David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

Global week in review: Iran hopes wax and wane

Global stocks, on balance, rose last week, helped by US President Donald Trump’s earlier suggestion that Iranian hostilities would end soon and that other countries would be left to try and open the Strait of Hormuz.

That hope, sadly, did not last.

Later in the week, Trump threatened in a national address to “bring them back to the Stone Ages” if it did not open the Strait. He followed that up with yet another 48 hour ultimatum to agree to a deal, or the US would begin to target key infrastructure such as bridges and electricity plants. Trump is playing both good and bad cop, often within the same speech!

So far at least, Iran has not budged – perhaps once again aiming to test Trump’s resolve. The deadline expires at 8pm tonight New York time (10am tomorrow morning Sydney time). The clock is ticking once again.

The frustrating aspect of all this is that I suspect Iran would reopen the Strait once the US declared victory and stopped the attacks. Closing the Strait was only ever a means of putting political pressure on Trump by jacking up global oil prices – once the US threat ends, so does the need to apply this pressure. If Iran agreed to open the Strait in exchange for the US ending hostilities, would that be enough for Trump? Maybe, maybe not. Either way, neither side so far wants to be seen as the one caving in.

Of course, there’s a chance that, in the next 24 hours, Trump could announce yet another reprieve, perhaps because of alleged signals from Iran that it (once again?) desperately wants to talk.

If not, and allowing for likely Iranian counter strikes, the world faces the grim prospect of widespread destruction of key Middle East energy, transport and, potentially, water infrastructure.

More serious damage to regional oil production facilities (which account for 40% of global oil exports) would mean supply constraints would last far longer, likely causing a further surge in oil prices and global recession. This is the fire Trump is playing with.

Given the Iran news, Friday’s stronger-than-expected US payrolls result was lost in the noise. The shame is that, were it not for the Iran drama, we’d be celebrating a remarkably resilient US economy – with a 186k bounce back in employment during March after a 129k slump in February, which was partly related to bad weather and strike activity.

The other notable development last week was outgoing US Fed Chair Jerome Powell noting that long-term inflation expectations remain well anchored, which led markets to scale back its (in my view, ill-founded) fear of a near term rate hike.

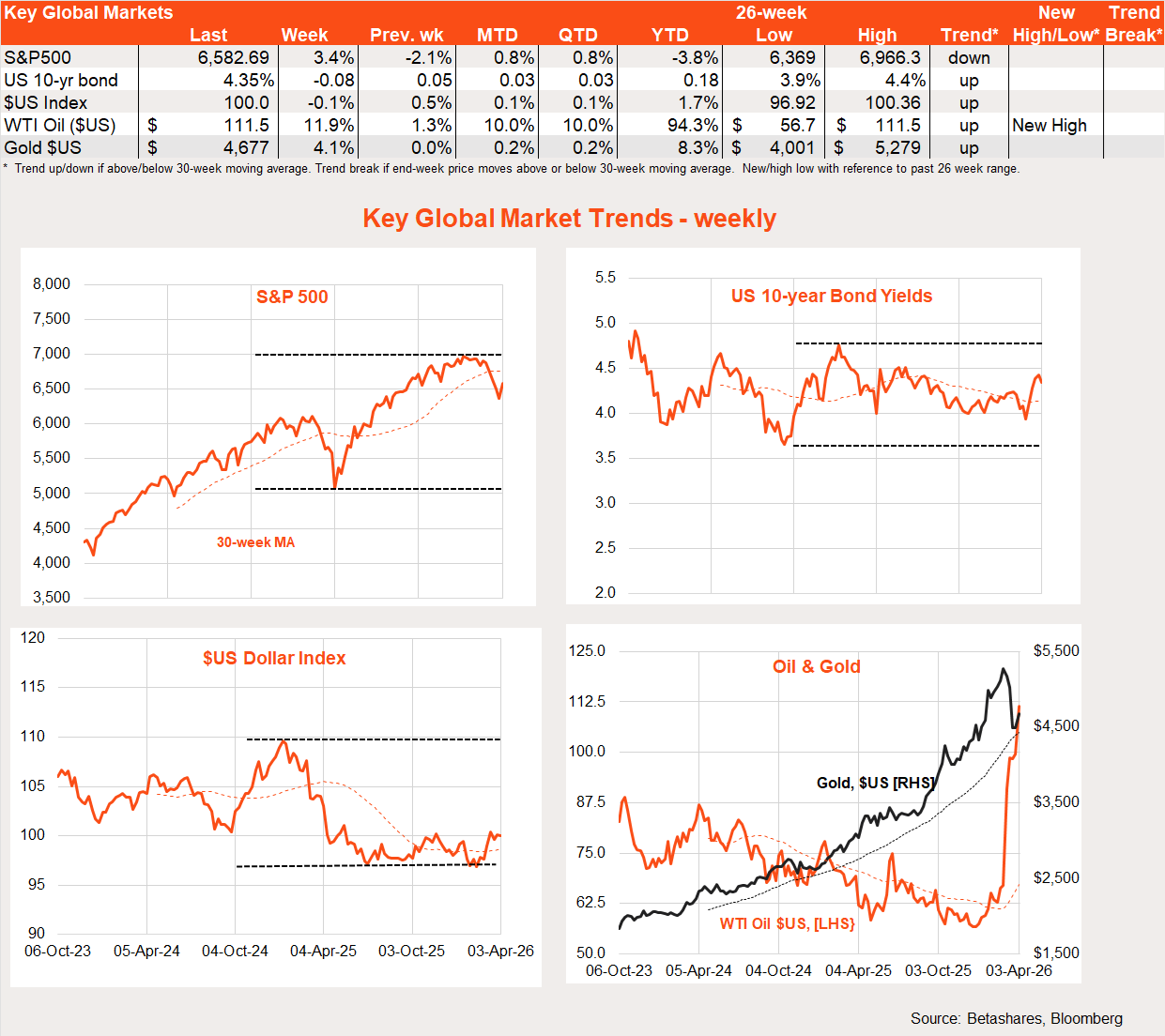

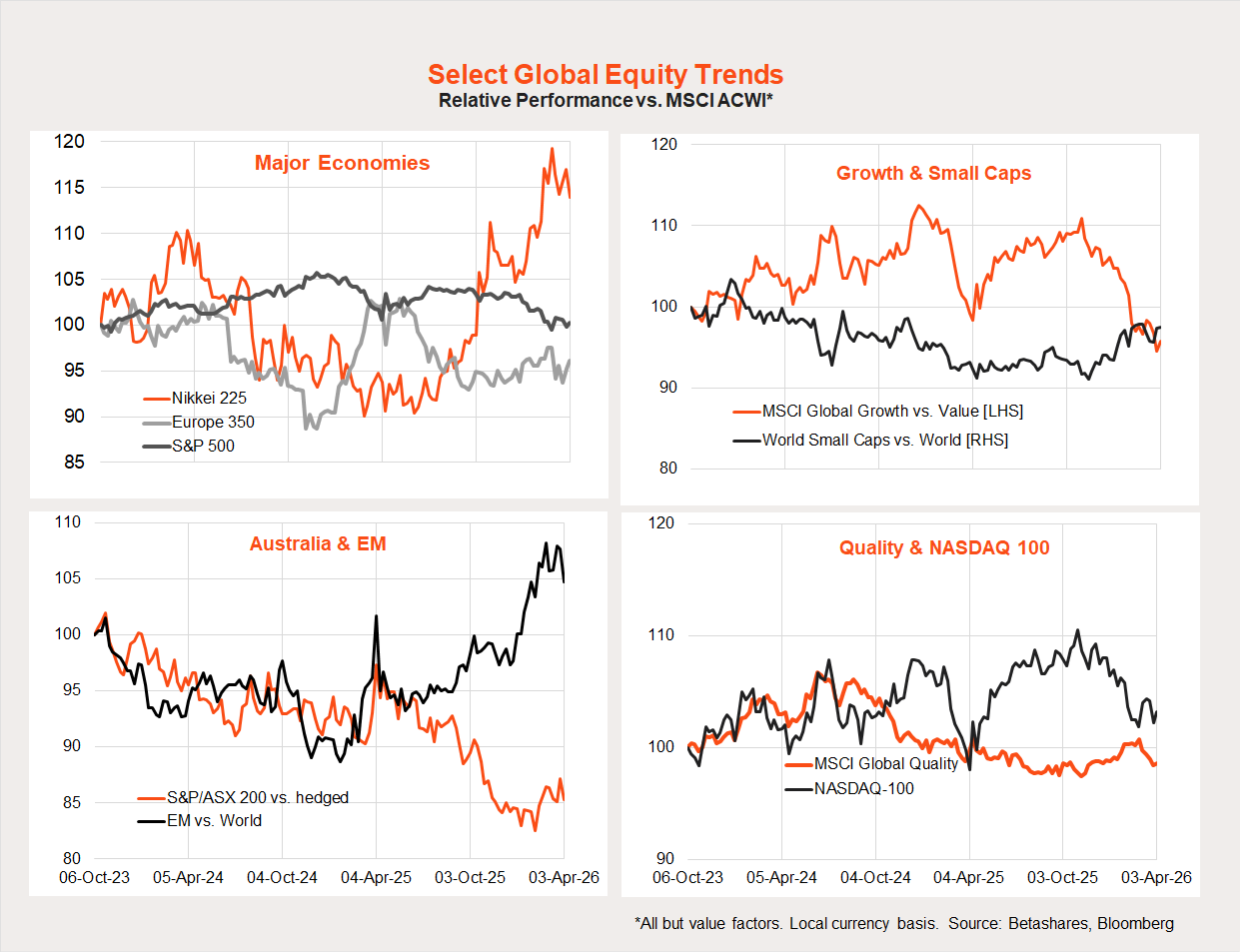

Global equity trends

Apart from the energy sector, there are few outright global winners from the war in Iran. Japan and emerging markets – the winning trades just prior to the war – have been hit hardest.

Global week ahead: Iran and US inflation

Iran will remain the centre of attention this week, with markets nervously awaiting Trump’s latest deadline – and the extent of Iranian retaliation should the US begin striking energy infrastructure.

Much like payrolls last week, ordinarily important US economic data – this time inflation – will not get much focus this week. That is also because the March and February readings for the CPI and PCED, respectively, will be treated as ‘old news’ given the energy cost spike now bearing down on the economy.

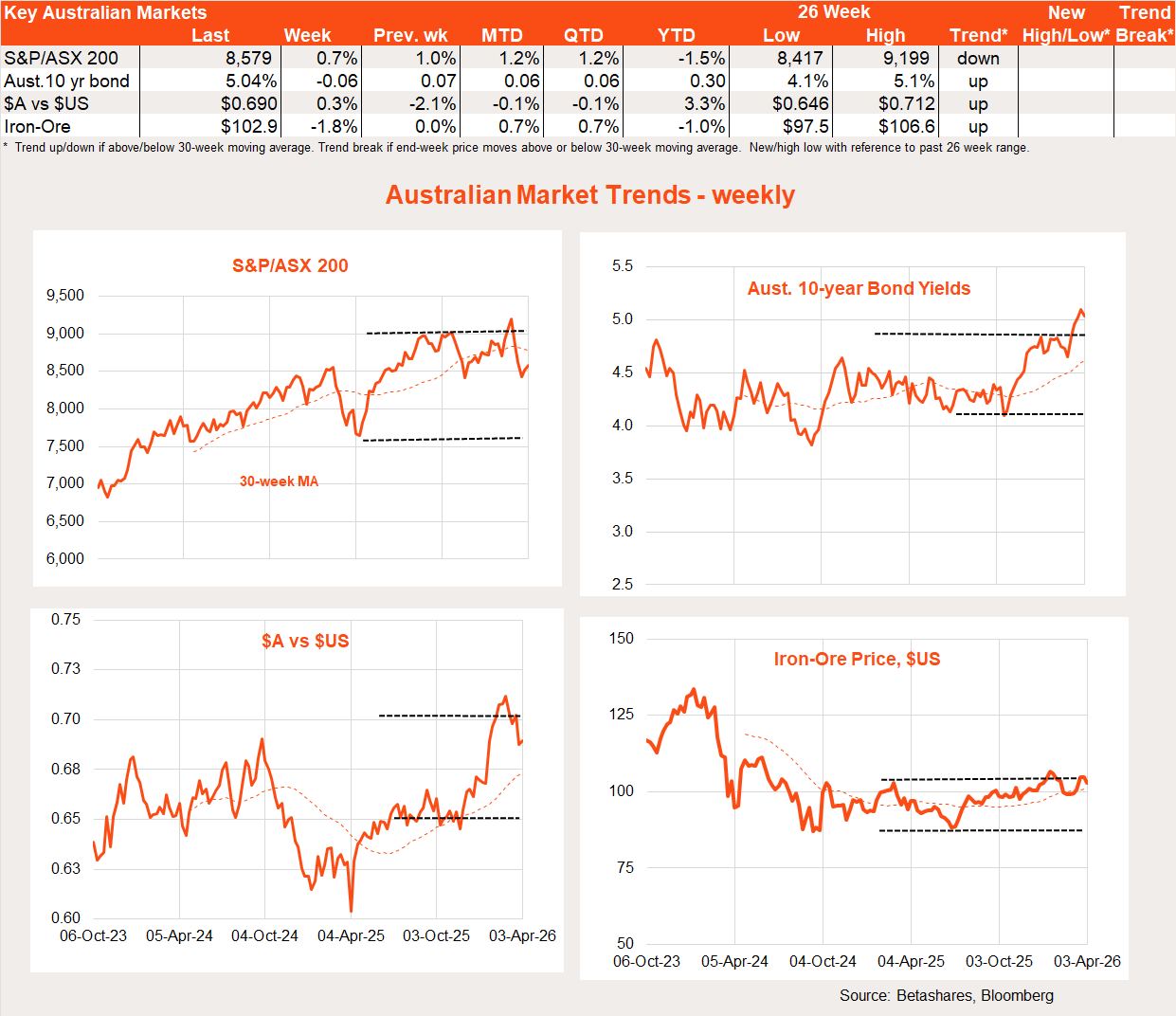

Australia in review: still-firm local data

Local shares also enjoyed a bounce last week on Iran hopes.

We received a smattering of local economic news last week – credit growth, house prices, building approvals and job vacancies. Much of these remained firm.

Although house prices continued to edge lower in Sydney and Melbourne, this was offset by continued strength in the other, cheaper capital cities. Building approvals also bounced back strongly and, looking through monthly volatility, the trend remains upward. Although down from their post-COVID peak, job vacancies have stabilised over recent quarters at a still-high level.

All of this continues to suggest the local economy is reasonably resilient, which would allow the RBA to remain resolutely focused on upside inflation risks.

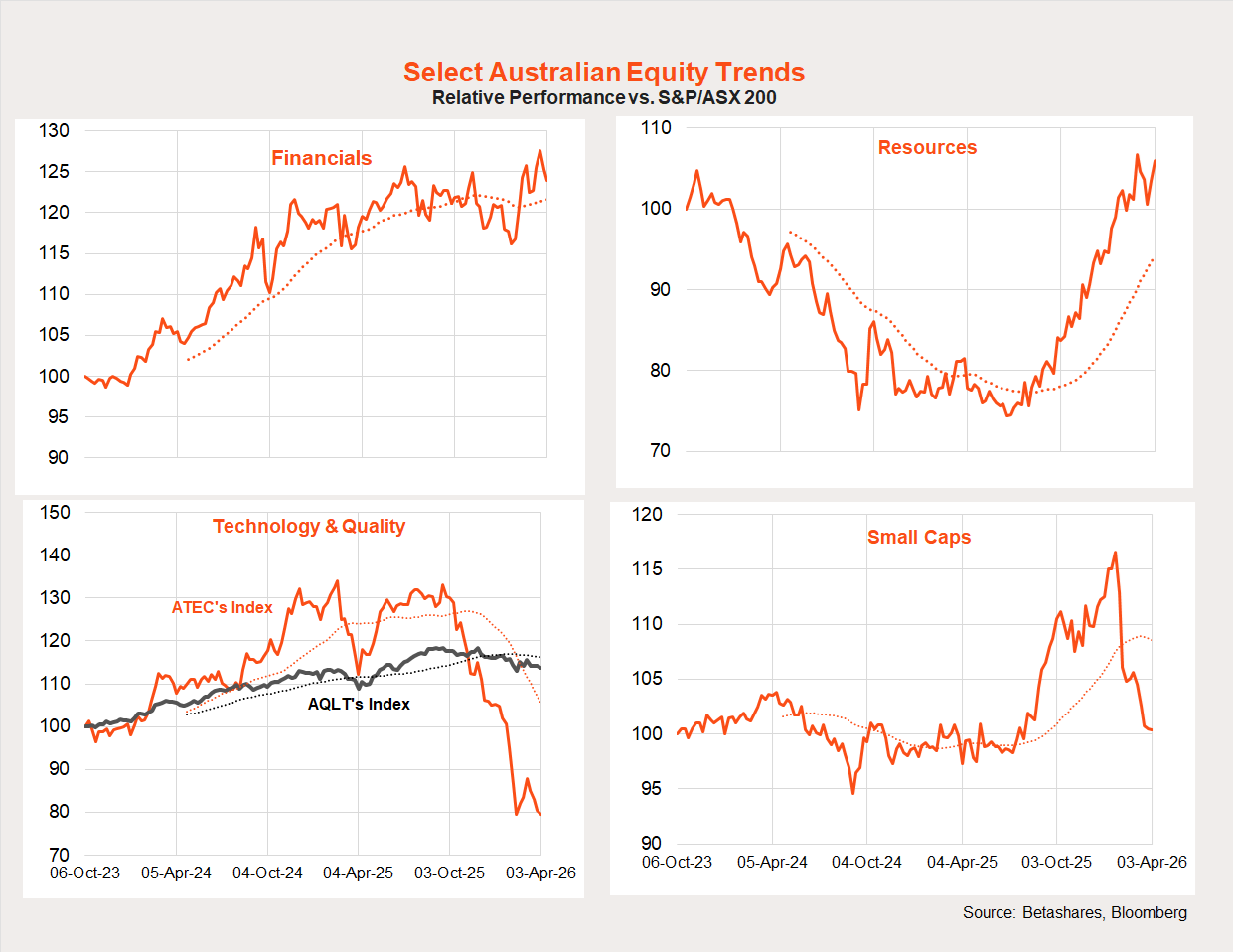

Local equity market trends

The Iran war has not been kind to high-beta local exposures such as technology and small caps. Relative performance of the larger cap resource and financial sectors has been choppy, but both have broadly held up.

Australia week ahead: household spending

The only local data of note this week is the newly established household spending indicator – which is broader in scope than the retail sales report it has replaced. Overall, spending is ticking along, albeit not especially strongly once inflation and population growth are allowed for.

Have a great week!