Tom Wickenden

7 minutes reading time

- Australian shares

- Technology

This information is for the use of licensed financial advisers and other wholesale clients only.

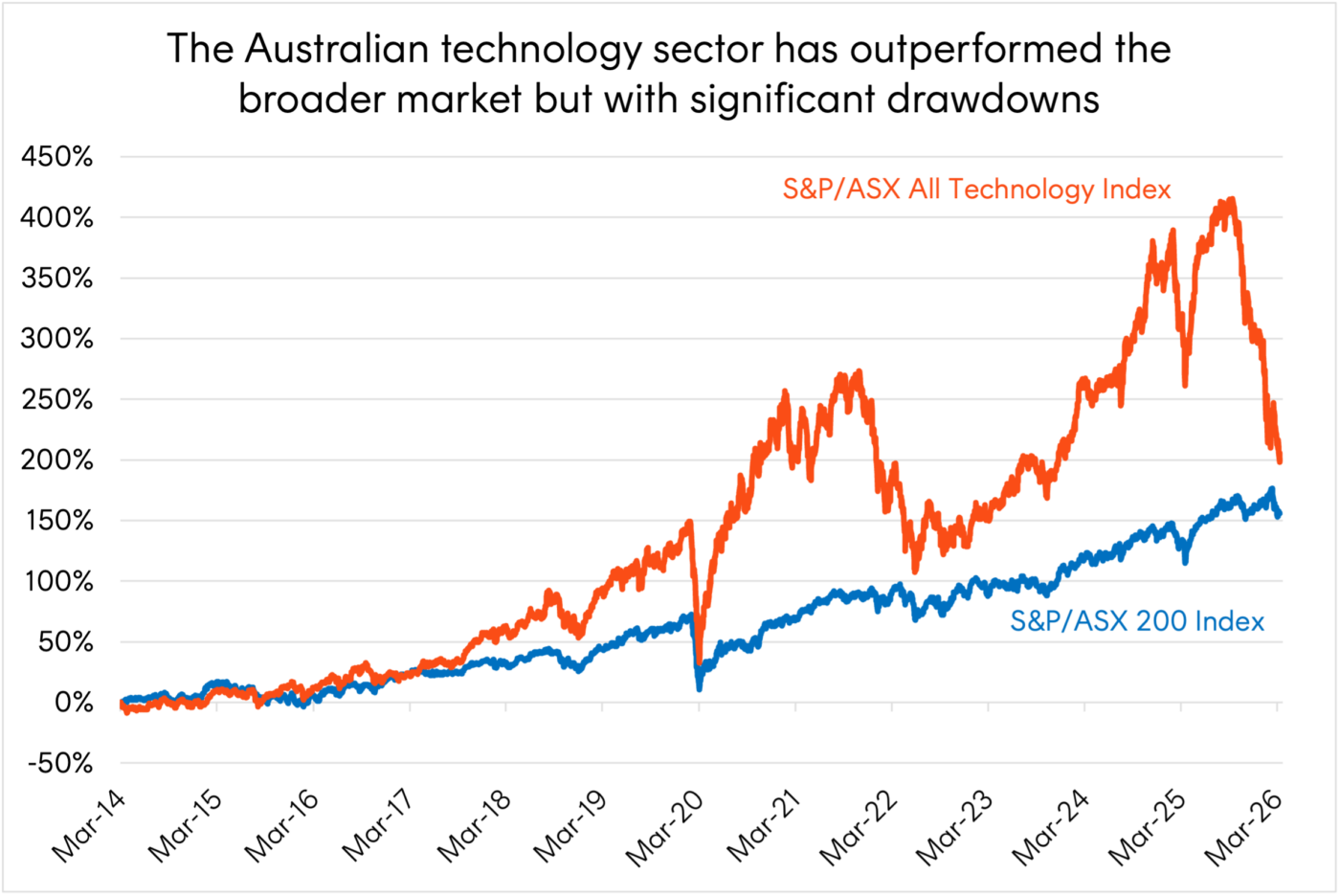

With just a 4% weight in the S&P/ASX 300 Index1 (ASX 300), Australia’s technology companies punch above their weight in terms of investor interest.

A small but dynamic part of Australia’s equity market, technology companies have experienced periods of significant outperformance against the broader Australian market and global technology peers while suffering material drawdowns along the way.

Since S&P’s launch of the S&P/ASX All Technology Index (the Index) in February of 2020, with data going back to 2014, we have had a true benchmark for Australia’s technology sector, enabling better analysis of both individual companies and the sector as a whole.

Source: Bloomberg. Since common inception 21 March 2014 to 31 March 2026. Chart is displaying total return indices. You cannot invest directly in an index. Past performance is not an indicator of future performance.

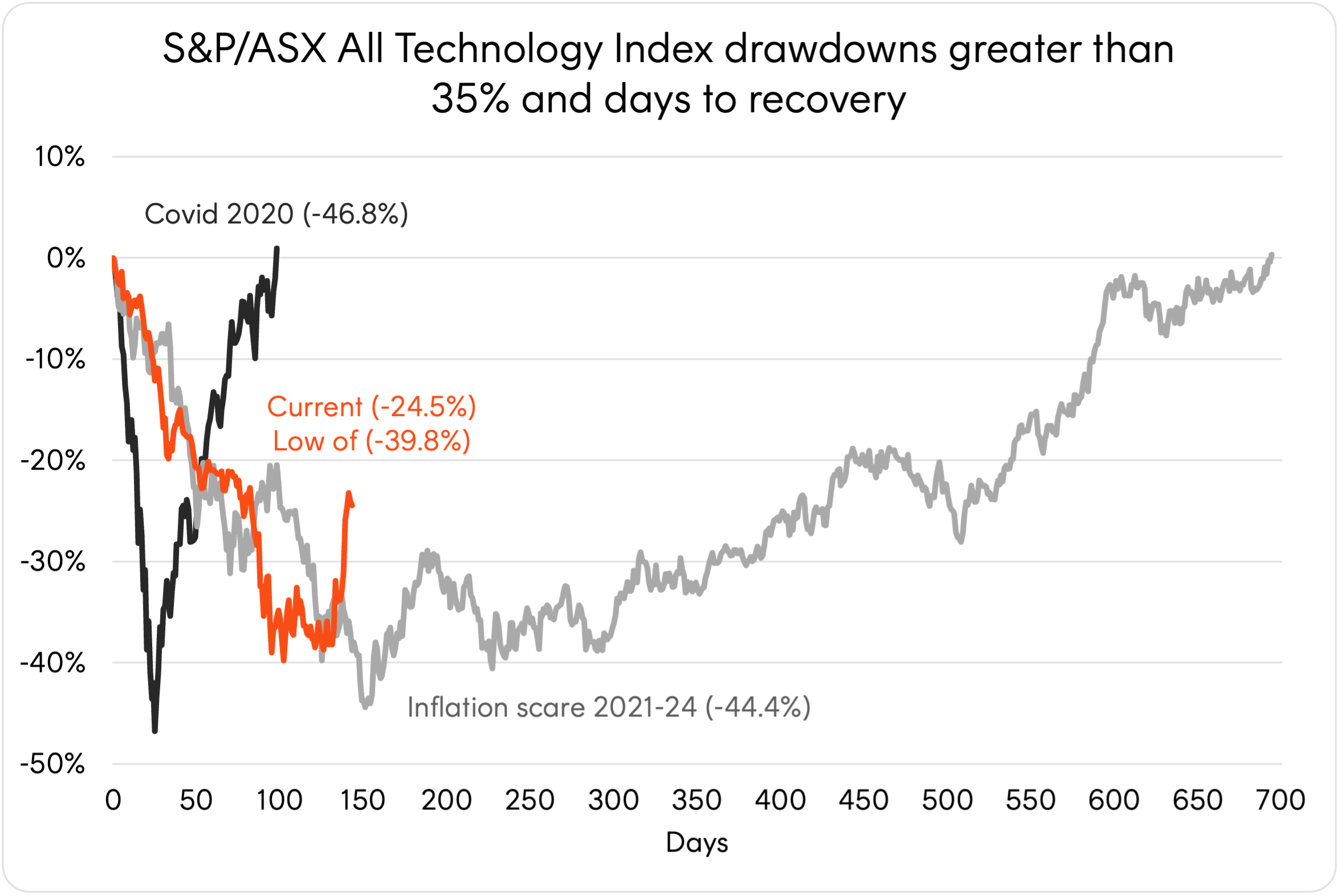

Having drawn down over 35% to the end of March, before rebounding 16% to mid-April2 on hopes of an Iran de-escalation and return to growth, we unpack the makeup of, and return drivers behind, the Australian technology sector and discuss the opportunities and risks ahead for investors.

Australian technology, no stranger to selloffs

While a drawdown of 35%+ might seem like a dramatic statistic for more ‘traditional’ sectors, it is not necessarily an anomaly for Australian technology.

Since the Index’ inception in 2014, the sector has experienced six drawdowns of 20% or more, with three drawdowns greater than 35% since 2020. The index has historically rebounded strongly in the years following these selloffs as market’s have returned to pro-growth cycles3.

Source: Bloomberg. Since index inception 21 March 2014. Covid drawdown: 18 February 2020 to 2 July 2020. Growth scare drawdown: 19 November 2021 to 17 July 2024. Current drawdown: 6 October 2025 to 22 April 2026 (not yet recovered) with a max drawdown of 39.8% on . You cannot invest directly in an index. Past performance is not an indicator of future performance.

Being a high beta sector, Australian technology has historically experienced larger drawdowns than the broader market during growth scares, such as the March 2020 selloff due to the Coronavirus outbreak.

Additionally, attracting high valuations due to typically strong earnings growth expectations and future upside potential, the Australian technology sector is also sensitive to interest rate expectations. For instance, markets pricing in higher future interest rates played a big role in both the 2022 selloff and the current drawdown4.

Both elements are at play in the sector’s current sell off. Geopolitical tension and technological disruption are threatening the pro-growth outlook while Australia’s persistent inflation and strong employment have driven the RBA to hike twice already in 2026.

There is, however, a factor unique to the current selloff. AI’s threat to software has made the Australian technology sector particularly vulnerable and seen its performance decouple from other regions, like the US’s Nasdaq 100.

The Australian technology universe

While traditional sector classifications like the Global Industry Classification Standard (GICS) identify the information technology (IT) sector, this does not guarantee that all technology companies in a market are captured within it.

In Australia for instance, Pro Medicus (ASX: PME) (a leading healthcare imaging software company) and Carsales.com (CAR) (a second-hand online car marketplace) are not classified in the IT sector, instead identified as healthcare and communication services companies respectively.

This is why S&P’s creation of the S&P/ASX All Technology Index was so important. The Index goes beyond the IT sector classification by including GICS sub-industries across sectors to capture the breadth of Australian technology companies, including:

- consumer electronics (consumer discretionary)

- health care technology (healthcare), and

- transaction and payment processing services (financials).

The result is a comprehensive portfolio of technology companies across Australia’s market. Of the Index’s 47 holdings, 31 appear in the ASX 300 yet collectively represent just 4% of that index5. The remaining 16 sit outside the 300 largest Australian companies entirely, meaning investors in broad market funds likely have little to no exposure to them.

Unpacking Australia’s technology sector

Examining the Australian technology sector’s composition helps to further explain the current selloff.

79% of the Index’s holdings are software companies, with just 17% classified as hardware. Of the software companies, 69% operate business to business (B2B) models6.

Compare this to the Nasdaq 100, with only 37% of current holdings classified as software companies and 42% hardware. The Nasdaq also has an almost even split of B2B versus business to consumer (B2C) models7.

|

S&P/ASX All Tech |

Nasdaq 100 |

|

|

Sub-Type |

||

|

Software |

79% |

37% |

|

Hardware |

17% |

42% |

|

Other |

3% |

21% |

|

Customer Type |

||

|

B2B (software) |

69% |

45% |

|

B2B (all holdings) |

76% |

56% |

|

B2C (all holdings) |

24% |

44% |

Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight.

Current concerns around AI disruption are being directed at B2B software companies as investors face uncertainty around their future profitability. The rapid advancement of AI capabilities is seen as a core threat to existing software moats that could be breached by cheaply created and implemented alternatives.

Additionally, B2B software companies relying on seat-count subscription models face the threat of job cuts reducing licence volumes across core business functions like finance (Xero Limited (ASX: XRO)) and HR/recruitment (SEEK Limited (ASX: SEK)). Hardware companies, as the picks and shovels of AI infrastructure, have largely been spared this pressure.

The result is a sector composition that has made Australian technology particularly vulnerable to the current sell-off.

Australian technology, stronger together

The honest caveat is that current investor uncertainty is not misplaced. Disruption risk is a permanent feature of technology investing. But disruption also presents opportunity, for incumbents to integrate and adapt and new entrants to grow. In a sector as dynamic and small as Australian technology, this points to the benefits of an indexed ETF approach.

Rather than concentrating risk in individual names, index ETFs can provide exposure to a broad basket of companies across a sector. As leading companies or new disruptors grow, their weight within an index increases naturally and investors gain greater exposure to emerging winners over time while reducing exposure to those that do not adapt.

In the short-term investors have already seen a rebound in Australia’s technology sector. A resolution to the Iran war, more certainty around AI disruption versus enablement, and Australia’s inflation coming under control allowing the RBA to cut rates once again are all short to medium term catalysts that could see the sector rebound strongly once again.

Long-term investors seeking diversified exposure to Australian technology may wish to consider the ATEC S&P/ASX Australian Technology ETF , which aims to track the S&P/ASX All Technology Index (before fees and expenses).

Disclaimer

Past performance is not indicative of future performance.

There are risks associated with an investment in ATEC, including market risk, technology sector risk and concentration risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk.

Any Betashares Fund that seeks to track the performance of a particular financial index is not sponsored, endorsed, issued, sold or promoted by the index provider. No index provider makes any representations in relation to the Betashares Funds or bears any liability in relation to the Betashares Funds.

No assurance is given that any of the companies in ATEC’s portfolio will remain in the portfolio or will be profitable investments.

Sources:

1. Source: Bloomberg. As at 16 March 2026. Weight of S&P/ASX All Technology Index constituents in the S&P/ASX 300. ↑

2. Source: Bloomberg. As at 22 April 2026. Drawdown period from 03 October 2025 to 30 March 2026, -42.2%. Past performance is not an indicator of future performance. You cannot invest directly in an index. ↑

3. Past performance is not an indicator of future performance. ↑

4. Source: Bloomberg, Betashares. Analysis of relationship between Australian 10-year government bond yields and S&P/ASX All Technology Index performance during historical episodes. Past performance is not an indicator of future performance. ↑

5. Source: Bloomberg. As at 16 March 2026. Weight of S&P/ASX All Technology Index constituents in the S&P/ASX 300. ↑

6. Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight. ↑

7. Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight. ↑