David Bassanese

6 minutes reading time

Many thanks to my colleague Tom Wickenden, Betashares Investment Strategist, for handling Bassanese Bites over the past two weeks. Reviewing developments in my absence, it’s apparent many of the markets’ enduring themes remain in place: Iran, AI and an emerging risk of US Fed rates hikes. Local news remains generally depressing!

Global week in review: Peace hopes continue

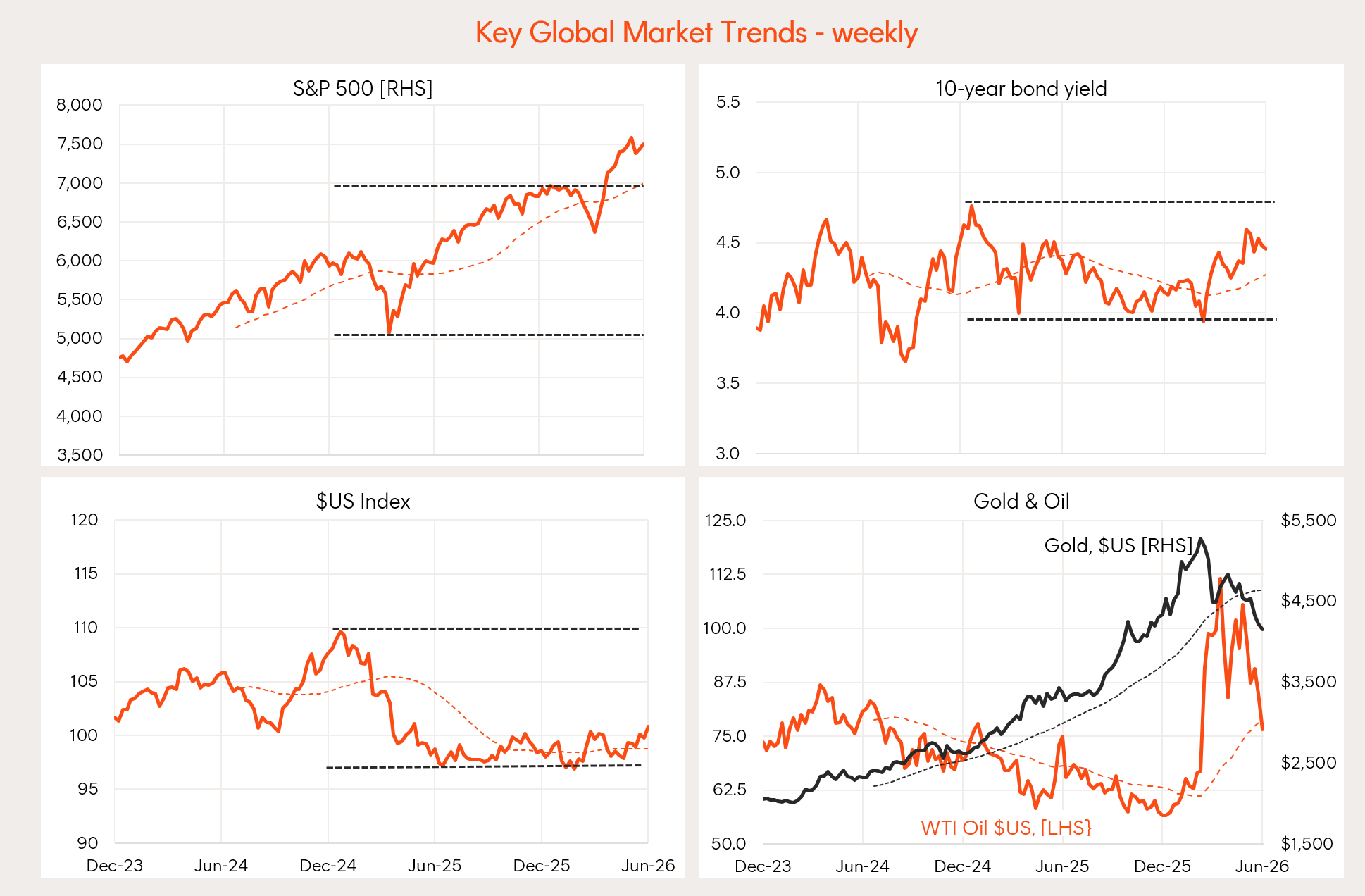

US equities lifted the 2nd week in a row following a major announcement that both the US and Iran had agreed to a peace deal. Oil prices dropped further and US bond yields eased, though the $US also firmed which did not help gold prices.

Source: Betashares, Bloomberg

While the peace deal details remained sketchy, reports suggest the demands on Iran were relatively light, consistent with the view that President Trump is increasingly keen to extricate himself from this ongoing Middle East quagmire. As Trump himself said, he was keen to strike a deal to avoid “economic catastrophe” as he was hopeful it would mean “oil prices down, equity prices up”.

The other major news over the week was the Fed’s widely expected decision to leave interest rates on hold. That said, markets were unnerved by the updated “dot plot” of Fed rate expectations, with 9 of 18 Fed members now anticipating one rate hike by year end.

Some central banks are not waiting. As was the case in Europe the previous week, the Bank of Japan lifted rates 0.25% last week to 1.0%.

Trump’s hopes of getting Iran behind him, however, were delt a blow over the weekend with Iran walking out of proposed peace talks in Switzerland, due to Israel’s continued attacks in Lebanon and Trump’s threats of further attacks.

Indeed, Trump over the weekend again threatened to take over the Strait of Hormuz and impose his own tolls! Of course, if he could control the Strait the war would be already over – the harsh reality is that US ships would be sitting ducks for Iranian drones and missiles.

Of course, helping to support markets meanwhile remains the AI boom, with optimism receiving a boost from the SpaceX IPO. Talk of bubbles and AI disruption is taking a back seat for now, though ripples a few weeks ago highlight the market’s vulnerability to a more hawkish pivot by the US Fed.

For Trump, it remains a race against time – and the Iranian’s know it!

Global week ahead: US inflation

Focus will no doubt remains on the US-Iran peace talks this week. In a sense, talk of a deal remains the gift that keeps on giving: markets suffer a modest setback when peace talks are delayed, then rally strongly on renewed hopes. This is likely to remain the case until such time as global oil shortages finally result in much higher oil prices, a feat which has so far been remarkably avoided.

On the data front, the key highlight will be the US private consumption expenditure deflator, with core prices expected to lift 0.3%, dragging up the annual rate from 3.3% to 3.4%. This is still uncomfortably high, though markets are waiting on the Fed to express more impatience than it has to date.

Global equity trends: Tech powers on

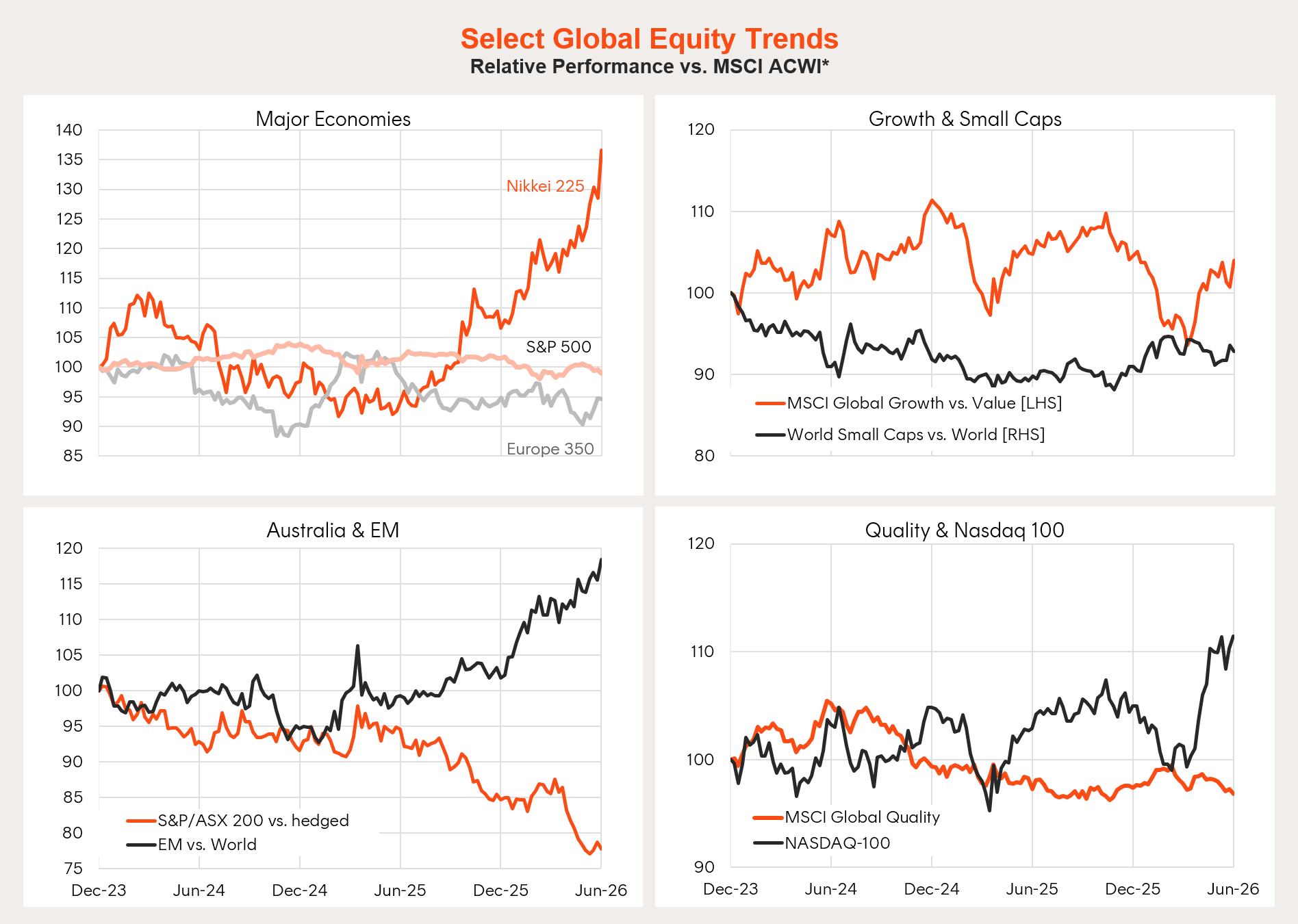

Major global market equity trends continue to favour anything AI-related. This is supporting not only the NASDAQ-100, but emerging markets and Japan to the extent that they contain major non-US technology companies, especially in the now very popular hardware space.

*All but value factors. Local currency basis. Source: Betashares, Bloomberg

Australia week in review: hawkish hold

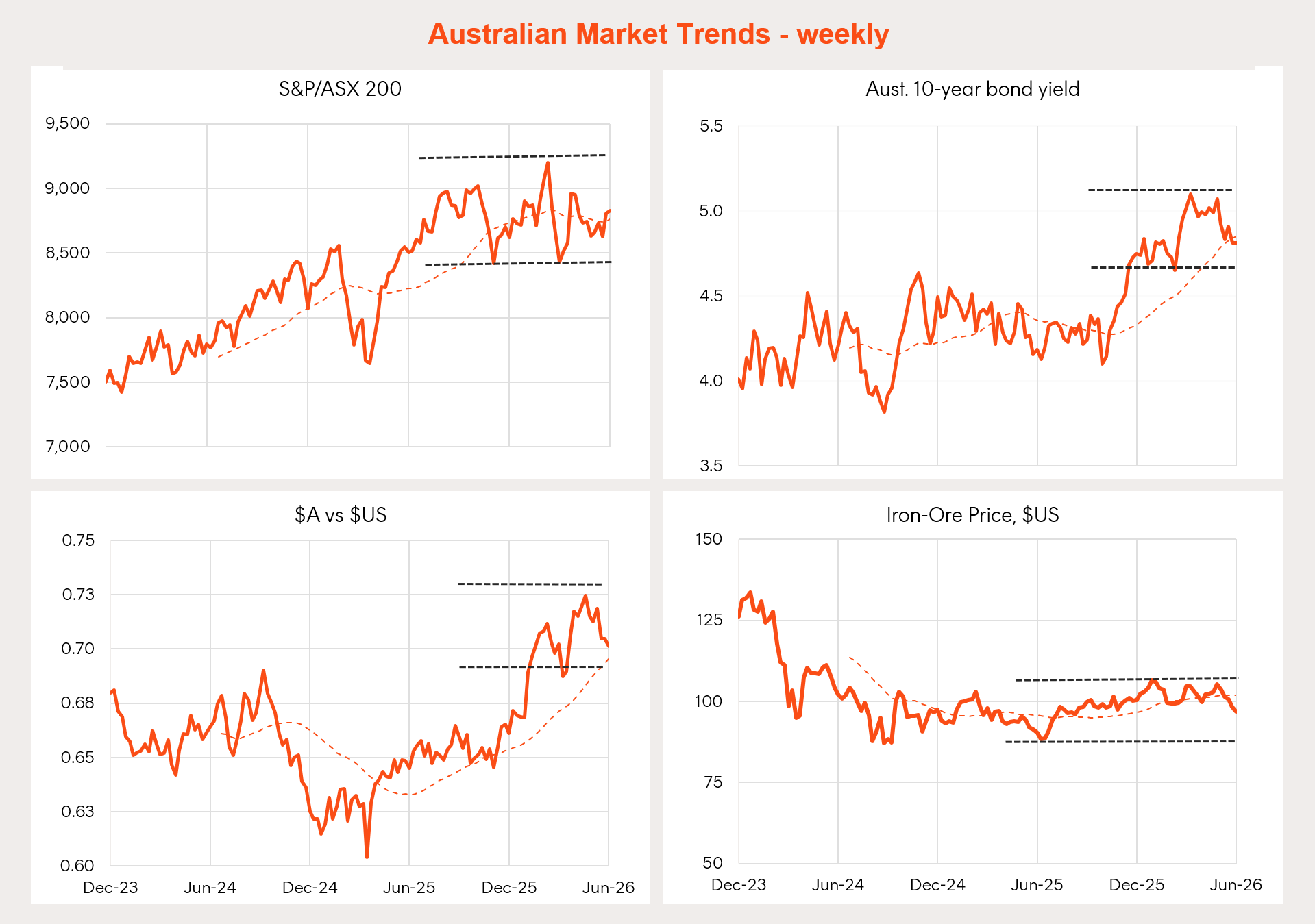

The local market eked out a small gain last week, with the RBA leaving rates on hold though warning there could be more rate hikes to come.

Source: Betashares, Bloomberg

Markets were perhaps a little disappointed with the “hawkish hold” from the RBA last week, though the Bank likely only wanted to play down the emerging talk of a potential rate cut. Much still depends on the inflation outlook though, with the Federal Budget succeeding in knocking economic sentiment and the property market, my base case remains that the RBA has done raising rates this year.

Yes, inflation is likely to remain high in the near-term, but the reality is that the economy is also slowing again – as evident with the modest 0.3% Q1 GDP gain. All that said, the potential avoidance of further rate hikes is the only local ray of optimism for the local economy and markets for the foreseeable future. The Australian equity market seems destined to continue to underperform its global peers.

Local equity market trends: technology bounces back

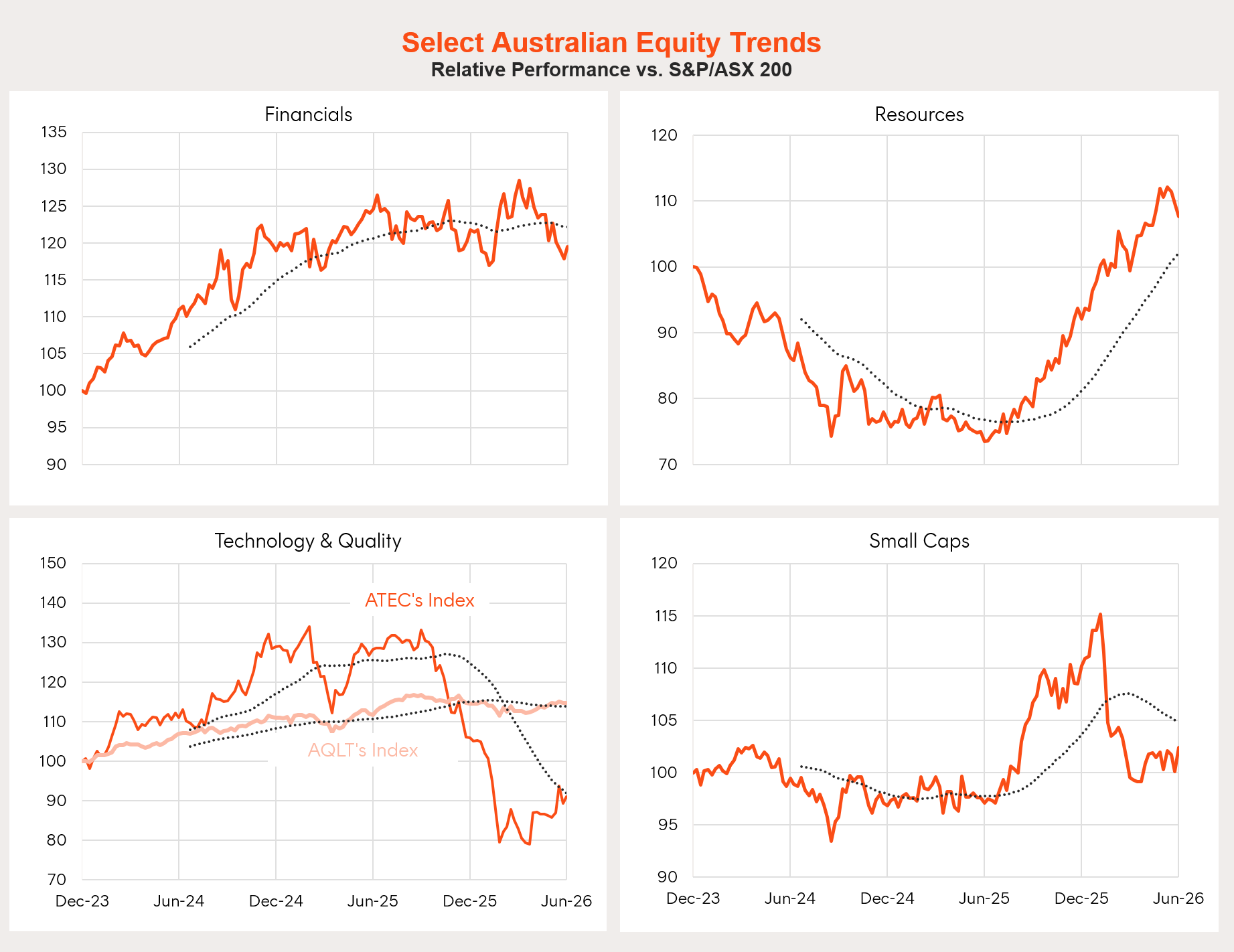

Both resources and financials have tended to underperform in recent weeks, with a welcome bounce back in technology, likely related to the ongoing global optimism around AI. Even small cap underperformance has bottomed out in recent weeks.

Source: Betashares, Bloomberg

Australia week ahead: CPI and employment

The monthly CPI and employment reports for May will be the local highlights this week. Easing petrol prices should see headline prices fall in the month, though underlying (trimmed mean) inflation is likely to remain firm. After seasonal related weakness in April, employment is also expected to bounce back in May, with the unemployment rate likely to ease back to 4.4% from 4.5%.

Results such as these should keep the pressure on the RBA. One point of interest will be whether emerging economic weakness and business pessimism results in a weaker than expected employment result. If so, that could be a case of “bad news is good news”, with markets rallying on optimism around no further RBA rate hikes.

It’s good to be back. Have a great week!