This information is for the use of financial advisers and other wholesale clients only. It must not be distributed to retail clients.

Key points

AQLT Australian Quality ETF extended its record to four consecutive years outperforming the S&P/ASX 200 – having outperformed every rebalance year since the Fund’s inception in April 20221 (AQLT rebalances on the 3rd Friday of June each year, giving a clean annual period to analyse the Fund’s performance. For simplicity, we will refer to this period as FY26 for the remainder of the blog).

In what was a tougher year for the quality factor, AQLT’s considered approach stood out amongst peers. The Fund outperformed the S&P/ASX 200 by 2.6%, taking average since inception outperformance to 3.9% p.a.

Like we have done in previous years, we wanted to take the opportunity to analyse AQLT’s performance between rebalances.

As a refresher, AQLT holds the largest companies listed on the ASX, but weighted by quality metrics rather than market capitalisation, meaning you get higher exposure to names like Telstra and Wesfarmers, lower exposure to CBA, and higher exposure to high-quality names from the mid and small caps, including Smartgroup, Data#3 and Breville.3

AQLT stands up in a tough year for quality

FY26 will go down as a tough year for quality factor investing in Australia.

The Australian FY25 corporate reporting season in August of 2025 saw many expensive growth-quality companies’ de-rate as results and guidance misses were punished by investors.

Software companies across sectors, which had become a feature of quality factor portfolios due to their low capital intensity, and strong and relatively stable earnings, suffered as AI disruption cast doubts over future returns.

Further, the RBA’s pivot from a cutting cycle to rate hikes impacted companies with higher valuations and more growth banked into future earnings. Both are typical features of high-quality companies.

As can be seen in the chart below, AQLT’s Australian active manager peers4 began suffering material drawdowns in August of 2025 during the Australian corporate reporting season with losses compounded during the year from the software sell off and RBA rate hikes. Promisingly, AQLT’s considered screening approach to quality investing in Australia held up a lot better, attributable to lower single stock concentration in names that suffered, picking local quality winners, and the portfolio’s large cap ballast.

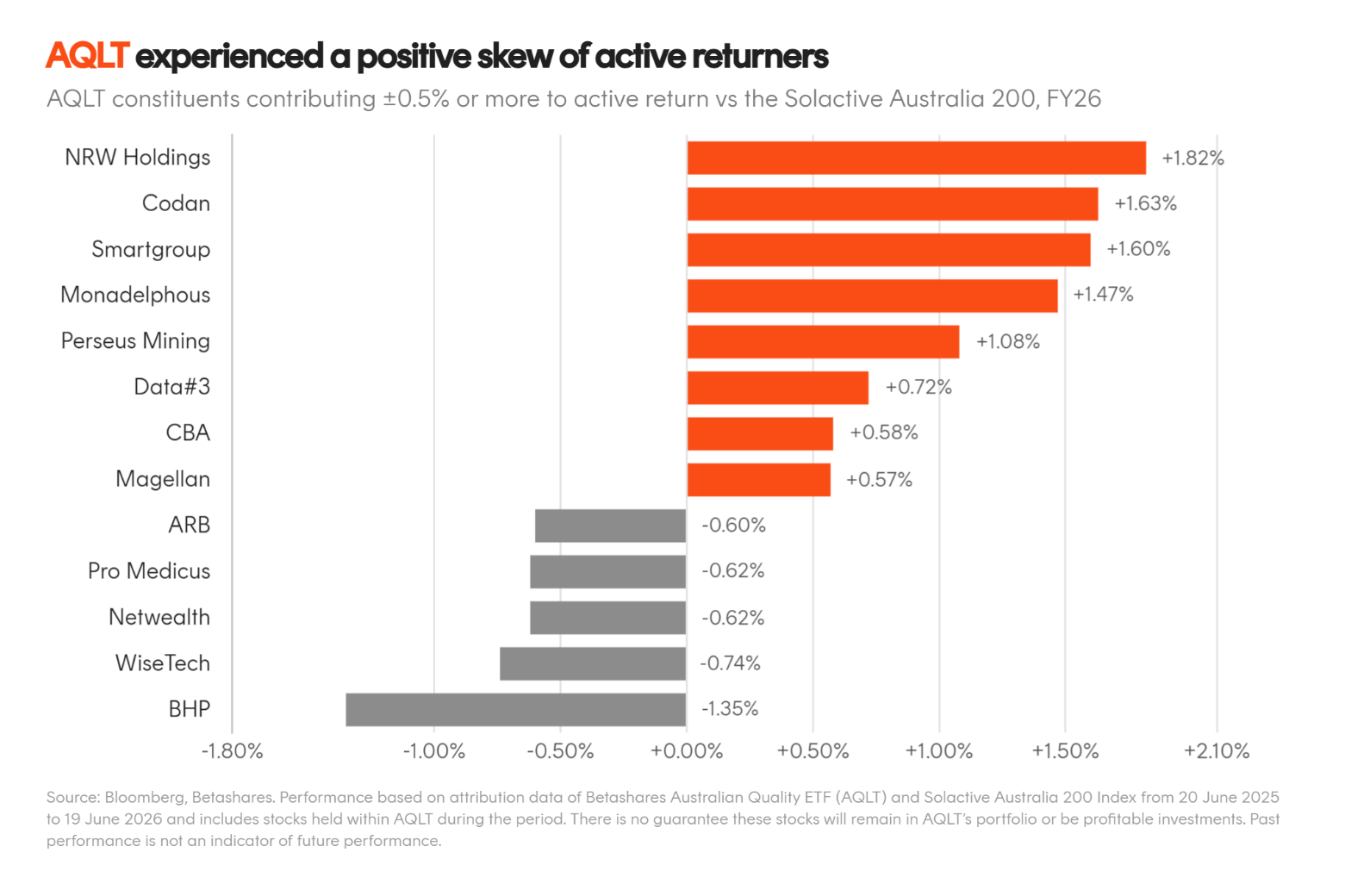

Familiar quality names dragged, but AQLT still skewed to the upside

A feature of AQLT’s relative outperformance since inception has been a meaningful positive skew of active returns from outperformers. Active return refers to the positive or negative contribution a selected security made relative to the comparable benchmark.

In FY26, high profile quality factor companies that AQLT was overweight in, like WiseTech, Netwealth and Pro Medicus suffered material drawdowns for the reasons outlined in the previous section. Cumulatively, the ‘losers’ that AQLT held contributed to 6.7% in active underperformance.5

AQLT’s ‘winners’ more than made up for those underperformers. The six largest contributors added 8.3% to active return6. The story this year behind AQLT’s top performers was split between high quality resource related companies that benefitted from the resource rally, a beneficiary of the AI rollout in Data#3, and Smartgroup’s policy windfall for the EV market.

By design, AQLT did not hold a lot of the more speculative mining companies that were some of the best performing companies on the S&P/ASX 200 as resources rallied. These exclusions cost AQLT versus the benchmark.

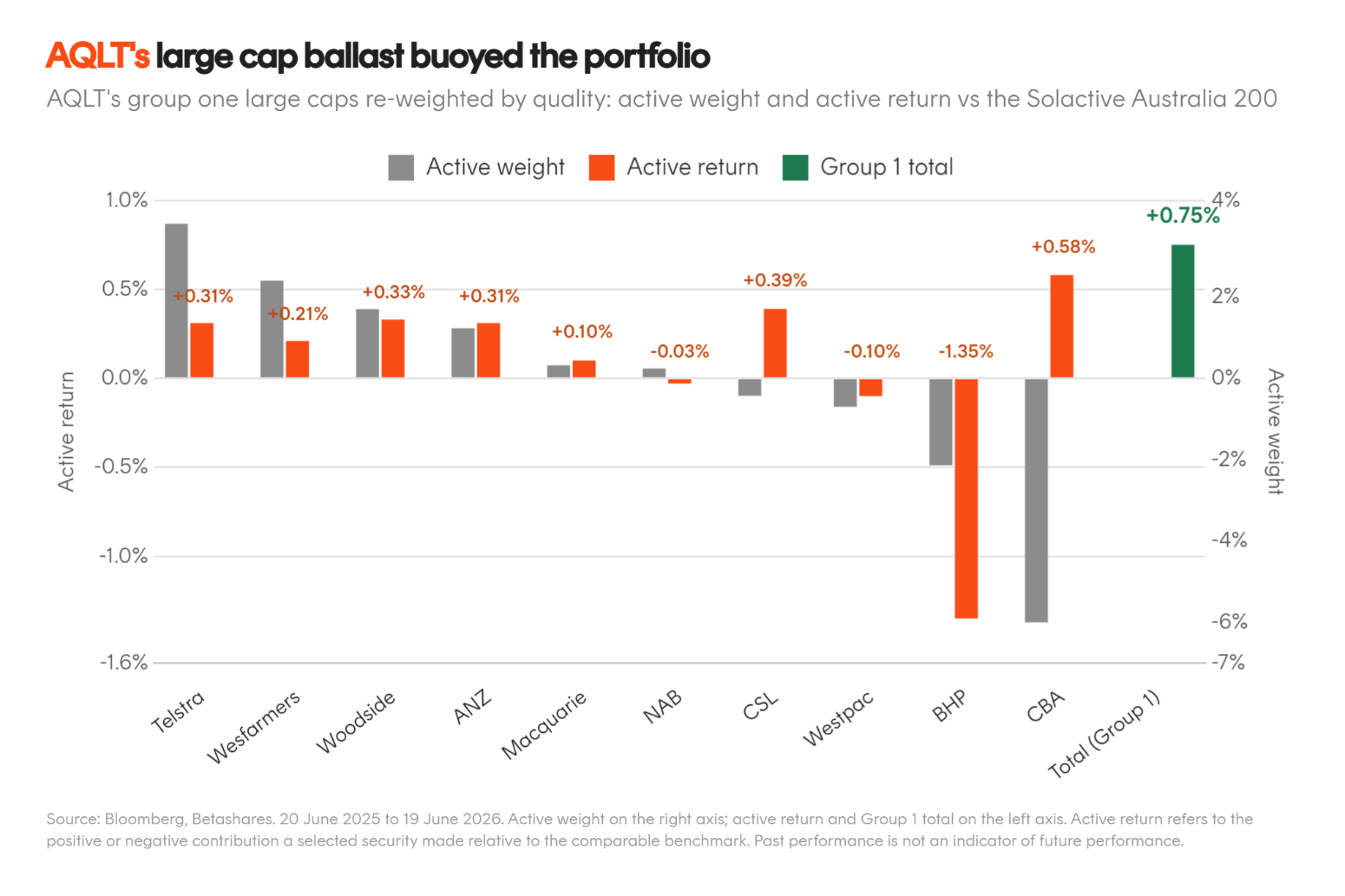

AQLT’s large cap ballast buoyed the portfolio

In constructing AQLT’s index we considered the fact that Australia’s market has inherently cyclical large caps and experiences periods of returns driven by these companies which are not considered high quality based on their fundamentals.

To overcome this challenge, AQLT still holds Australia’s largest companies, by market capitalisation, listed on the ASX and reweights them by their quality metrics. These include Australia’s ‘Big Four’ banks, along with cyclical resource companies like BHP and Woodside.

This year a majority of the large cap re-weightings led to positive active return. Notably, the underweight to CBA, which had historically been the portfolio’s biggest drag as the bank outperformed in prior years, led to a positive contribution following its decline.

BHP was the single biggest drag on the portfolio’s return this year. While BHP’s return on equity (ROE) and debt to equity rank favourably amongst the other large caps, the company’s stability of earnings, measured by AQLT as the five-year variation in ROE, is the poorest amongst the group. Given BHP’s significant weight in the benchmark index and its middle-of-the-pack composite score amongst the large caps, it received an underweight in AQLT’s portfolio, leading to 1.35% of underperformance. Not holding BHP at all would have cost AQLT around 6% versus the benchmark.7

Overall, the large cap re-positioning led to a positive contribution of 0.75%, providing a ballast for the portfolio against the S&P/ASX 200.8

Investment implications

In a tougher year for quality factor investment strategies in the Australian market, AQLT’s considered approach still provided meaningful outperformance versus the S&P/ASX 200.

AQLT’s success has seen it grow to over $1.3 billion in FUM since its inception in April 2022, up from $500 million this time last year, and perform in the top 5% of Australian Large Blend funds as defined by Morningstar.9

AQLT can be used in a diversified portfolio as a core Australian equities allocation.

Australian equities have been a challenging asset class for many investors over recent years given the changing large cap leadership, corporate earnings season volatility, and de-rating of many high quality and growth companies that featured heavily in favoured active manager portfolios and broad indices alike.

Given different factors tend to outperform and underperform during different phases of the market cycle, Betashares’ own Dynamic Managed Accounts use AQLT blended with an Australian value QOZ FTSE RAFI Australia 200 ETF and momentum MTUM Australian Momentum ETF with the aim of outperforming the broader market and improving risk adjusted returns through the cycle. For more information on Betashares approach to constructing a better Australian equities portfolio please read this insight.

For more information on AQLT, please visit AQLT Australian Quality ETF .