Tom Wickenden

11 minutes reading time

3 things we learned

Cautious optimism driving US markets higher

US markets climbed a wall of cautious optimism in Q3 2025, with the S&P 500 recording 23 new all-time highs1. A slowdown in disruptive policy from the US administration gave investors time to reassess the economic and market cycles.

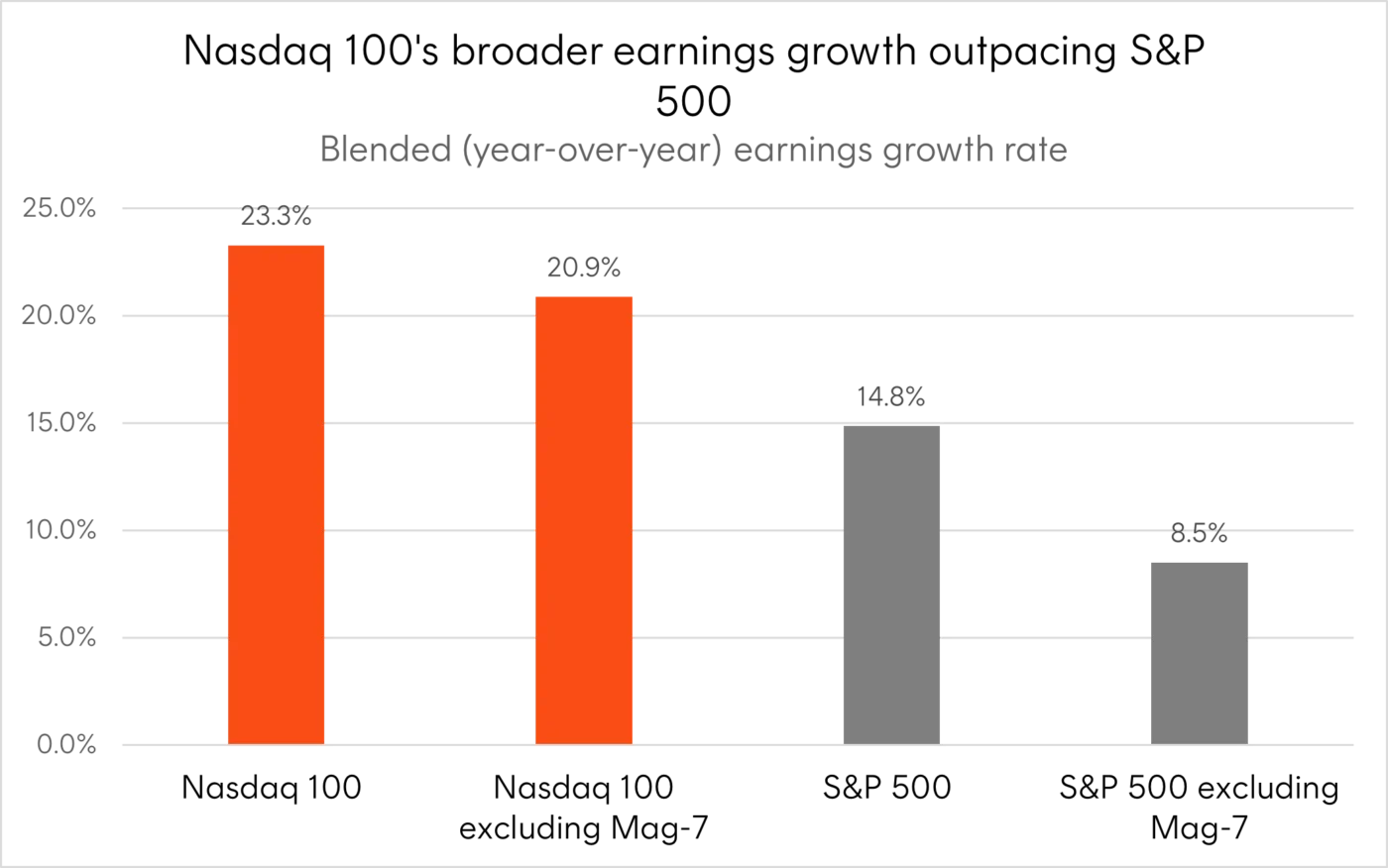

Corporate America once again steered the ship, as overly pessimistic downgrades ahead of Q2 earnings season set up a higher-than-average percentage of beats across sectors. This translated into impressive year-on-year earnings growth of 14.8% for the S&P 500 and 23.3% for the Nasdaq 1002.

Source: Nasdaq Global Indexes, FactSet. As of 25 August 2025.

Even more surprising, and promising, the broader US economy showed resilience, with revised data reporting 3.8% annualised growth versus earlier estimates of 3.3%, rebounding strongly from Q1’s 0.5% contraction3. A confident consumer, alongside signs of improving corporate capex plans, points to a positive outlook and potential for further upside surprises.

With the impact of higher tariffs on inflation still muted during Q3, the Fed shifted its focus to weakening US employment, allowing for a September rate cut. Rate cuts can support equity markets through multiple channels, including valuations, lower borrowing and financing costs, improved consumer purchasing power, and rising asset prices that encourage further spending and investment.

Source: Bloomberg, Betashares. September 1995 to September 2025. Personal consumption expenditures (PCE), also known as consumer spending, is a measure of the spending on goods and services by people of the United States.

While these conditions are often more supportive of mid and small caps, as we will discuss in the next section, the Nasdaq 100 remains our preferred US investment choice to gain exposure to the tech hyperscalers, who continue to lead the market in earnings, scale and innovation, alongside the growing cohort of Nasdaq 100 companies now leveraging AI to accelerate profits, creating a wider set of opportunities for exposure to future US equity growth.

Australian rotation under way

While the Australian macro picture is clearer than in the US, the broad market outlook is less convincing.

Trimmed mean inflation reaffirmed itself within the RBA’s target band in Q3, with a 2.7% June reading reported in July. Meanwhile, as noted in the RBA’s September meeting, labour market conditions remain steady and even a little tight. Together, these factors suggest a similarly favourable backdrop to the US, but without the same tail risks i.e. US debt levels, government shutdown, geopolitics, tariff related inflation impulse.

Like the US, Australian large caps have driven returns in recent year. However, in contrast, Australia’s large caps have not been the main source of earnings growth. In fact, during FY25 corporate reporting in Q3 the top heavy ASX 200 reported its second consecutive year of negative earnings growth4, underscoring the disconnect between price performance and underlying fundamentals.

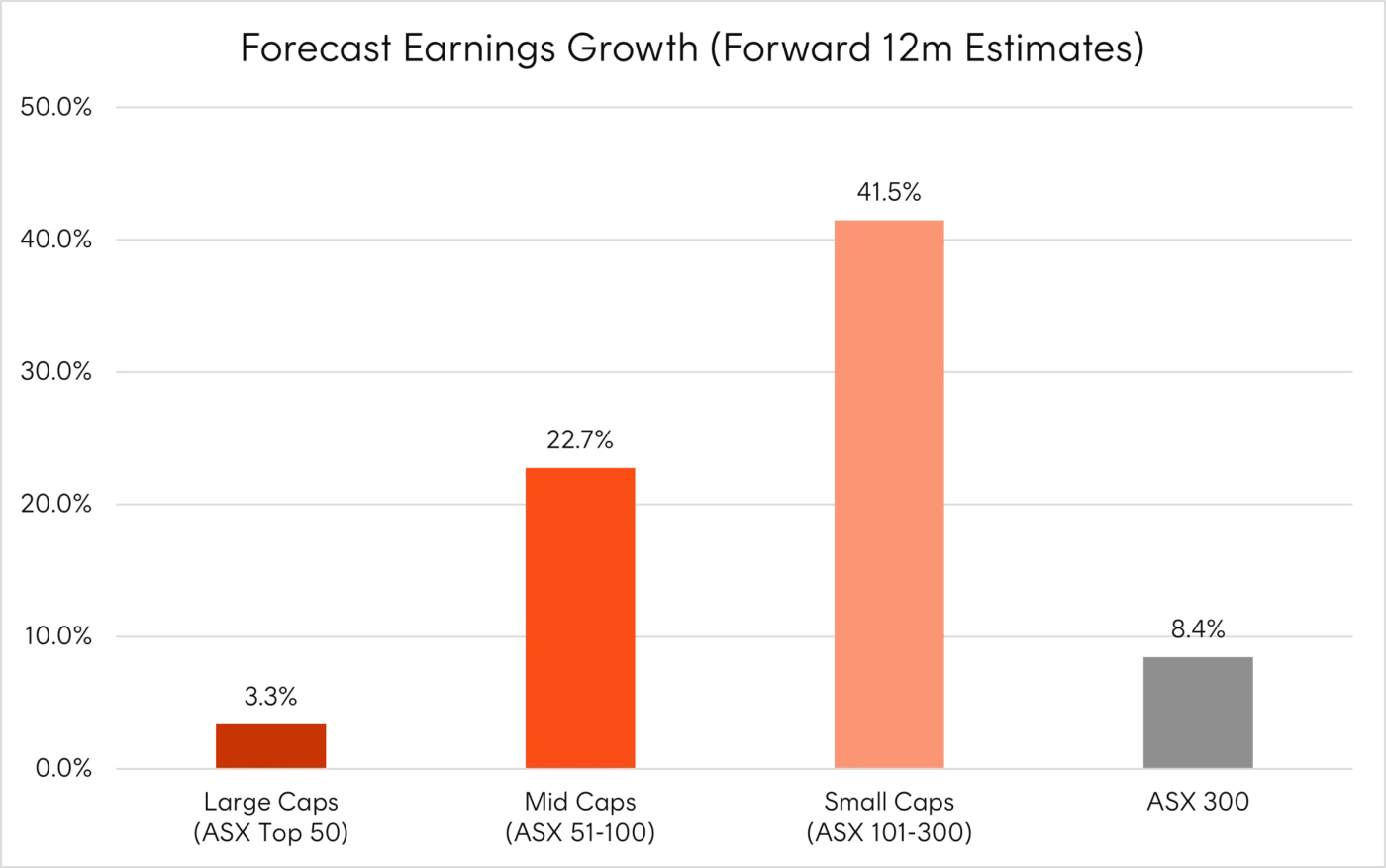

While Australia’s market does have pockets of strong earnings growth, for instance the Communication Services and Information Technology sectors, which delivered 26.9% and 26.4% YoY growth respectively5, these sectors are underrepresented at the broad index level – with better representation in mid and small cap indices.

For this reason, we have higher conviction in a rotation away from large caps into mid and small caps in the Australian market compared to the US. A rate cutting environment typically provides a stronger tailwind for smaller companies. At the same time, Australian investors are seeking alternatives to expensive lower growth blue chips with opportunities in the mid cap segment.

Source: Bloomberg. Earnings Growth reflects index weighted average of the forward 12 month estimates as at 17 September 2025. ASX Large Caps refers to the S&P 50 Index. ASX Mid/Small Caps refers to the S&P/ASX Mid Small TR Index. ASX 300 refers to the S&P/ASX 300 Index. Actual results may differ materially from estimates.

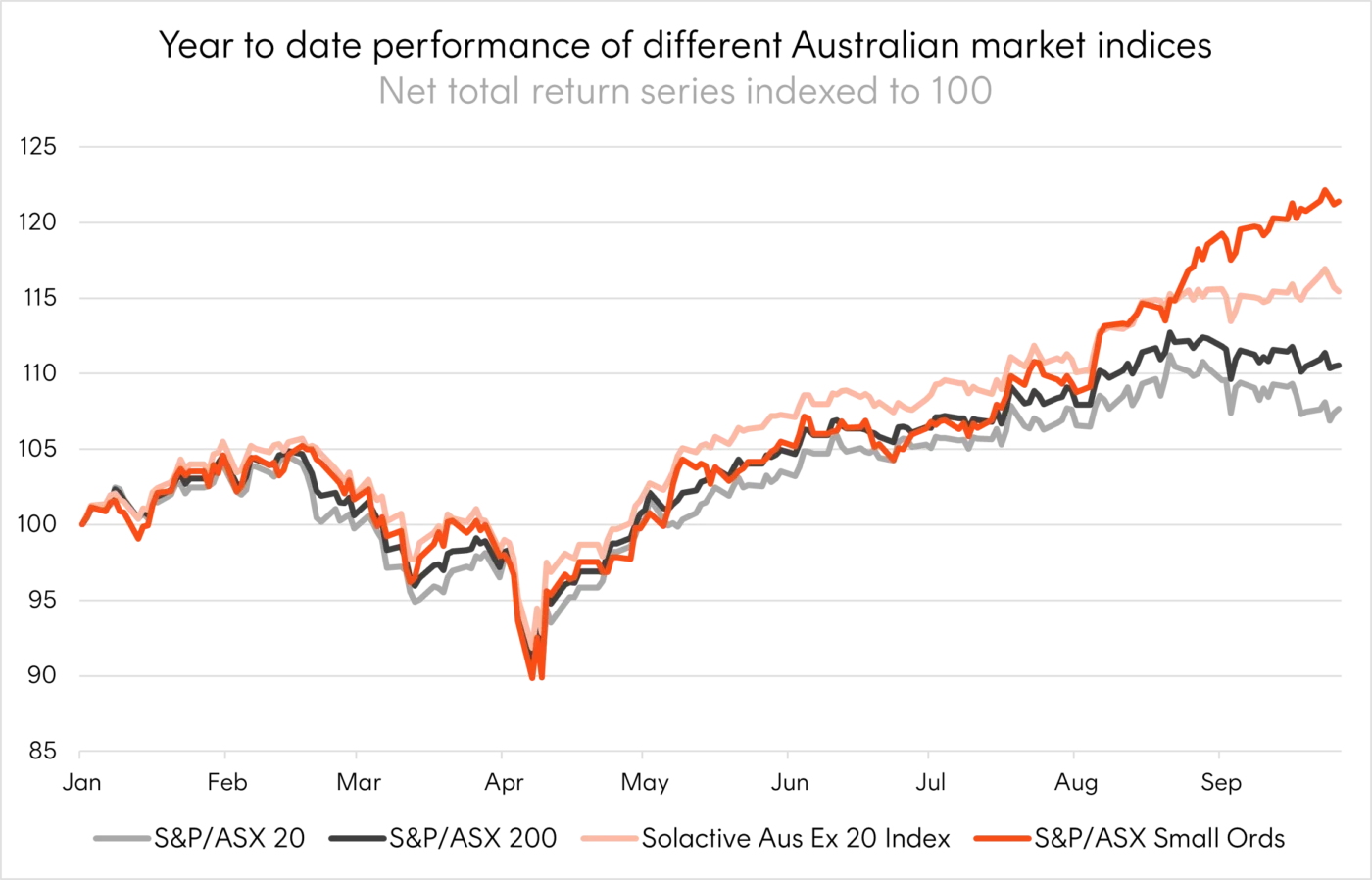

This rotation is already underway with the mid-caps and the ASX Small Ordinaries outperforming the broader market by 4.9% and 10.8% YTD respectively6. Notably this outperformance accelerated midway through August’s reporting season as the earnings picture across the index became clearer.

Source: Bloomberg. 1 Jan 2025 to 26 Sept 2025. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Asian technology continues breaking out

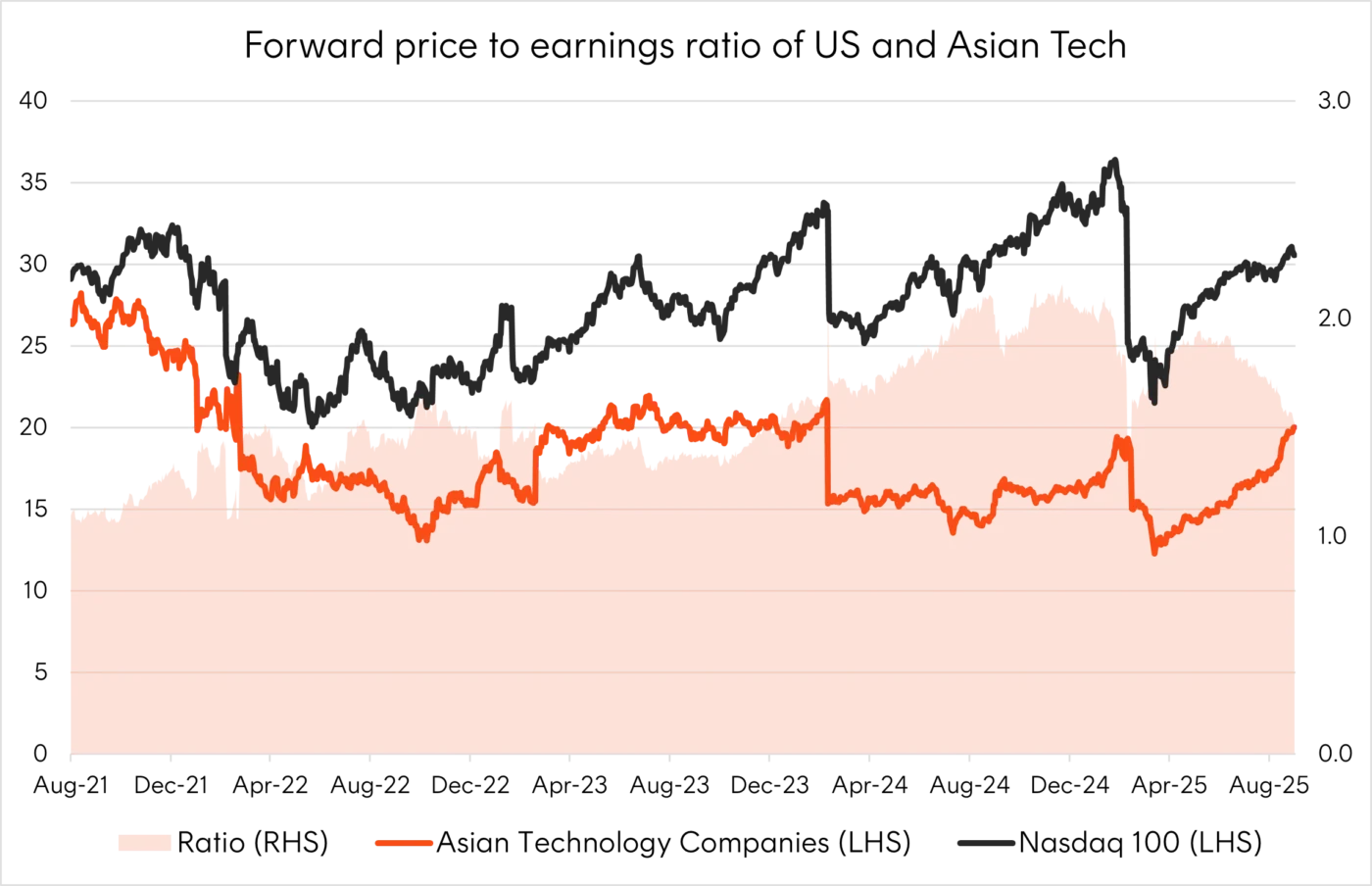

Asian technology companies extended their breakout in Q3, returning 21.1% and comfortably outpacing US peers, with the Nasdaq 100 up 9.8% over the same period7.

Momentum was fuelled by a string of positive announcements across the region, headlined by Alibaba’s Aspara Conference 2025 – a major summit on cloud and AI. The company unveiled its latest large language model, Qwen3-Max, and announced expanded investment in AI and cloud infrastructure, sending its shares up 19.4% in the 7 days from the start the event8.

Alibaba’s strong rally highlights one of the key drivers of short-term performance in Asian technology: valuation expansion. The company was trading on a forward P/E ratio of just 13.4x at the start of September9, underscoring the market’s appetite for underpriced growth. More broadly, Asian technology continues to trade at a 33% discount to US peers – though this gap has narrowed from 50% at the start of Q310.

Source: Bloomberg. August 2021 to September 2025. Asian Technology Companies represented by the Solactive Asia Ex-Japan Technology & Internet Tigers Index. Past performance is not an indicator of future performance.

While US hyperscalers have arguably earned their valuation premiums through a decade of consistent earnings growth, their Asian counterparts are still catching up. Encouragingly, alongside valuation expansion there are clear signs of strong fundamental growth within Asian tech, with both TSMC and SK Hynix reporting stronger-than-expected Q2 earnings during the quarter, reflecting their central roles in the AI supply chain.

Supported by government initiatives, expanding capex by Chinese hyperscalers seeking to rival US counterparts, and strong fundamentals from key Asian AI infrastructure suppliers, the region’s technology sector offers a compelling complement to US holdings and remains well positioned for further re-rating.

Source: Bloomberg. As at 9 July 2025.

2 charts we’re watching

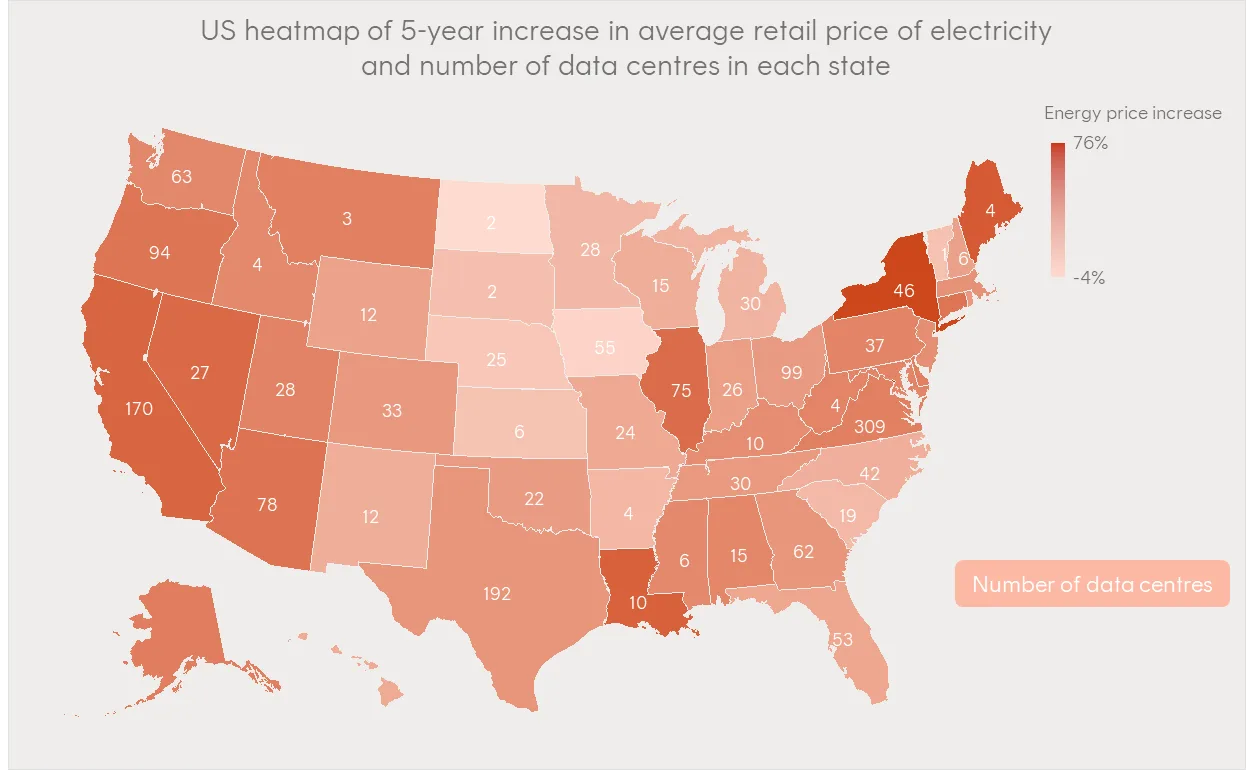

Energy impact of AI rollout

Source: U.S. Energy Information Administration, Aterio. 5-year increase in state by state retail energy prices from April 2015 to April 2025. Where energy and data centre date available.

The key bottleneck to the AI rollout could be the energy requirements to facilitate the amount of compute being built out. Even at this early stage the impacts are being felt by US energy consumers.

The heat map above charts the five-year increase in average electricity prices across US states, overlaid with the number of data centres in each state. While state-level data is less precise – given variations in data centre locations near border, grid capacity, and mitigating factors such as the renewable energy boom in southern Texas – it suggests that electricity prices are rising more sharply around states with higher data centre activity.

More granular analysis by Bloomberg of 25,000 individual Locational Marginal Pricing nodes indicates that electricity price increases are concentrated near data centres with a strong correlation between proximity to major compute hubs and price rises.

The risks around power consumption may be underappreciated as a potential disruptor to AI’s progress. This issue is likely more pronounced in the US, where energy capacity has not needed significant expansion for decades – contrasting with China, which is more accustomed to rapidly scaling energy infrastructure.

Separately, energy could be just as important an investment exposure to the AI rollout as the technology companies themselves.

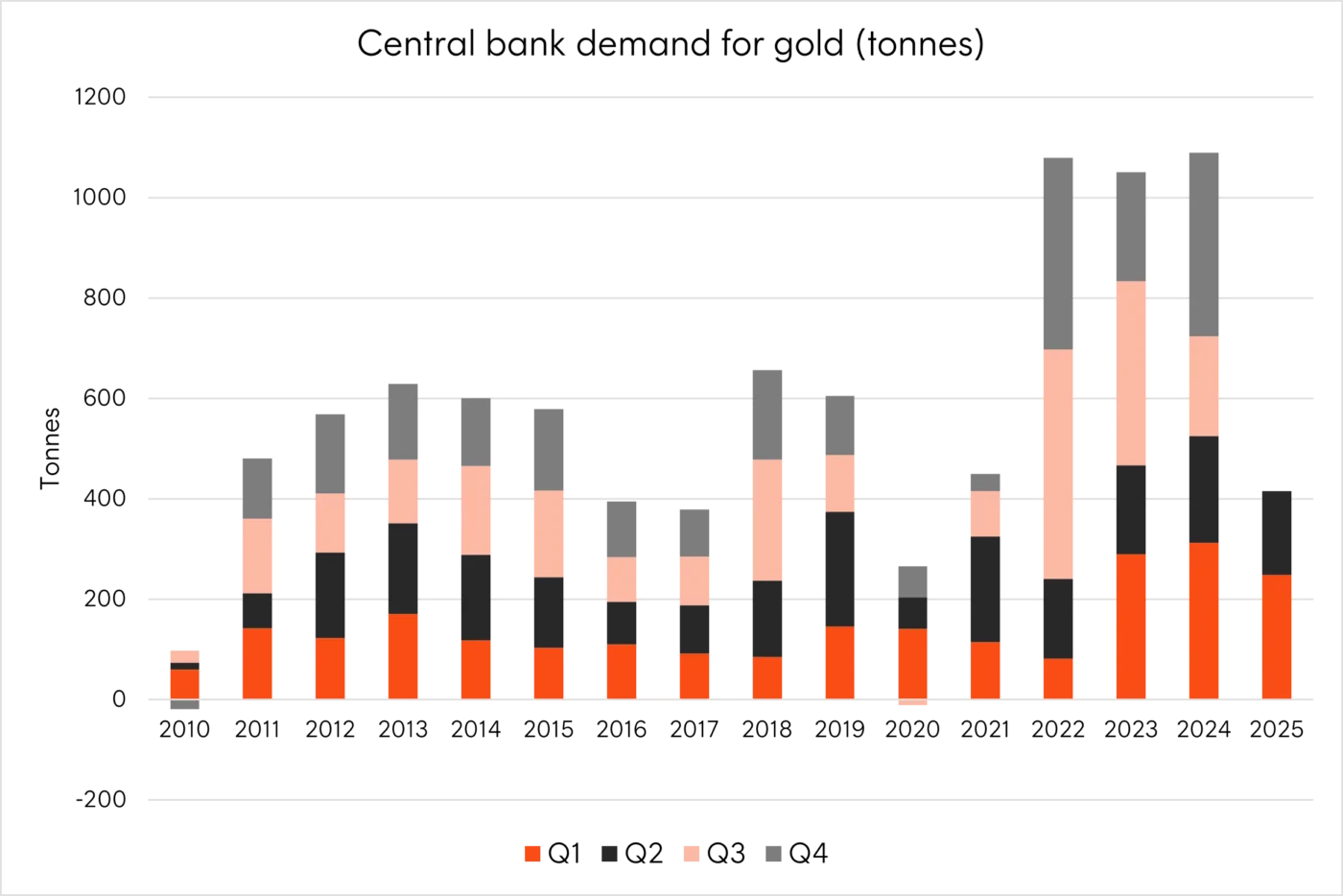

Structural support remains for gold’s rally

Source: World Gold Council. Gold Demand Trends: Q2 2025.

A key structural element to gold’s rally has been increased central bank buying. Data released during Q3 shows that while moderating a little in the first half of this year compared to 2023 and 2024 buying remains well above the 15-year average11.

Notably, during the third quarter, gold holdings as a percentage of international reserves surpassed US Treasury holdings for the first time since 1996, highlighting its growing prominence in central bank portfolios.

Alongside this structural support, cyclical factors, including a weakening US dollar and Fed rate cuts, continue to underpin gold’s appeal, notwithstanding its very strong run over the past few years.

1 question remaining

Where are we in this cycle?

Despite persistent recession concerns since the post-COVID rate hiking cycle, global economies have proven more resilient than expected. Growth is surprising to the upside, and corporate earnings have generally beaten expectations. Consumer spending remains solid, while businesses are showing greater confidence in future capex plans. These developments are more consistent with an early-cycle recovery than an imminent late-cycle slowdown.

At the same time, central banks have scope to cut from restrictive levels, providing additional support to activity. The question is how much the Fed and RBA will ultimately cut if economies continue to overdeliver, with employment the likely swing factor.

Looking ahead, investors may want to look beyond the economic cycle, as structural rather than cyclical risks could pose the bigger threat. In the US, key risks could be over-investment and excess capacity in certain sectors, disruptive technological shifts, energy bottlenecks, and antitrust. That said, Google’s ruling during the quarter – found to have illegally maintained a search monopoly but escaping with only a light penalty – suggests regulatory risk may be less severe than feared over the past few years.

In Australia, the challenge may be more about being tactical with allocations rather than leaning on the broader benchmark, which is top heavy with lower-growth names.

All in all, the backdrop appears constructive for further equity growth, with any market corrections potentially presenting opportunities for investors.

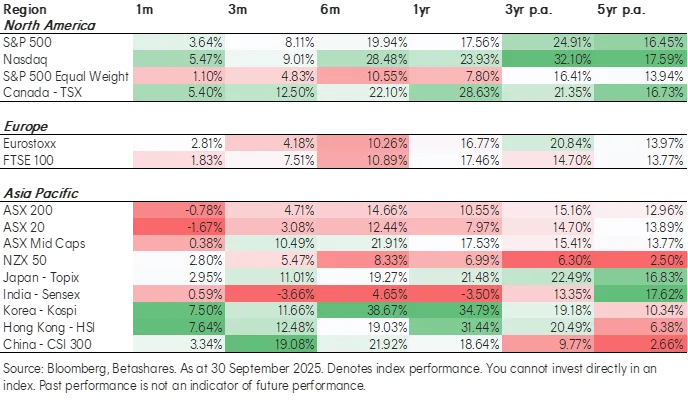

Equity market dashboards

Betashares Capital Limited (ACN 139 566 868 / AFS Licence 341181) (“Betashares”) is the issuer of this information. It is general in nature, does not take into account the particular circumstances of any investor, and is not a recommendation or offer to make any investment or to adopt any particular investment strategy. Future results are impossible to predict. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in any opinions, projections, assumptions or other forward-looking statements. Opinions and other forward-looking statements are subject to change without notice. Investing involves risk.

To the extent permitted by law Betashares accepts no liability for any errors or omissions or loss from reliance on the information herein.

Sources:

1. Source: Bloomberg. ↑

2. Source: Nasdaq Global Indexes, FactSet. As of 25 August 2025. ↑

3. Source: U.S. Bureau of Economic Analysis. 25 September 2025. ↑

4. Source: FactSet data. As at 1 September 2025. ↑

5. Source: FactSet data. As at 1 September 2025. ↑

6. Source: Bloomberg. As at 1 October 2025. Mid caps represented by the Solactive Australia ex 20 Index. You cannot invest directly in an index. Past performance is not an indicator of future performance. ↑

7. Source: Bloomberg. As at 1 October 2025. Asian technology represented by the Solactive Asia Ex-Japan Technology & Internet Tigers Index. You cannot invest directly in an index. Past performance is not an indicator of future performance. ↑

8. Source: Bloomberg. September 23 to September 30. Past performance is not an indicator of future performance. ↑

9. Source: Bloomberg. Forward P/E ratio as at 1 September 2025. ↑

10. Source: Bloomberg. Asian Technology Companies represented by the Solactive Asia Ex-Japan Technology & Internet Tigers Index. Past performance is not an indicator of future performance. ↑

11. Source: World Gold Council. Gold Demand Trends: Q2 2025. ↑