhile, after underperforming in 2025 due to weaker than expected corporate earnings, India’s economy and private sector are generally expected to rebound in 2026. The recovery should be driven by ongoing structural reforms, improving infrastructure, tax cuts and lower interest rates, with a recent US trade deal acting as a crucial catalyst for investors to re-enter the market.

The renewed commodity supercycle should also support Latin American countries like Brazil, Peru and Chile with terms of trade heavily influenced by exports of soy, iron ore and copper.

Finally, a weaker USD and an easing Fed could provide additional tailwinds for emerging markets countries by lowering USD denominated debt servicing costs and encouraging foreign capital inflows.

What is the best way to invest in emerging markets?

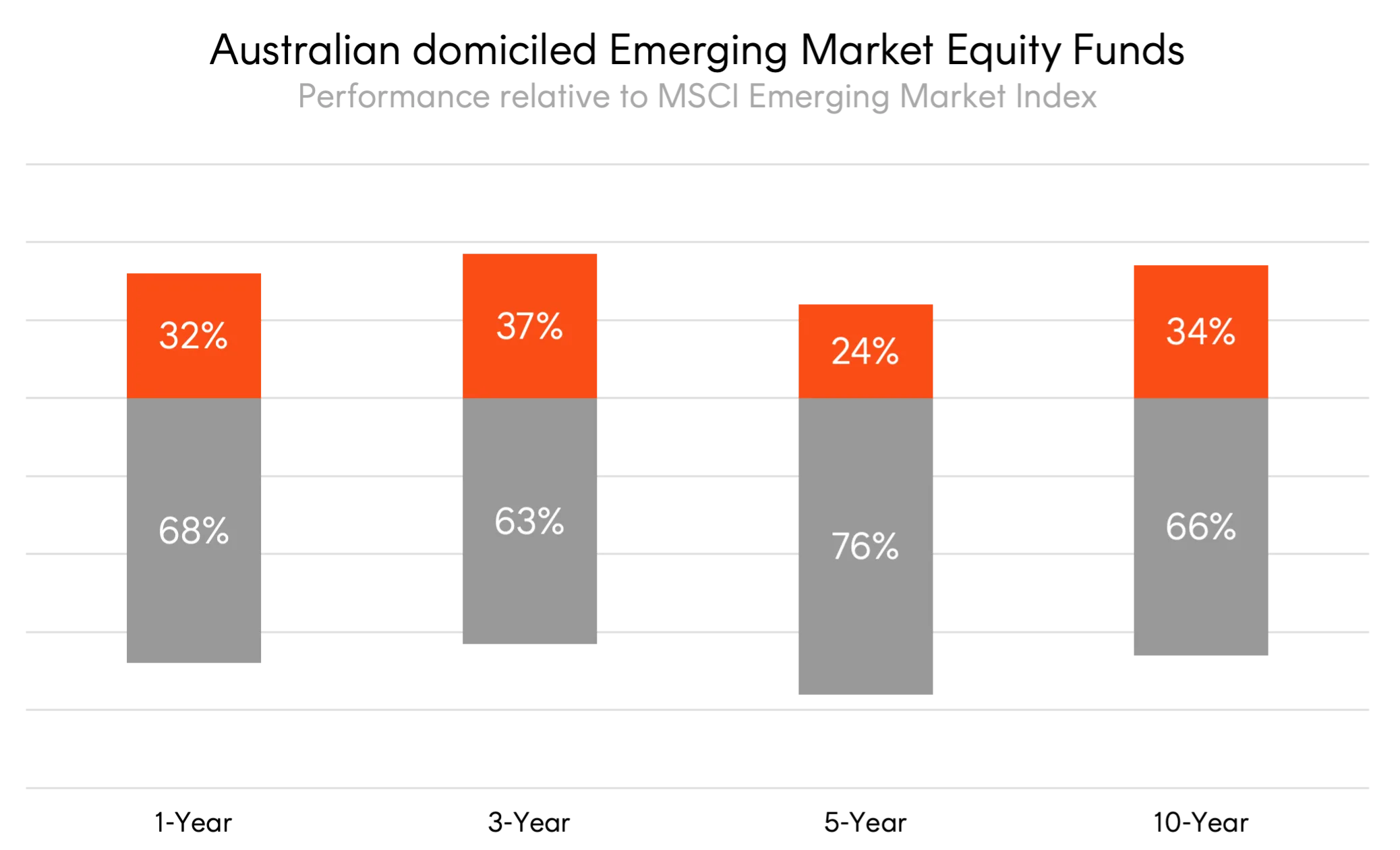

Investors have had limited choices when gaining exposure to emerging markets for some time. Active managers struggle to consistently add value in this region given the disparity in returns between underlying regions and sectors within them. Morningstar data shows that many Australian domiciled emerging market equity funds have underperformed the MSCI Emerging Markets Index as a result.

Source: Morningstar Direct. As at 30 June 2025. Analysis across 29 Australian domiciled Emerging Market Equity funds. Past performance is not an indicator of future performance.

Additionally, passive emerging market exposures have had relatively high management fees, underlying costs and high tracking error due to direct physical replication (i.e., holding all securities of an index) approaches typically used.

Instead, the BEMG MSCI Emerging Markets Complex ETF seeks to overcome these issues mentioned above by providing an efficient, cost-effective and tax-efficient exposure one might expect from an Australian domiciled and ASX traded ETF.

BEMG invests into an underlying fund managed using a swap-based replication method that seeks to ‘receive’ the performance of the MSCI Emerging Markets Index, while avoiding the regulatory hurdles, low trading liquidity and high execution costs that other vehicles would typically incur when trading in this region.

At a high level, the three key benefits that BEMG’s structure provides compared to other emerging markets ETFs available in Australia include:

- Cost-effective – 0.35% p.a. management fee, making BEMG one of the most cost-effective ETFs of its kind in Australia.

- Tax efficient exposure – the underlying swap-based non-distributing UCITS vehicle improves tax efficiency including by not incurring upfront capital gains tax on the sale of Indian securities.

- Efficient index replication – Enhanced replication efficiency where an index is more complex to replicate such as emerging markets and can provide more efficient tracking of the index.

For more information on the tax efficiency and structural benefits of the BEMG please refer to the FAQs available on the Fund Page here.

Investment implications

After years of underperformance and under-allocation, emerging markets present a compelling opportunity. The convergence of cheaper relative valuations, improving fundamentals across multiple regions, and structural exposure to secular growth themes like AI creates an attractive risk-reward backdrop.

For Australian investors, BEMG now offers an efficient and cost-effective way to access emerging market opportunities. Are you still underweight emerging markets?

For more detailed information you can visit BEMG’s fund page here.

There are risks associated with an investment in BEMG, including market risk, emerging markets risk, currency risk and derivatives risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.