David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

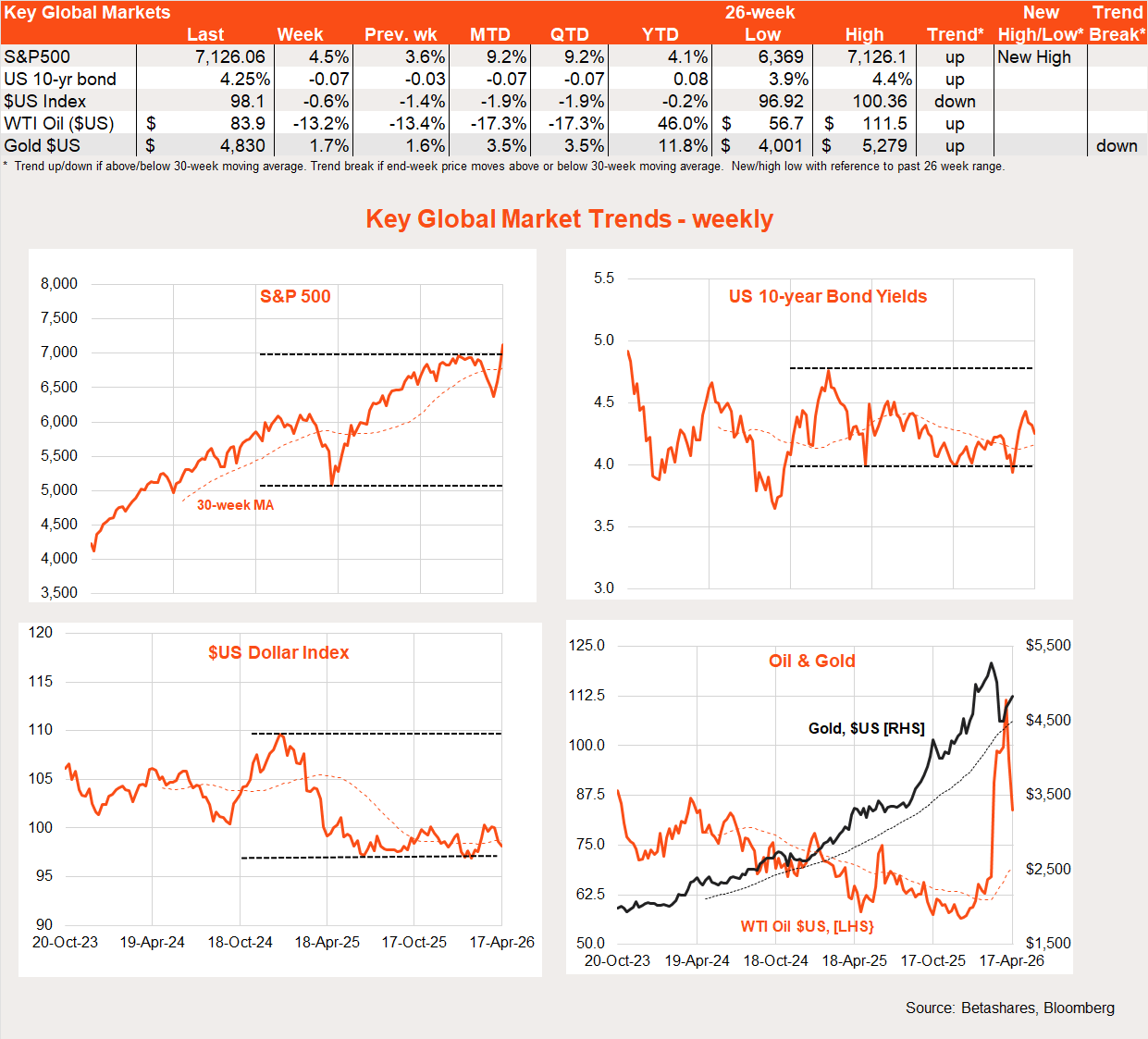

Global week in review: Optimism but Strait still closed

Global stocks rose further last week, reflecting hopes around on-again off-again US-Iran peace talks.

Global markets continued to be buffeted last week by on-again off-again peace talks. The week started on a dour note, with news of the failure of weekend peace talks. But Trump’s heavy hints that talks were ongoing supported market hopes through the remainder of the week.

In theory, a two-week ceasefire deal was supposed to have included a re-opening of the Strait of Hormuz. But within 24 hours of saying the Strait was open, Iran said it was closed again – due to the US’s own blockade of Iranian linked ships. At the time of writing, there’s news of the US seizing an Iranian ship, for which Iran has vowed retaliation. Iran has also denied US reports suggesting talks were set to resume.

Suffice to say confusion reigns supreme! If there’s one guiding light for markets, it’s the idea that the longer the war drags on and the higher oil prices go, the greater the political pressure on President Trump to cut a deal. In short, in TACO we trust – though patience is being tested.

Global week ahead: Brinkmanship continues

Global events will remain almost exclusively focused on Iran. Nothing much else matters in global markets at present.

At either extreme, we seem to face a best and worst case scenario this week.

- The worst case scenario is Iranian attacks on US military ships, potentially even sinking one with causalities. That could spark an “all bets are off” resumption of US/Israel missile strikes, potentially including Iranian energy infrastructure, which in turn could spark Iranian attacks on energy and water infrastructure across the Middle East.

- The best case scenario is no tit-for-tat ship attacks and an agreement to hold more talks.

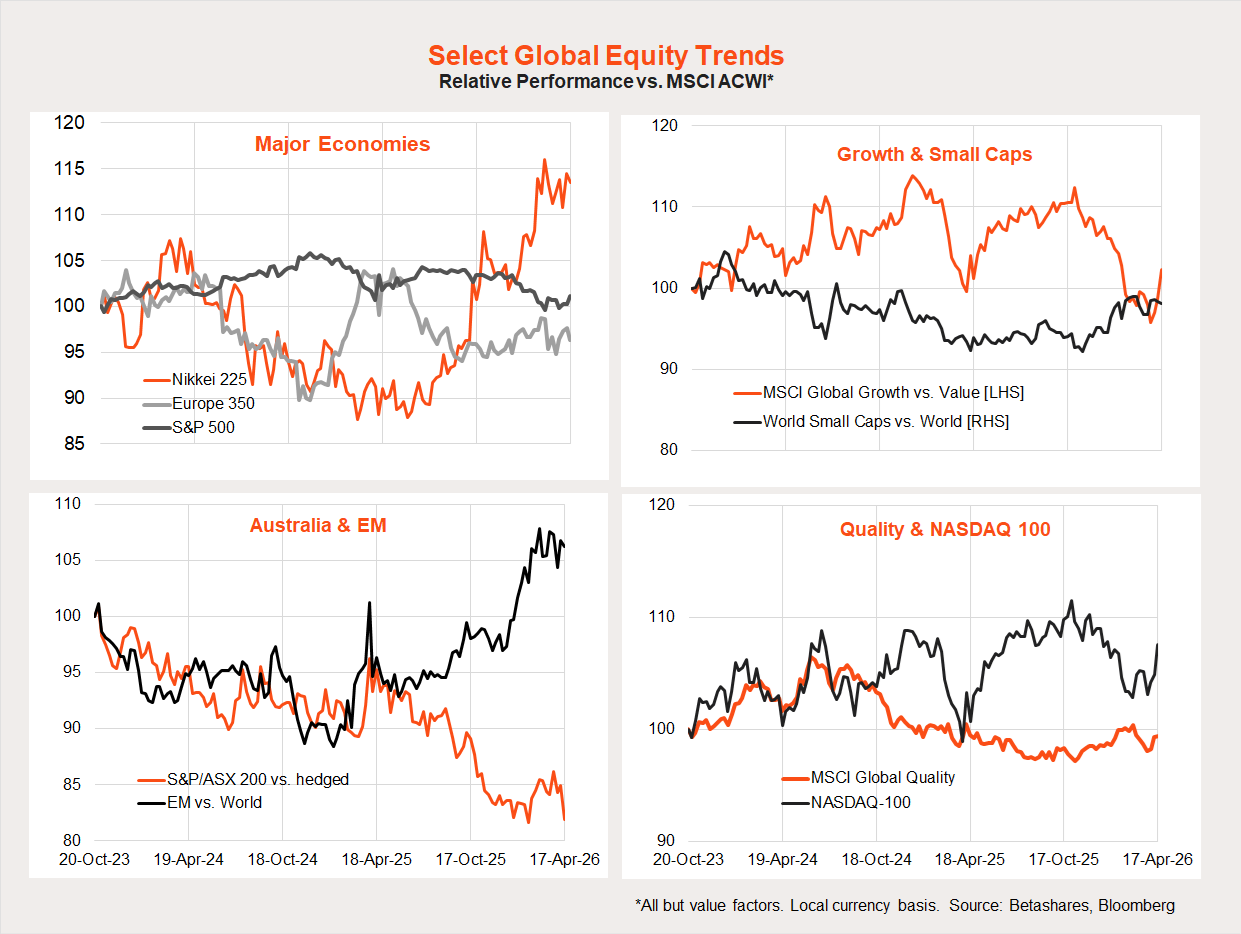

In other news, we’re entering the US Q1 reporting season with many major tech names due to report next week. The NASDAQ-100 has been on a tear in recent weeks, reflecting both peace talk optimism but also potentially a sense that AI disruption fears for the major players may be overdone. Tech companies are clearly cutting workers and costs, but whether they face a major loss of customers – or pricing power – due to AI remains to be seen.

Global equity trends: US outperforms

Global equity markets have staged a three-week rebound on peace-talk hopes. Indeed, overall global stocks and the S&P 500 are now trading above the levels prevailing just before the Iran war began.

What’s also of interest is that US stocks fell the least during the initial sell-off and have so far rebounded the hardest, with the NASDAQ-100 ending last week 6.9% above its weekly close on 27 February. Japanese and European stocks are still a little below their pre-war peaks, as is the case in Australia.

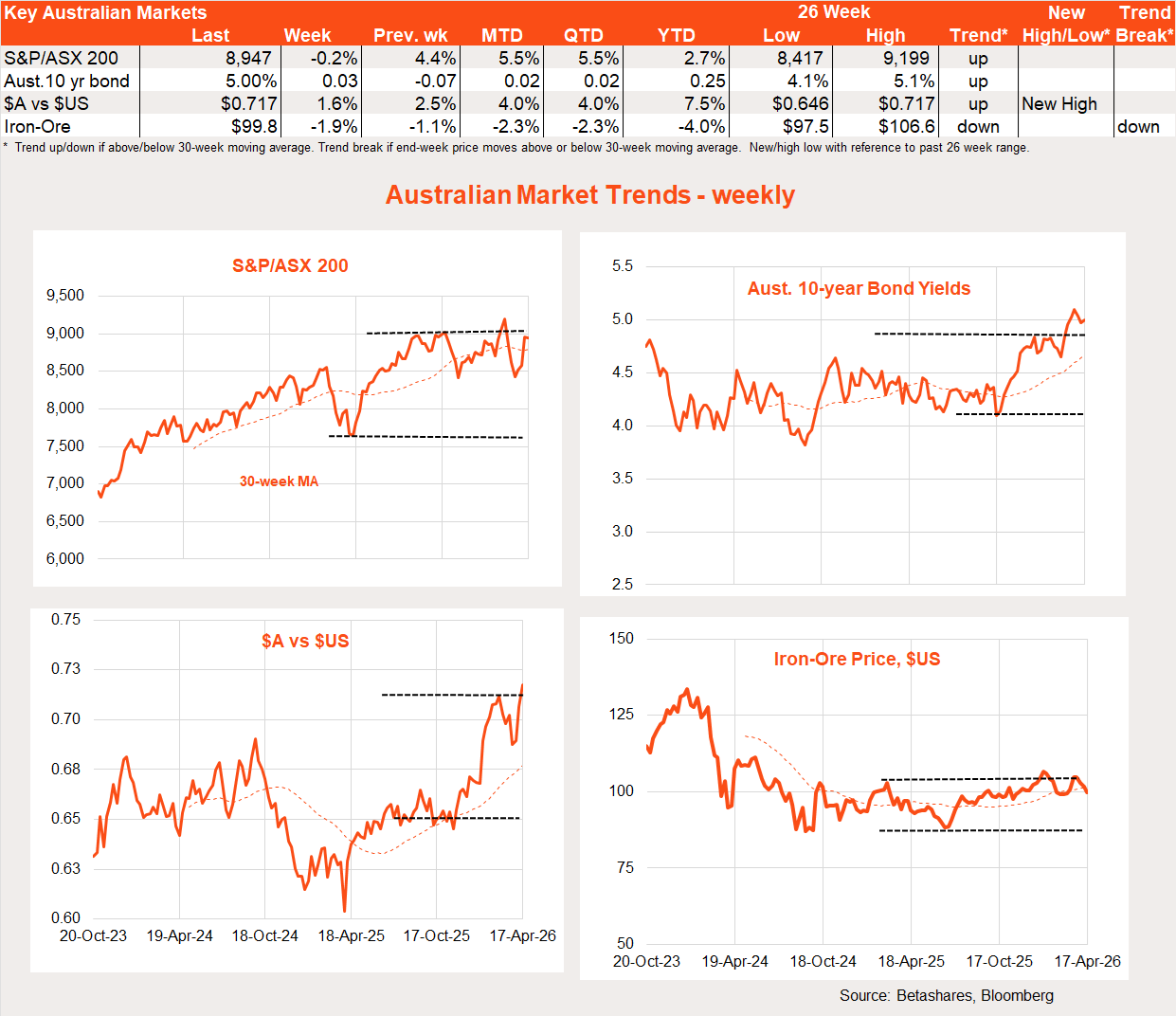

Australia in review: Confidence collapse

Local stocks lagged the global rebound last week, not helped by news of a collapse in local consumer and business confidence.

Weaker energy stocks on peace-talk optimism and concerns around local banks also dragged on the market. Westpac last week announced an increase in bad debt provisions due to an expected softening in the economy. NAB this morning has released a similar warning.

Other key local news last week were the Westpac and NAB surveys of consumer and business confidence respectively. Perhaps not surprisingly, both surveys revealed a large drop in confidence by both groups during March, reflecting the surge in petrol prices and related interest rate fears. The NAB measure of business conditions, at least, held steady.

Almost holding steady was the labour market, with news last week that employment grew by 17k in March – largely in line with market expectations – and enough to keep the unemployment rate at 4.3%.

All up, despite the knee-jerk collapse in confidence measures, actual economic activity is still holding up – leaving the RBA on track to raise rates again next month.

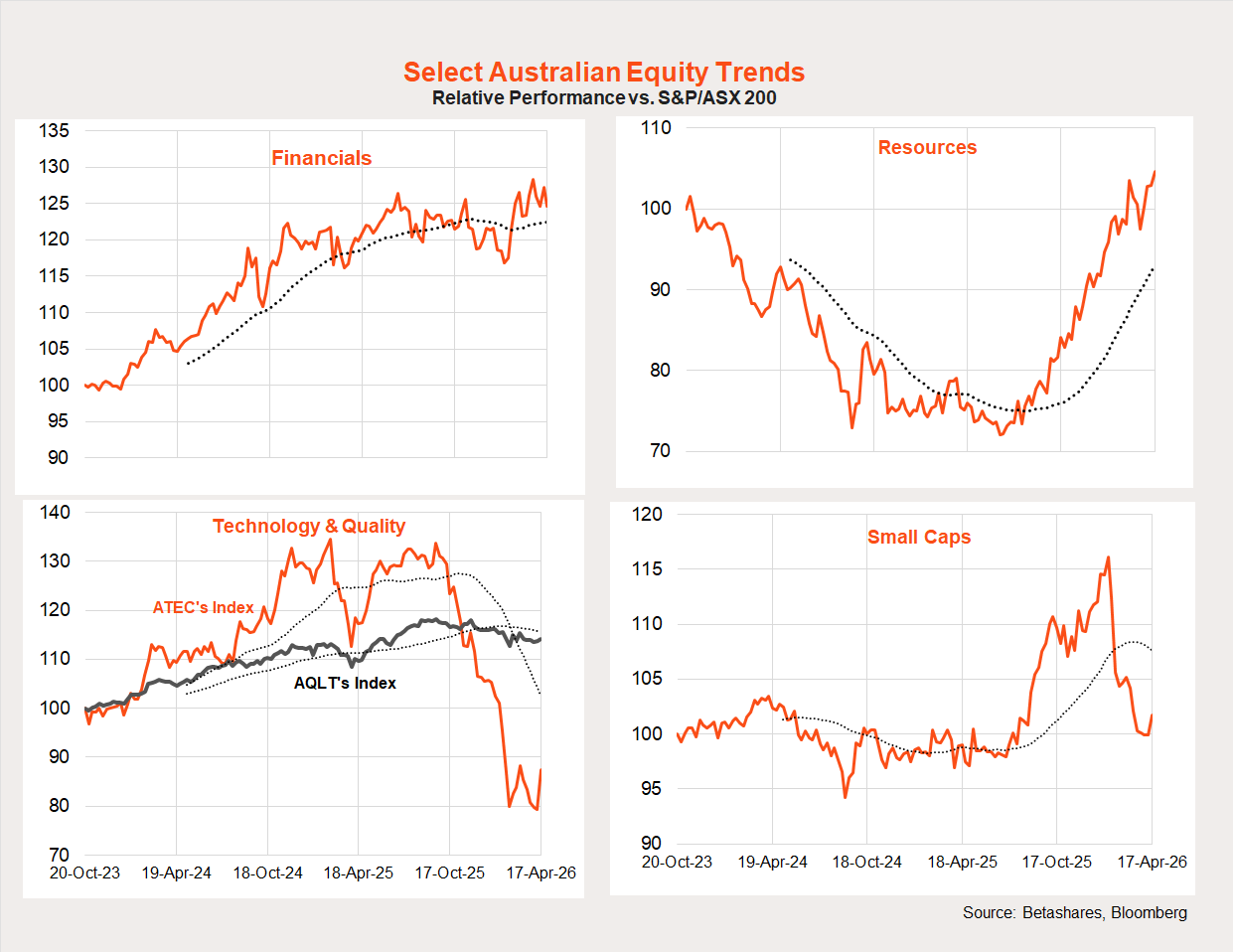

Local equity market trends: Technology bounce

The Iran war had initially not been kind to high-beta local exposures such as technology and small caps. That said, technology enjoyed a solid bounce last week – and small caps to a lesser degree – while the financial sector sold off.

Australia week ahead: Iran

There’s little major local economic news this week, with developments in the Iran war to remain the major focus.

Also of note will be any further hints about the May budget and whether other banks also announce higher bad debt provisions.

Have a great week!