Cameron Gleeson

5 minutes reading time

- Commodities

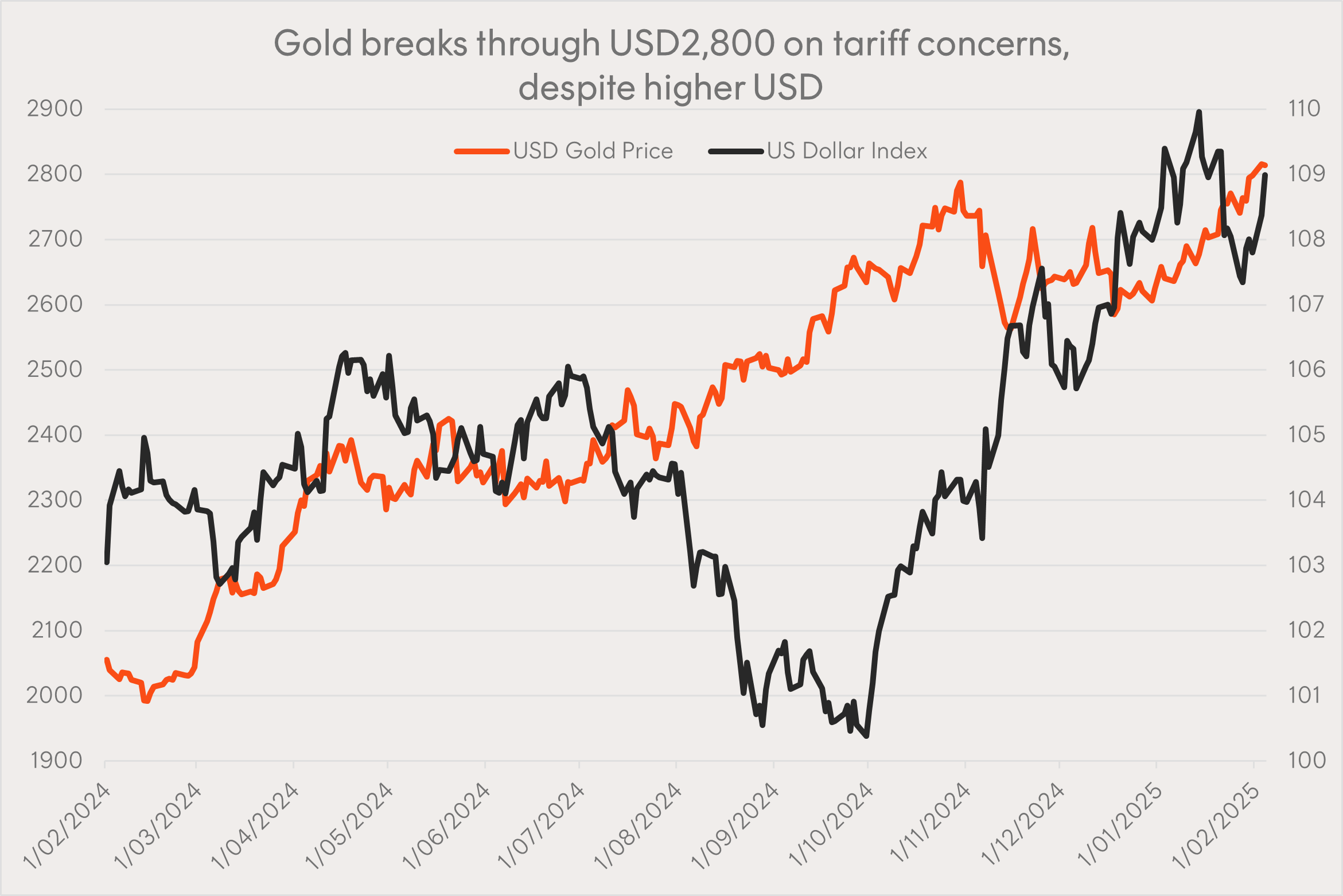

The gold price has punched through USD2,800 an ounce for the first time, after US President Trump signed an executive order to impose tariffs on Canada, Mexico and China, while threatening to do the same against the European Union.

The tariff uncertainty has stoked fears of inflationary pressure, particularly in the US, and a hit to global growth. Initially investors turned to other safe havens, like the US dollar (USD) and Japanese Yen, before pushing the USD gold price to a new all-time high. As at the time of writing, Trump has agreed to delay tariffs on Mexico and Canada, however the gold price remains above USD2,800 an ounce.

Source: Bloomberg, as at 4 January 2025. The US Dollar Index measures the performance of the dollar against a basket of other currencies. You cannot invest directly in an index. Past performance is not an indicator of future performance.

With strong structural and cyclical demand it’s likely we’ll see the gold price track higher from its current levels. Gold also provides protection against escalating trade wars, geopolitical conflict and fears relating to US government debt and Fed independence.

Structural Support – Central Banks

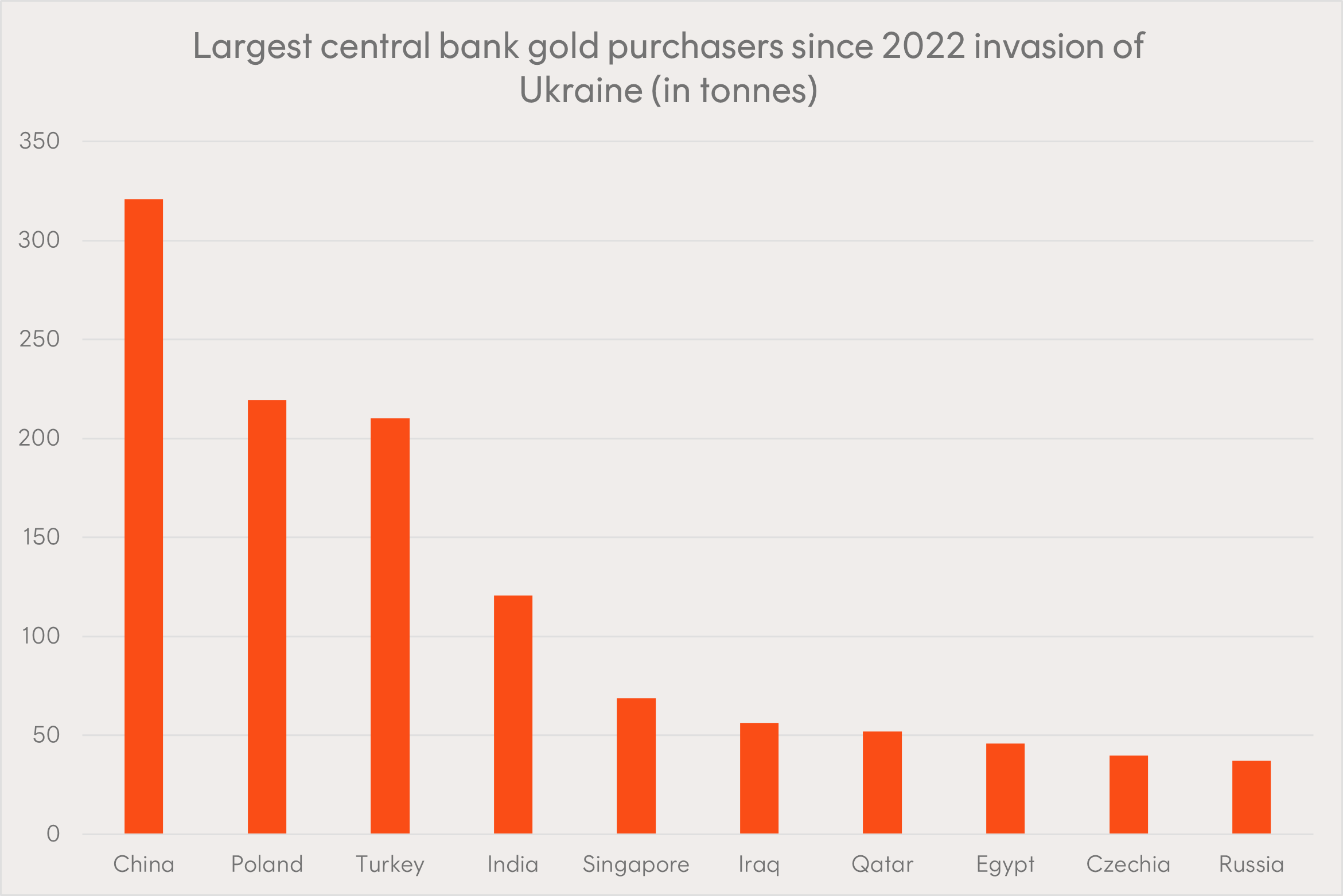

As geopolitical tensions have escalated over the last few years particular central banks have gone on a gold buying spree.

As a reliable store of value, gold is highly attractive for central banks seeking to diversify their reserves beyond foreign currencies like the USD and US Treasuries. In the wake of the Ukraine invasion, the US showed they were not afraid to ‘weaponise’ the dollar-centric global financial system by imposing crippling sanctions on another nation state. As the world’s reserve currency, the USD gives the United States enormous leverage on the world stage.

In response to this threat, the central banks of countries that wish to remain non-aligned or independent of the US have become huge buyers of gold in recent years. Since February 2022, total reported central bank buying has jumped five-fold thanks to emerging market and Eastern European countries like China, India, Poland, Turkey and Egypt.

Source: World Gold Council. Net purchases and sales from 1 February 2022 to 30 November 2024.

Goldman Sachs also reported that central bank buying at the end of 2024 came in significantly higher than their expectations, particularly from China.

Cyclical Support – Consumers and Investors

China and India are currently the world’s largest gold markets. More generally, Asia makes up more than 60% of annual demand (excluding central banks), so these consumers and investors provide significant support for higher gold prices.1 Over the past year, China has seen a boom in demand for gold jewellery, as the Chinese property crisis and slowing economy spurred a flight into gold. Gold buying was traditionally skewed to the older generation in China, but today 18-34 year olds make up a third of China’s gold jewellery sales.2 In the second half of 2024, Indian demand jumped thanks to strong economic growth and the reduction of customs duty on gold imports.

In addition, global investor appetite for gold ETFs finally turned around in 2024, booking the first aggregate annual inflow in four years.3

Trump, tariffs and a rising US budget deficit

Gold traditionally performs strongly in periods of uncertainty and when the economic outlook deteriorates.

While the initial reaction to Trump’s tariff announcement over the weekend centred on the risk to inflation, Trump’s previous trade war with China suggests that it may be economic growth rather than inflation which is most at risk. Any threat to US exceptionalism is net negative for the USD and net positive for gold. Given how stretched the USD is on a purchasing power parity basis right now, and how much volatility there is in currency markets, it may not take much for gold to rally strongly in USD terms. In fact, China is widely expected to announce fiscal stimulus in March. If market participants deem this support to be meaningful, we may see the USD fall in Australian dollar terms and gold rally in USD terms.

Furthermore, if the US deficit widens further under the new administration, concerns around the serviceability of US government debt may dampen investor appetite for Treasury bonds and weaken the USD. Historically, there has been a strong correlation between rising US budget deficits and gold prices.

Currency hedging your gold exposure is an important consideration.

Investment Implementation

In a period of escalating geopolitical tension and policy uncertainty, gold provides unique characteristics to diversify risk embedded in other asset classes. As such, adding some exposure to the USD gold price can improve diversification for traditional multi asset portfolios.

As the only currency hedged gold ETF available on the ASX, QAU Gold Bullion Currency Hedged ETF offers a purer exposure to the USD gold price rather than the AUD price of gold, and has seen the largest year-to-date inflows out of any ASX-listed gold bullion ETF.

Sources:

1. World Gold Council, Gold Outlook, 2025. ↑

2. Bloomberg, Why Are Chinese Consumers So Keen on Gold? | Big Take Asia, 30 January 2025. ↑

3. World Gold Council, Gold ETF Commentary, December 2024. ↑