CPI to pressure rates

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Week in review

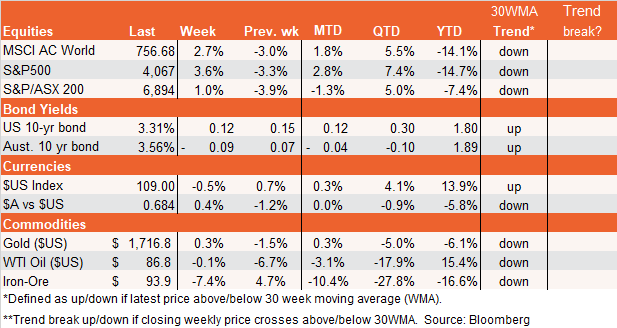

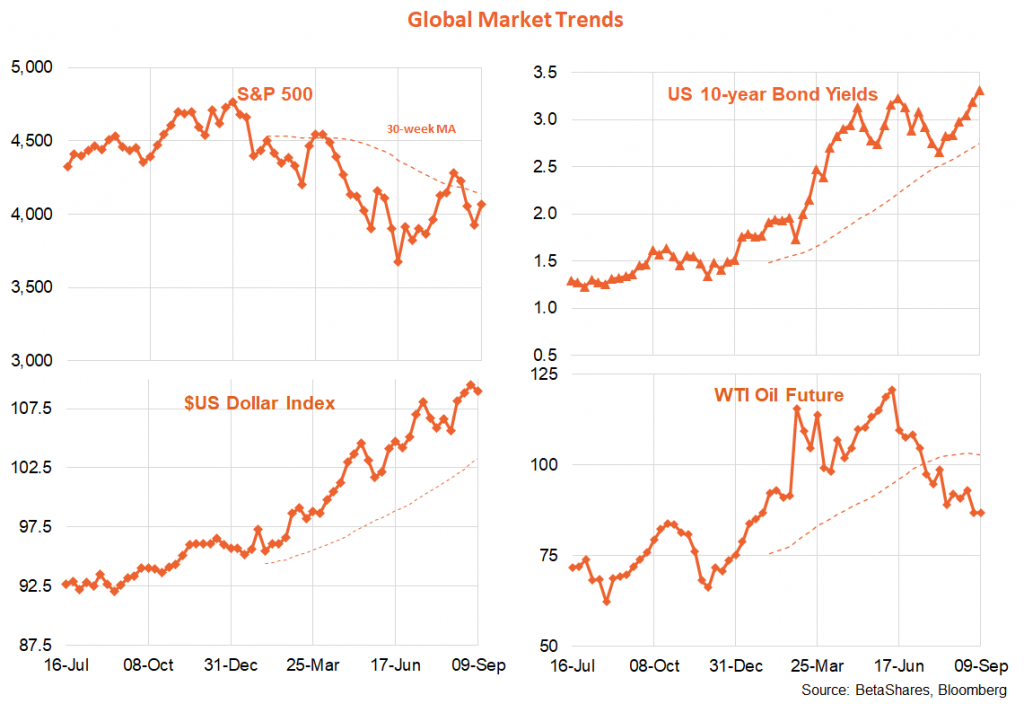

After several weeks of losses, global stocks bounced back last week on little new fundamental news, likely reflecting end-of-month rebalancing and profit taking from short sellers.

If there was one possible fundamental reason, it was a couple of Fed speakers (Brainard and Mester) acknowledging that the aggressive pace of policy tightening will eventually ease as growth slows and inflation declines. Wall Street leapt on the glimmer of good news. That said, most of their other comments remained hawkish, suggesting rates needed to rise to restrictive levels and stay there for some time. Fed chair Powell also chimed in with another barrage of aggressive comments. Indeed, US 2-year bond yields actually rose last week, reaching new high for the year at 3.56%.

Keeping with the hawkish sentiment, both the Bank of Canada and the European Central Bank hiked rates by 0.75%. OPEC also agreed to shave their production target by a modest 100k barrels per day, though continued China lockdowns kept oil prices flat over the week.

One interesting development last week was signs of lingering strength in the US economy, with the services sector PMI remaining firm in August and weekly jobless claims easing back. Along with recent improvements in consumer sentiment, it could be that the decline in petrol prices and some easing in some supply bottlenecks in recent months could be providing a ‘positive supply shock’ boost to demand – which ordinarily would be a positive for both bond and equity markets. The only concern is that the Fed appears to have concluded that a period of below trend economic growth (and rising unemployment) is required to sustainably bring down inflation.

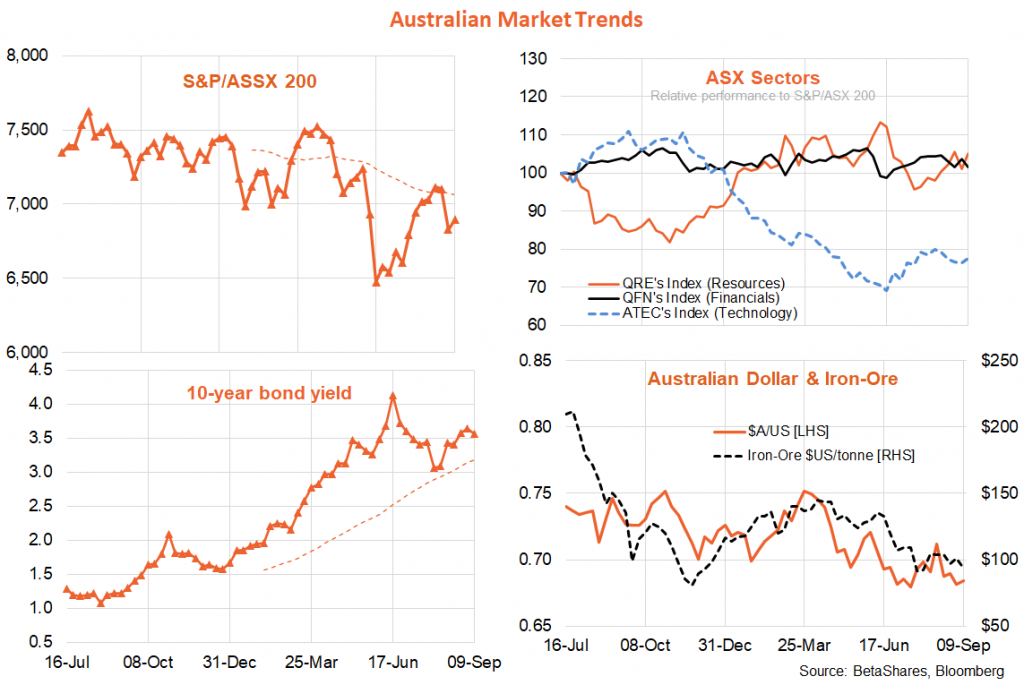

In Australia, the RBA hiked rates by 0.5% as widely expected, and the 0.9% gain in Q2 GDP affirmed the continued solid momentum in the economy, underpinned by consumer spending and employment demand. A rebound in ANZ job ads in August also suggested that hiring intentions in Q3 remain strong, despite the rise in interest rates to date. In a key speech, however, RBA Governor Lowe hinted that the Bank is getting closer to the point where it at least starts raising rates by 0.25% each meeting rather than 0.5%. In turn, this saw bonds spreads versus the US narrow somewhat last week. My base case is for only a 0.25% hike in both October and November – and a pause in December

Week ahead

The clear highlight this week will be the US consumer price index (CPI) report on Tuesday. Thanks to lower petrol prices, the headline CPI is expected to decline by 0.1% though core prices (i.e. excluding food and energy) are expected to rise by a still fairly firm 0.3%. Given the market’s extreme sensitivity to the inflation outlook, any upside or downside surprise could cause considerable volatility. Indeed, it would not surprise if the market rallied even if the CPI were in line with market expectations – on relief that it was not worse than expected.

A faster than expected decline in US inflation remains the main upside risk to global equity markets in coming months – though given a tight labour market and still solid growth in service sector prices, it still seems more likely than not that inflation won’t slow quickly enough to ease the Fed’s hawkish stance any time soon.

Another potential positive factor to watch this week is developments in Ukraine. With reports of Ukraine’s successful counter attack and territorial gains, there’s at least a glimmer of hope that Russia’s forces might actually crumble and/or someone finally taps Putin on the shoulder. To the extent it would help lower energy and food prices, any near-term resolution to the Ukraine war offers equity and bond markets at least a short-term reprieve from worrying about America’s hawkish central bank and red hot economy.

In Australia, we get further updates on consumer (Westpac/Melbourne Institute) and business sentiment (NAB) on Tuesday along with the labour market report on Thursday. Consumer sentiment is likely to remain weighed down by the rise in interest rates and decline in house prices – though so far at least this has not stopped them spending with abandon. Business sentiment, meanwhile, is likely to remain firm while there’s also likely to be a solid bounce back in August employment growth after last month’s surprise decline.

Have a great week!