Hugh Lam

4 minutes reading time

The health of US corporate earnings has never been more important this year.

Exuberance around AI continues to drive markets to record highs with new deals between megacap tech companies dominating headlines in recent months. While there are concerns around the “circularity” occurring in AI deals and whether an AI bubble is forming beneath us, ultimately the current bull market will need to rely on earnings doing the heavy lifting for its run to continue.

And with an ongoing US government shutdown set to delay jobs report data this week, investors will remain laser focused this earnings season for guidance to the overall direction of US stocks from here.

How is corporate America performing three weeks into earnings season?

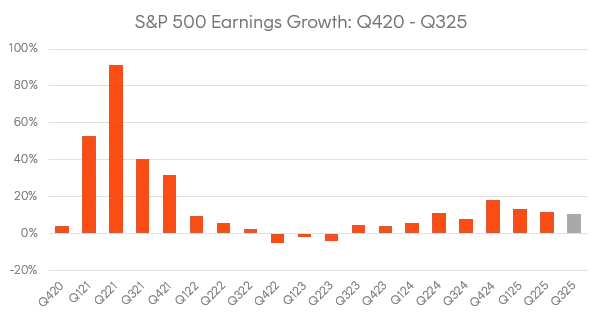

More than half of S&P 500 companies have now reported earnings for the third quarter and overall, the results appear strong. The blended (year-over-year) earnings growth rate for the S&P 500 is estimated to be 10.7%, which marks the 4th consecutive quarter of double-digit earnings growth for the index according to estimates from FactSet.

Source: FactSet. As at 31 October 2025.

Much of that growth has been driven by the Financials and Information Technology sectors.

Positive EPS surprises by Morgan Stanley, Capital One, Bank of America, and JPMorgan Chase were driven by strong dealmaking activity, investment banking fee revenue, and stock trading income. Across their transcripts, consumer spending remains solid with credit quality holding up despite the higher rate environment, however there was more restrained spending among lower income households.

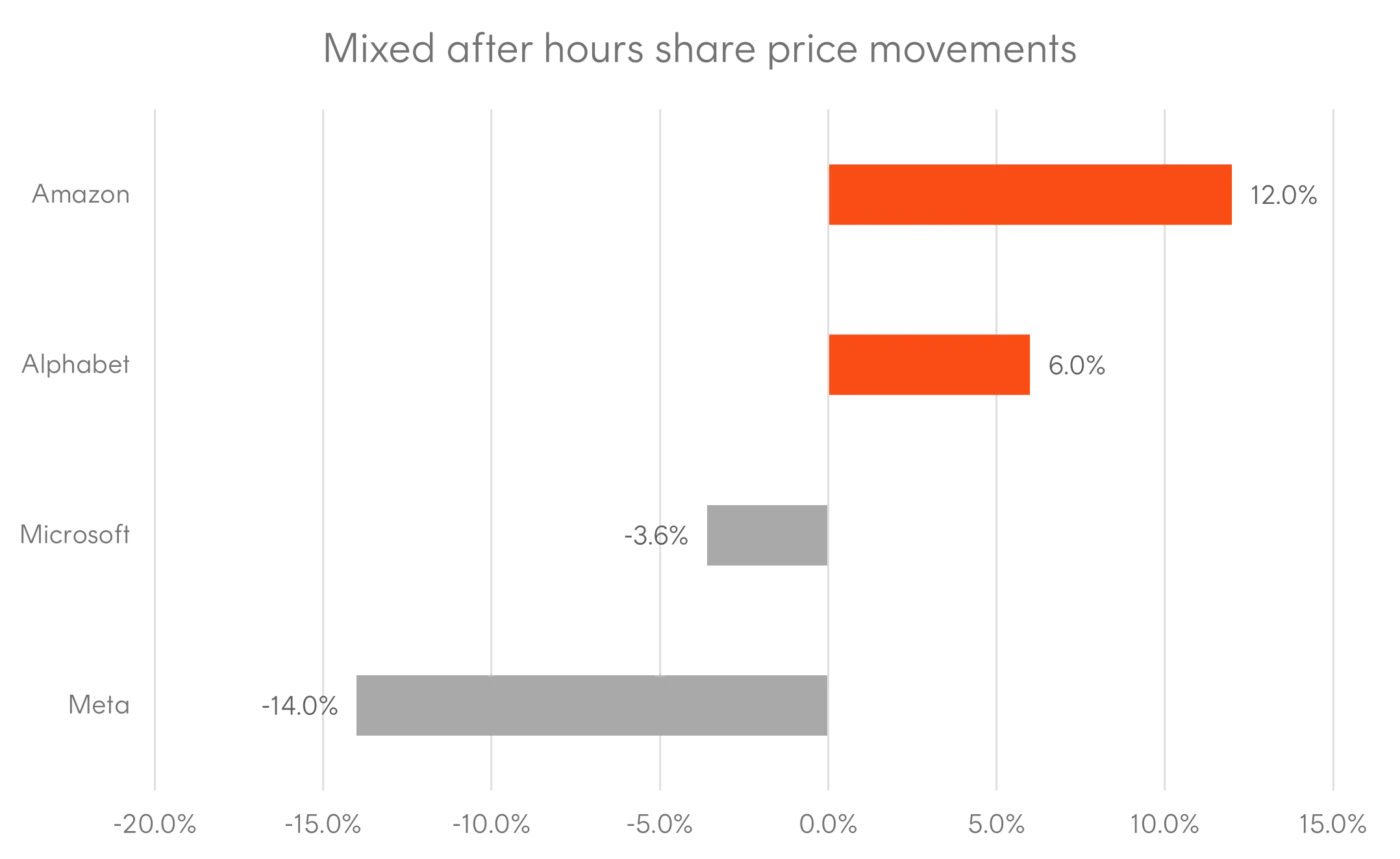

In technology, we saw five of the Magnificent 7 companies reporting last week. Overall, their results showed that the capex juggernaut is showing no signs of slowing but this time around, markets are becoming more discerning on whether these investments are translating into profits – best reflected in the mixed share price reactions of these companies.

Meta and Microsoft both slid on concerns over surging AI capital expenses. And while Alphabet also raised its 2026 capex forecast, its shares rose as investors were more accepting of its AI monetisation capabilities with its cloud platform (GCP) growing revenues by 34%. GCP is widely viewed as Alphabet’s strongest source of growth and an indicator of how the AI boom is contributing to the company’s sales. Similarly, Amazon’s 12% share price rise was driven by its cloud services unit (AWS) which grew revenues by 20% over the year, its fastest pace of growth since ChatGPT was released. The unit generated US$11.4 billion in operating income at a high 35% margin rate.

Source: Bloomberg. Data as at each company’s respective earnings release date.

Despite the mixed movements, the S&P 500 index ended October up 2.3% for the month, marking its sixth straight month of gains. With momentum on its side, we turn to some key themes worth watching from here.

What to watch from here

This week, we have another busy batch of earnings with more than 130 index companies reporting.

In tech, Qualcomm will be reporting earnings tomorrow morning (AEDT) where investors will be assessing how well its AI chips are being adopted as it looks to diversify away from the smartphone market; and earlier this morning, AMD had a strong result raising Q425 revenue guidance to US$9.6 billion +/- $300 million which would reflect a 25% year-over-year growth rate. As these companies aim to take a larger share of the AI accelerator chip market, investors will be turning toward Nvidia’s earnings results when they report on November 19th after hours. Palantir also reported earlier this week with US$1.18 billion in revenue for the third quarter, however its share price fell almost 8% despite the beat due to concerns around the company’s lofty valuation. Palantir shares have more than doubled this year.

Beyond earnings, Wall Street will be looking towards any resolution to the ongoing US government shutdown which has injected another layer of uncertainty for investors as economic data will either be made absent or delayed. That, alongside the difficulty of balancing the Fed’s dual mandate led to two historical dissents last week – one from newly appointed Governor Stephen Miran who voted for a 50bps cut, while Kansas City Fed President, Jeff Schmid preferred no change.

Finally, the US Supreme Court will be deciding this Wednesday as to whether Trump had the legal authority to impose tariffs under the IEEPA (International Emergency Economic Powers Act). If not ruled in his favour, the decision could fundamentally reshape the Republican’s trade and economic policies which have defined much of 2025.