Southern route

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

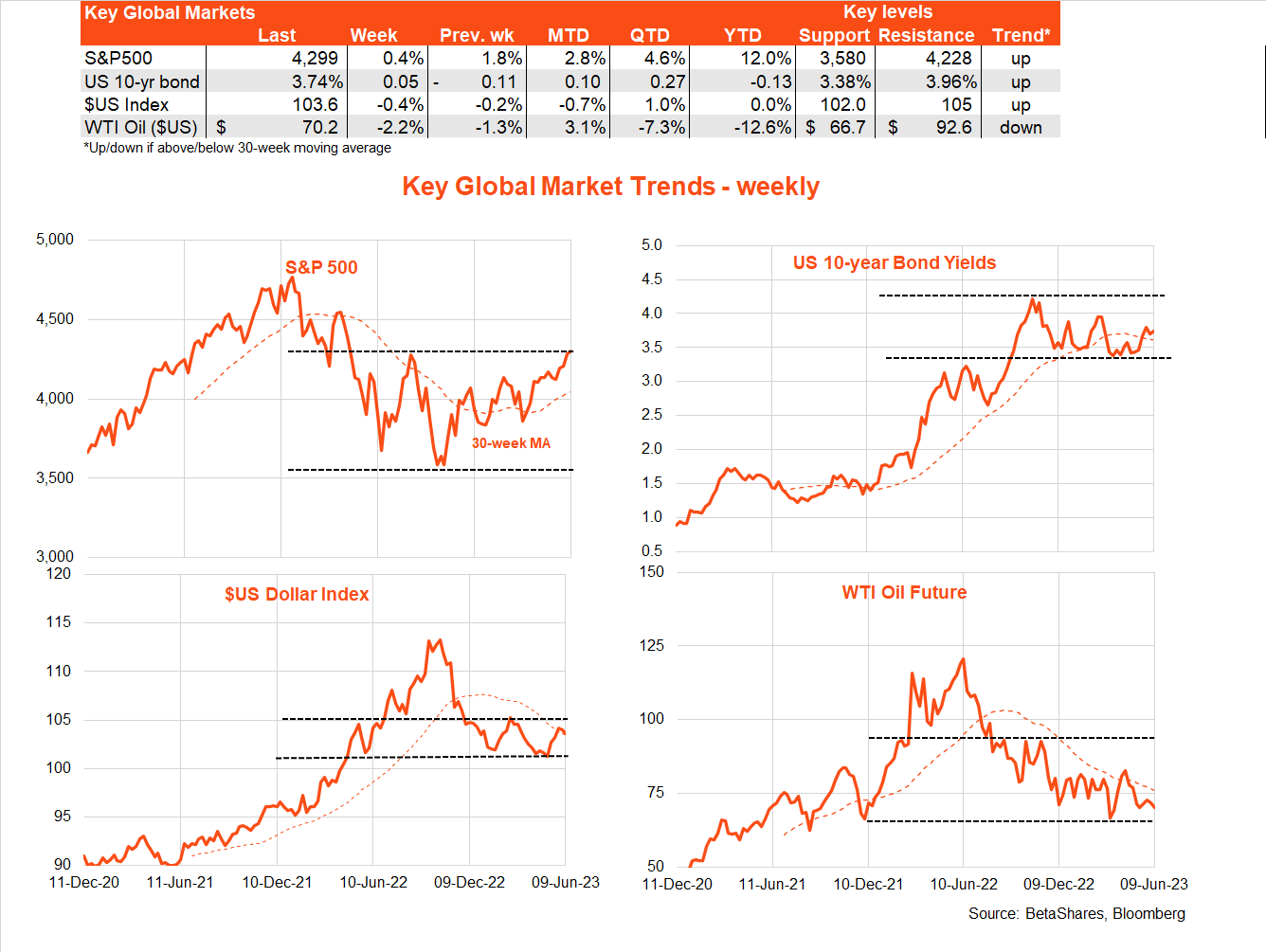

Global Markets

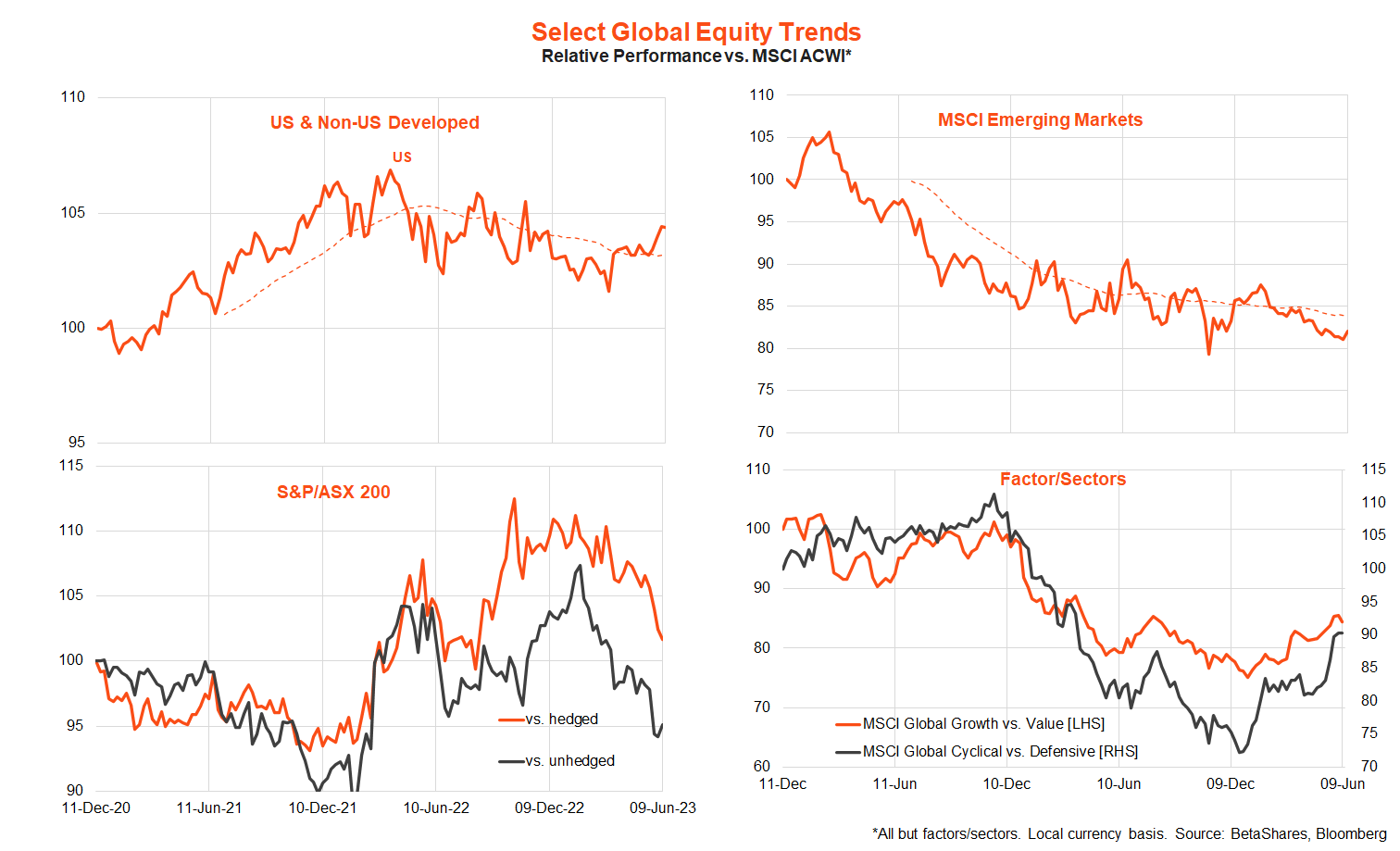

Global equities continued to grind ever higher last week, with some improvement in breadth as US small-cap stocks posted better performance than large-cap stocks.

Overall, equity markets took softer-than-expected US service sector data and a surprise rebound in weekly jobless claims as reasons to fear recession, but rather to be reassured that the Fed won’t jack up rates this week. According to market pricing, there’s an 80% chance the Fed will “skip” raising rates at Wednesday’s policy meeting, but a 75% chance it will hike by at least 0.25% p.a. in July.

That said, there’s still a lingering fear the Fed could surprise – after all, Australia and Canada both surprised with rate hikes last week after each found demand and inflation pressures had rebounded somewhat following an initial policy pause.

Also of note at this week’s Fed meeting will be an updated ‘dot plot’ of Fed rate hike expectations. The March projection had an end-23 Fed Funds projection of 5.1% p.a. (where it is at present), so the Fed would effectively signal it’s likely done raising rates unless it is lifted. As I don’t think it wants to convey this impression, it seems likely the end-23 level will be raised to 5.3% p.a. At the same time, the Fed will likely need to revise down its year-end unemployment forecast (from 4.5%) and revise up its core inflation forecast (from 3.6% p.a.).

Of course, other key US data will be retail sales and the CPI. Sales are expected to slip 0.1% after a solid 0.4% gain in April. The headline CPI is expected to rise only 0.2%, thanks to weaker energy prices, though core prices are expected to remain sticky with another 0.4% gain. That will see core annual CPI inflation ease to a still-high 5.3% p.a. from 5.5% p.a.

Elsewhere in the world, the European Central Bank is expected to hike rates another 0.25% p.a. on Thursday. That’s despite last week’s news that the EU slipped into a ‘technical recession’ after downward GDP revisions now suggest negative 0.1% growth in both the December and March quarters.

Data on Chinese industrial production, fixed-asset investment and retail sales are also released on Thursday, which are likely to confirm a slowing in the pace of economic recovery.

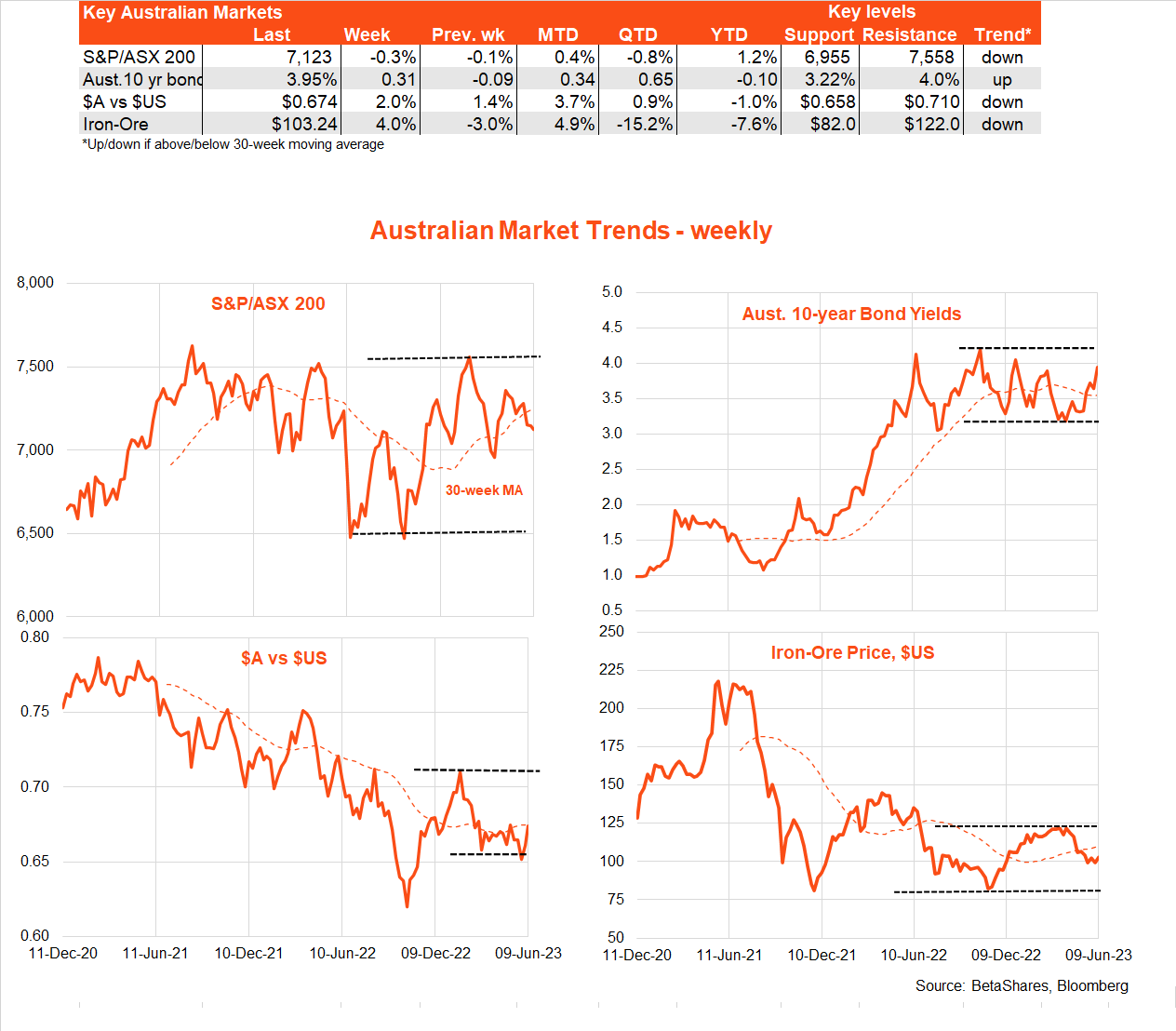

Australian Markets

Of course the major local highlight last week was the RBA’s surprise decision to hike rates for the second month in a row. Despite a clear softening in retail spending and employment demand, the RBA remains concerned with an apparent rising trend in labour costs as well as sticky service sector inflation.

My thinking is that the apparent tolerance of the Fair Work Commission and federal/state governments with solid gains in both minimum award wages and public sector pay was the ‘straw that broke the camel’s back’ in terms of RBA fears that an acquiescent inflation culture could be developing. The RBA wants to demonstrate it’s dead serious about bringing inflation down, even at the risk of a recession.

We learn more about just how vulnerable the economy is to a hard landing this week with an update on both consumer and business confidence from the Westpac and NAB surveys respectively. I suspect both will reveal significant declines in confidence.

Also of interest locally will be the May labour market report on Thursday. The market anticipates a modest 15k rebound in employment, after a surprise 4k fall in April, with the unemployment rate holding steady at 3.7%. Rising immigration makes it easier to keep employment growth ticking over, though what will be of interest in coming months is the extent to which labour demand is able to absorb this rising supply – and, if not, the extent to which unemployment lifts.

Have a great week!

Explore

Bassanese Bites