David Bassanese

6 minutes reading time

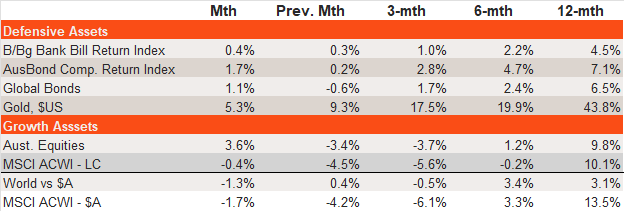

Major asset class performance

- Global equities fell modestly in April. An initial sharp sell-off due to President Trump’s ‘Liberation Day’ tariff announcements was largely offset by a sharp recovery on hopes that global trade deals would be announced and proposed US tariff levels reduced.

- Australian equities enjoyed a month of outperformance, reflecting relatively limited direct impact from US tariff increases and hopes of further local rate cuts due to a benign Q1 inflation report.

- A decline in bond yields, due to rising global growth concerns, led to modest gains in both global and Australian fixed-rate bond prices.

- Gold continued to perform strongly. The yellow metal is seen as a good ‘safe haven’ during volatile times and especially now given the downside risks to the US dollar.

Source: Bloomberg, Betashares. Cash: Bloomberg Australian Bank Bill Index; Australian Bonds: Bloomberg AusBond Composite Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged); Gold: Spot Gold Price in $US; Australian Equities: S&P/ASX 200 Index; Global Equities: MSCI All-Country World Index in local currency and $A currency (unhedged) terms. Past performance is not indicative of future performance.

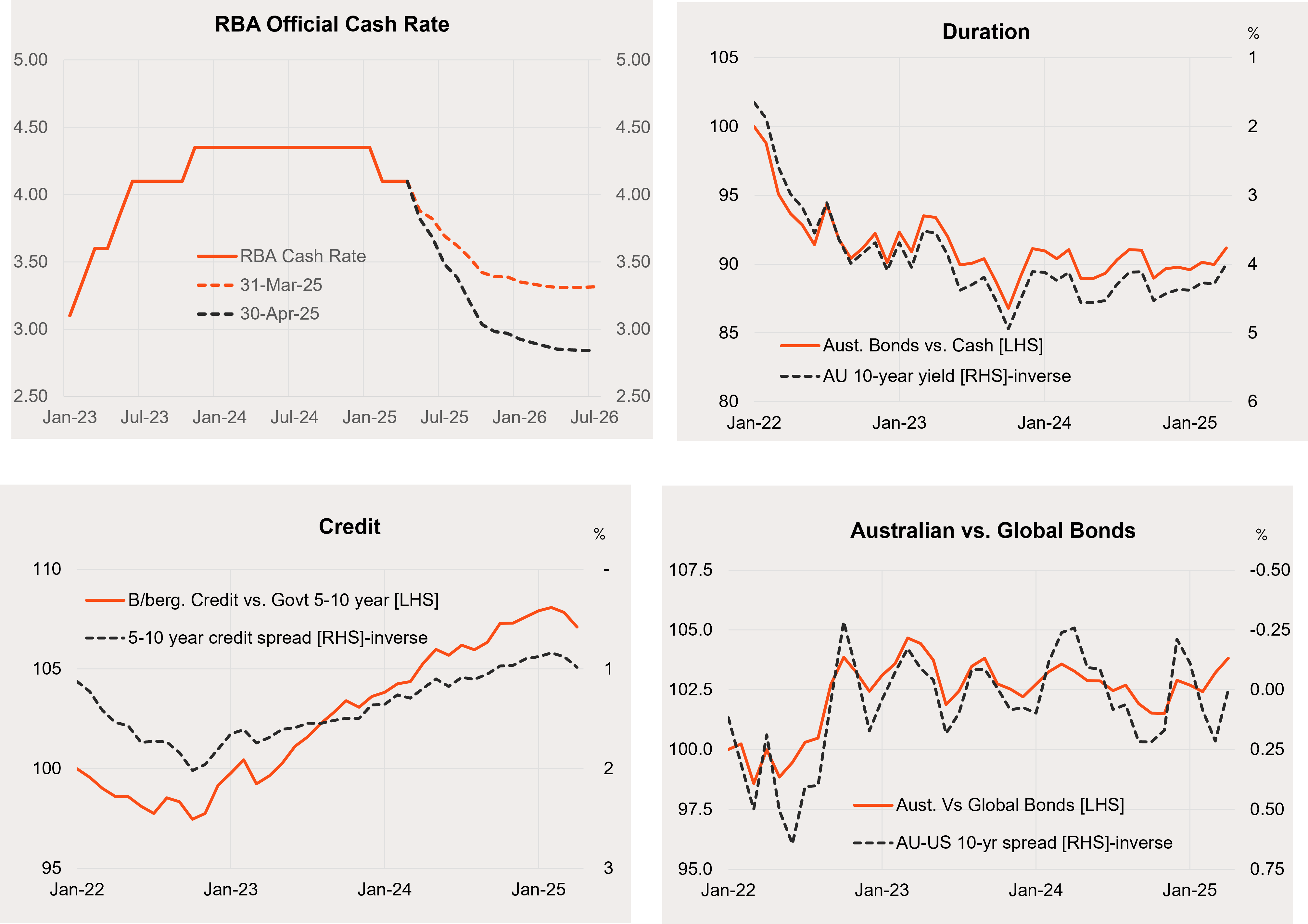

Fixed-rate bond trends

- Global growth concerns and benign inflation saw local rate cut expectations deepen over April. The market now expects the RBA to cut the cash rate from 4.1% to around 3% by year-end. In the US, rate cut expectations also deepened. The Fed funds rate is expected to drop to 3.2% from 4.3% by year-end.

- A general easing in bond yields since October last year has allowed local fixed rate bonds to modestly beat cash over this period. However, the longer-term trend since late 2022 has been choppy. The prospect of further rate cuts should support bond returns relative to cash over the coming year.

- Reflecting tariff concerns, local credit spreads widened in April. This partly unwinds a narrowing that has been evident since late 2022. Spreads remains vulnerable in the short-term due to further global tariff uncertainty.

- Local fixed-rate bonds have modestly outperformed global bonds in recent months. However, the relative performance since late 2022 has been more choppy. The outlook for local versus global bonds remains relatively neutral.

Source: Bloomberg, Betashares. Australian bonds: Bloomberg AusBond Composite Bond Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged).

Global equity trends

- The MSCI All-World Price Index declined by 0.5% in April. A modest uptick in the price-to-forward-earnings (P/E) ratio was more than offset by a decline in forward earnings.

- Both rising valuations and forward earnings have helped support global equity returns since late 2023. Given bond yields have been in a choppy sideways range over this period, the rise in valuations signals a declining equity-risk premium.

- Although earnings growth expectations remain robust, a decline in the expected level of earnings for both this year and next year has been evident in recent months. Recent US tariff concerns aggravating the concerns in April.

- With valuations still somewhat elevated, continued market gains will be reliant on falling bond yields and/or continued resilience in the corporate earnings outlook.

Source: Bloomberg, LSEG, Betashares. Global Equities: MSCI All-Country World Index. Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged). You cannot invest directly in an index. Past performance is not an indicator of future performance.

-

Among select Betashares global equity ETFs, financials (BNKS), gold miners (MNRS), and healthcare (DRUG) have performed relatively well so far this year. This reflects the strength in gold prices and a broader rotation toward value stocks over growth.

- Having said this, there was a modest correction in these trends in April.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the MSCI All-Country World Index (local currency terms) for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Australian dollar

- The Australian dollar strengthened further in April from US62.5c to US64.0c, in spite of global growth concerns.

- With iron ore prices and relative interest rates reasonably steady, the Australian dollar’s strength largely reflected US dollar weakness.

- Although normally considered a safe haven in times of global market stress, the US dollar has been undermined of late by US-centric concerns. Should tariff concerns escalate, there may be more US dollar weakness and Australian dollar strength down the line.

- Bigger picture, the US dollar remains expensive based on long-run valuation metrics. This should favour a firmer Australian dollar over time.

Australian shares

- Australian equities enjoyed a rare burst of outperformance in April, with the S&P/ASX 200 index returning 3.6%.

- The lift more so reflected a bounce in prices rather than further downward pressure on forward earnings.

- Relatively high valuations leave the local market vulnerable without a decent decline in bond yields. Expected 12-month growth in forward earnings of 8% is modestly less than the 12% expected globally. However, local earnings expectations remain in a broad downward trend.

Source: Bloomberg, LSEG, Betashares. Australian Equities: S&P/ASX 200 Index. Australian Bonds: Bloomberg AusBond Composite Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

- Among select Betashares Australian equity ETFs, financials (QFN) have generally held up better so far this year, while technology (ATEC) has tracked lower in line with our global peers. Performance among the other ETFs has been relatively even.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the S&P/ASX 200 Index for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.