Hugh Lam

5 minutes reading time

Key takeaways:

- Adoption is moving from experimentation to production, with the steepest part of the S-curve still ahead.

- Anthropic hits US$30B annualised run-rate from $9B at the end of 2025, fuelled by rapid enterprise adoption.

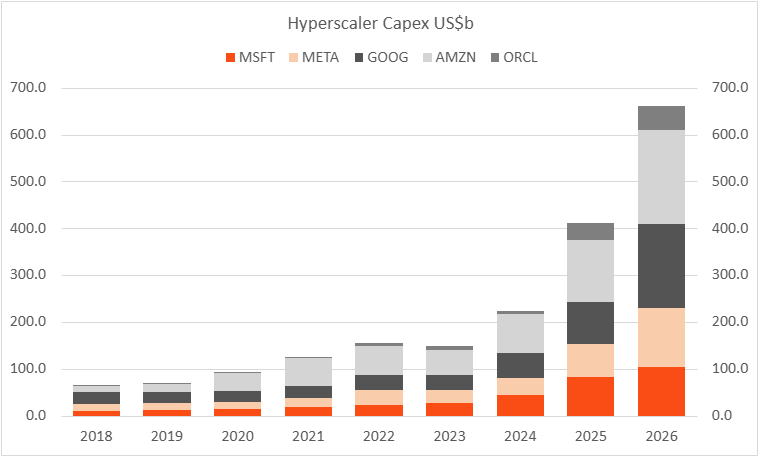

- Q1 2026 results from publicly listed hyperscalers reinforce the investment case for hardware and cloud providers building out next-gen compute capacity.

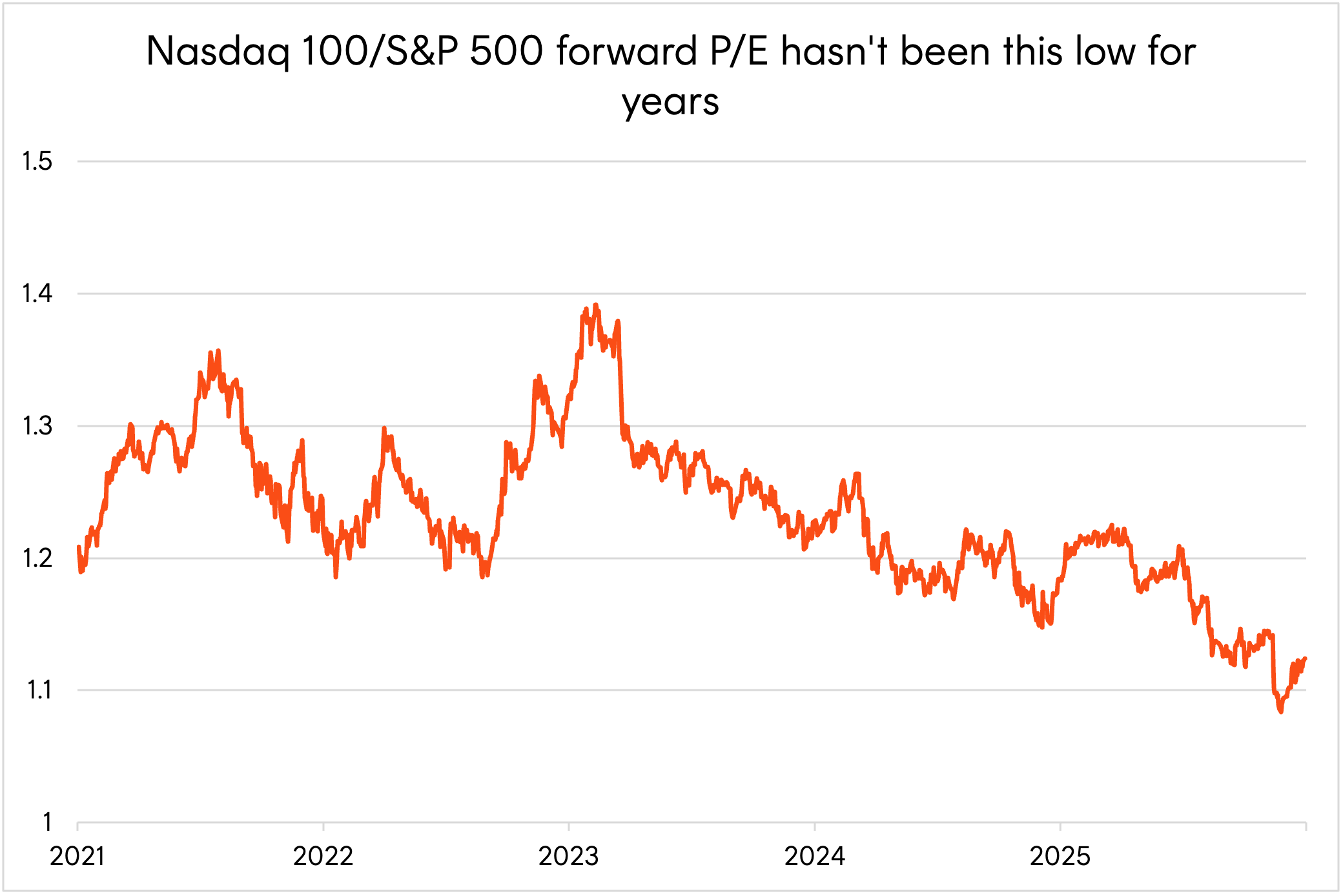

- The Nasdaq 100’s valuation premium relative to the S&P 500 is at multi-year lows, supported by strong earnings growth.

Not long ago, fears of an AI bubble dominated headlines throughout Q4 2025. Concerns around elevated valuations, rising debt issuance patterns and a massive amount of data centre capex spending saw the broader tech sector derate considerably.

Source: Bloomberg. 2026 figures are estimates.

But as we’ve highlighted in this article late last year, upfront investment outlays are often required before revenues scale exponentially; so the key question on investors’ minds was whether this would occur and if so, how long would it take before investor patience runs thin?

Fortunately, Q1 2026 results from the mega cap tech companies as a whole were enough to push US equity markets back to all-time highs despite the ongoing war in the Middle East.

- Alphabet was the standout performer despite capex guidance being raised to a range of US$185-$190 billion this year. The insatiable demand for compute has seen GCP (Google Cloud Platform) revenues soar by more than 60%, hitting US$20 billion for the quarter.

- While Microsoft’s results were also solid with Azure cloud revenue growing 40%, it is not experiencing the same reacceleration as its peers.

- Meta was another casualty with markets penalising its lack of cloud service offering but importantly have seen material ROI benefits with AI. The company experienced a rapid acceleration in top-line growth at higher EBITDA margins (~50%) while average prices per ad rose by 12% year-over-year.

- Amazon slipped as capex spending weighs on free cash flows despite AWS (Amazon Web Services) growing 28% yoy, marking the fastest growth rate in 15 quarters highlighting significant reacceleration, while its chip business (Trainium, Graviton) hit a $US20 billion annual run rate.

- Finally, Apple delivered better than expected results with iPhone sales up 22% while the CEO succession announcement of John Ternus is generally being looked upon favourably by markets given his more than two decades experience at Apple and demonstrable working experience with product/hardware design.

Beyond the overall robust results across these publicly listed megacap tech companies, we are also seeing positive developments with private model developers such as Anthropic, the creator of Claude.

Anthropic surpasses OpenAI in annualised revenue

Perhaps the best proof point happened last month when Anthropic announced it surpassed US$30 billion in annual run-rate revenue – up from just $9 billion at the end of 2025.

That’s more than triple in the space of just three months, with the rapid step change in growth driven by accelerating enterprise adoption with now over 1,000 businesses paying over $1 million annually for Anthropic’s latest models.

Source: Altimeter Capital Management estimates, Anthropic Press Release

To put into context how fast this achievement is, Google only crossed the $30B revenue threshold when it had ~110,000 people. Anthropic achieved this milestone with ~2,500 employees and just ~1.5-2 gigawatts of compute capacity. All else equal, that should bode well for improving unit economics and gross margins.

And with AI agents becoming a legitimate solution to solve real business problems, there will likely be more companies embedding Anthropic models into their workflows and customer facing apps via APIs. Usage is evidently shifting from experimentation phase to larger, production-level deployment.

The outlook for continued revenue acceleration remains bright given we have not yet reached the steepest part of the technology S-curve with enterprise AI penetration still in early stages.

The outlook for US tech

Anthropic’s result is a vote of confidence to the broader AI ecosystem and so far, validates megacap tech spending on data centre infrastructure.

Since March 31st, the blended earnings growth rate for the US Information Technology sector increased to 50%1, led by companies in the semiconductor industry.

Abroad, Samsung, a leading memory chip manufacturer, reported an eightfold jump in quarterly profit, while Taiwan Semiconductor posted a 58% profit jump.

Beyond strong fundamentals, valuations are attractive with the ratio of Nasdaq 100’s forward price-to-earnings ratio to S&P 500’s at multi-year lows. A large part of the decline in this ratio has been driven by the Nasdaq 100’s superior earnings growth over recent years.

Source: Bloomberg. As at 5 May 2026.

Additionally, the Nasdaq’s new fast entry rule would also allow massive IPOs, such as potential listings from Anthropic, OpenAI, and SpaceX, to join the index just 15 trading days after listing.

Looking forward, investors will remain attentive to how unit economics evolve, particularly for AI research labs like Anthropic given the scale of infrastructure investment required. That said, this is a positive development for leading hardware providers such as Google and Broadcom they are building the latest generation TPU chips, set to provide Anthropic around 3.5 gigawatts of compute capacity starting in 2027.

With the Nasdaq 100 trading at fairer valuations, and evidence of AI monetisation already before us, investors may find an attractive opportunity in tech now.

Source:

1. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_050126.pdf ↑