All in on AI? 3 ways to reduce concentration risk

Hugh Lam

7 minutes reading time

- Technology

Related articles

The bar continues to be raised for Big Tech companies every quarter. So how did they perform in the most recent Q4 quarter?

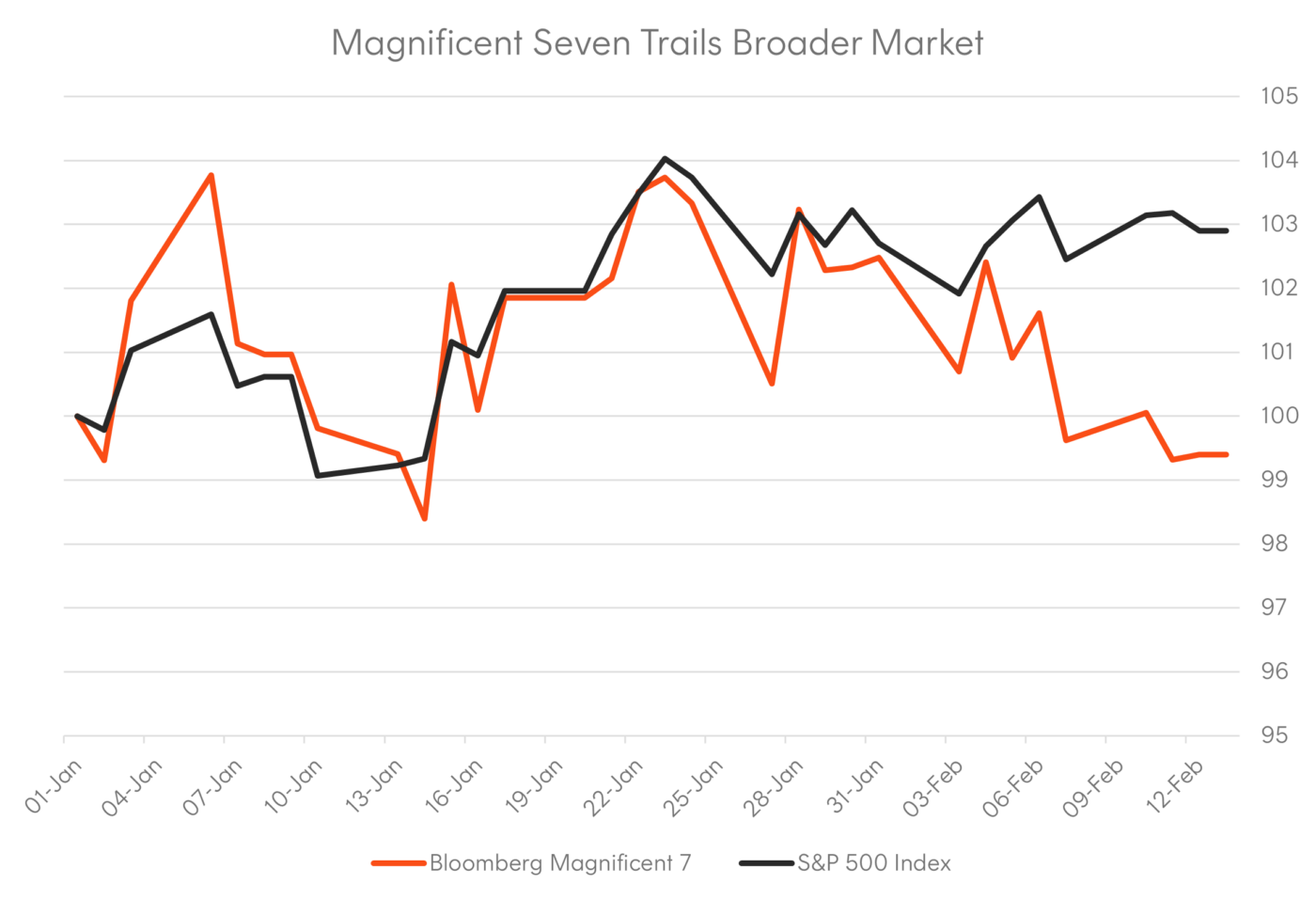

At a high level, the reported earnings (excluding Tesla, and Nvidia which is set to report later this month) were slightly better than consensus expectations from stock analysts. Despite this, three out of six experienced a stock price fall post announcement, and year-to-date the Bloomberg Magnificent 7 index has underperformed the broader market.

Chart 1: Bloomberg Magnificent 7 vs S&P 500 Index Performance – 1 January 2025 to 13 February 2025

Source: Bloomberg, Betashares. 1 January to 13 February 2025. Rebased to 100 as at 1 January 2025. You cannot invest directly in an index. Past performance is not an indicator of future performance.

In addition, the AI narrative continues to evolve following the announcement of DeepSeek – a Chinese open-source AI model that rivals the performance of OpenAI’s at just a fraction of the cost.

Given its efficiencies and lower development costs, DeepSeek raises the question as to whether Big Tech companies are spending too much on building out data center capacity. As a result Microsoft, Alphabet and Amazon sold off as markets marked a red tick against slowing cloud revenue growth numbers.

However, we will likely see companies that are able to build and monetise end-user software applications become net beneficiaries. We saw this with Meta’s share price reaction post earnings – their spending has had an immediate effect on the company’s bottom line, generating higher average revenues per user. The stock is up over 20% year to date at the time of writing.

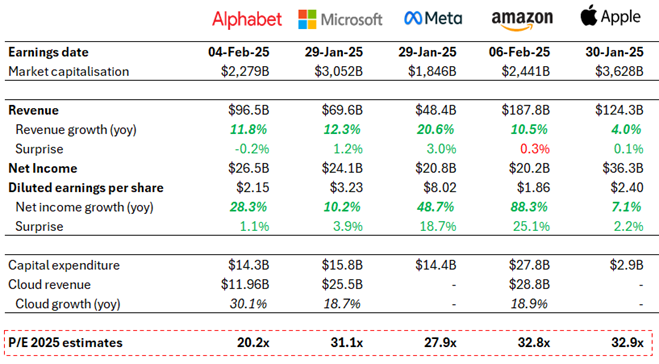

Q4 2024 Earnings Dashboard

Source: Bloomberg. Market capitalisation and P/E (2025 being next 4 quarter estimates) estimates data as of 14 February 2025. Revenue, earnings and capital expenditure data as at relevant company’s earnings date. Revenue and EPS surprises from FactSet. In US dollars. Tesla excluded on the view that its business model is not within the same supply chain as the companies represented above.

Key takeaways

- Google Cloud revenue growth slowed from 35% yoy in the previous quarter down to 30%, but release of its own TPUs (tensor processing units)[1] and its Gemini flash AI models can help accelerate Cloud segment growth.

- Alphabet is now generating annual revenues of US$110 billion for Cloud and YouTube, demonstrating that the company can sustain high-20% growth this year for both segments.

- Full-year capex guidance was raised to US$75 billion.

- AWS (Amazon’s cloud unit) revenue grew 19% yoy for the third consecutive quarter, despite power capacity shortages hindering the cloud unit from bringing new data centers online. Amazon anticipates these constraints will ease in the second half of 2025.

- Amazon’s retail segment offset the challenges in cloud, posting a 7% increase in online sales to US$75.6 billion.

- Full-year capex guidance raised to over US$100 billion.

- The rate of growth in Microsoft’s Azure cloud computing unit continued to slow, growing 31% yoy compared to 34% and 35% in the two prior quarters. Similar to Amazon, data center capacity constraints rather than lack of demand are contributing to the marginal slowdown according to Microsoft CFO, Amy Hood.

- Positively, there is a strong backlog of AI commitments (from OpenAI) which should keep the company well positioned in the AI-software space.

- Operating margins expanded roughly 190 bps despite muted top-line growth, led by lower SG&A costs (sales, general and administrative costs) as a share of revenue.

- Meta was a stand-out performer among the Magnificent 7 that have reported, benefiting from the investments made in building out AI solutions. Average prices per ad were 14% higher in the fourth quarter.

- Additionally, the release of Llama 4 may bolster is position vs other LLMs (large language models), given interest in DeepSeek’s open-source approach.

- The number of daily active people (DAP) was 3.35 billion on average, an increase of 5% year-over-year.

- Meta shares are up over 20% year to date.

- Apple had a challenging quarter with iPhone sales muted and foreign smartphone brands in China such as Vivo and Huawei gaining market share.

- However, gross margin and services segment growth were bright sports which should support the company to improve its profitability and drive higher margin revenue streams.

- Interestingly, sales were stronger in countries where Apple Intelligence is available, highlighting the appetite for end-user AI applications.

US equities beyond Big Tech

Whilst a lot has been said about the levels of concentration and valuation premium that Big Tech brings to investor portfolios, it is hard to ignore the structural growth story of these companies which has driven US equity market exceptionalism.

Ultimately, earnings for the Mag 7 will still continue to grow at a healthy clip in the next few quarters but the level of outperformance experienced in recent years will likely cool, prompting investors to explore other areas of the market that can deliver healthy earnings growth without the valuation premium.

Chart 2: Historical and future estimated year over year (YoY) earnings per share (EPS) growth rates

Source: J.P. Morgan Asset Management. As at November 15 2024. Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. *Earnings estimates for 3Q2024 onwards are forecasts based on consensus analyst expectations. Actual results may differ materially from forecasts

Next week, we will explore the other non-tech sectors with strong earnings momentum and other investment opportunities in US and global equities.

[1] TPUs are application-specific integrated circuits developed by Google. They are more specialized than CPUs and GPUs – only found in Google data centers to run its most popular AI services such as Seach and YouTube.

Betashares Capital Limited (ACN 139 566 868 / AFS Licence 341181) (“Betashares”) is the issuer of this information. This is general information only and we have not taken your individual circumstances, financial objectives or needs into account when preparing it. This information is not a recommendation to invest in any financial product or to adopt any particular investment strategy. Future results are inherently uncertain. This information may include opinions, views, estimates and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in such forward-looking statements. Opinions and other forward-looking statements are subject to change without notice. Any opinions expressed are not necessarily those of Betashares.

Explore

Markets

1 comment on this

[email protected]