All in on AI? 3 ways to reduce concentration risk

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Week in review

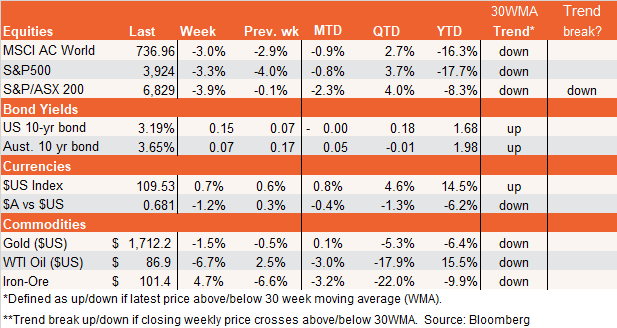

Global equities retreated further last week and bond yields rose as the very hawkish speech by Fed chair Powell from the previous Friday continued to cast a long shadow. Most Fed speakers continued to talk of the need to raise rates aggressively to bring down inflation even in the face of recession risks. At this stage it still seems likely the Fed will hike rates a further 0.75% at the upcoming September 20-21 policy meeting.

Accordingly, markets are unsure how to interpret incoming US activity data – is it good or bad news, for example, if the economy remains resilient or shows signs of tipping into recession? Strong growth (such as US payrolls on Friday) only raises the risk of even more aggressive Fed rate hikes, while signs of slowing growth (as in the housing sector) lessen interest rate risk but increase corporate earnings risk.

The one unambiguous economic reading at present is inflation – if US inflation shows signs of falling quickly (and there are tentative signs that it might), that would clearly be a positive for both bond and equity markets. The next important US inflation report is the CPI next Tuesday, September 13.

Non-US developments are also hardly market-supportive – with Russia shutting off gas supplies to Europe over the weekend for ‘maintenance’ purposes, and China persisting with locking down cities when and if COVID cases appear.

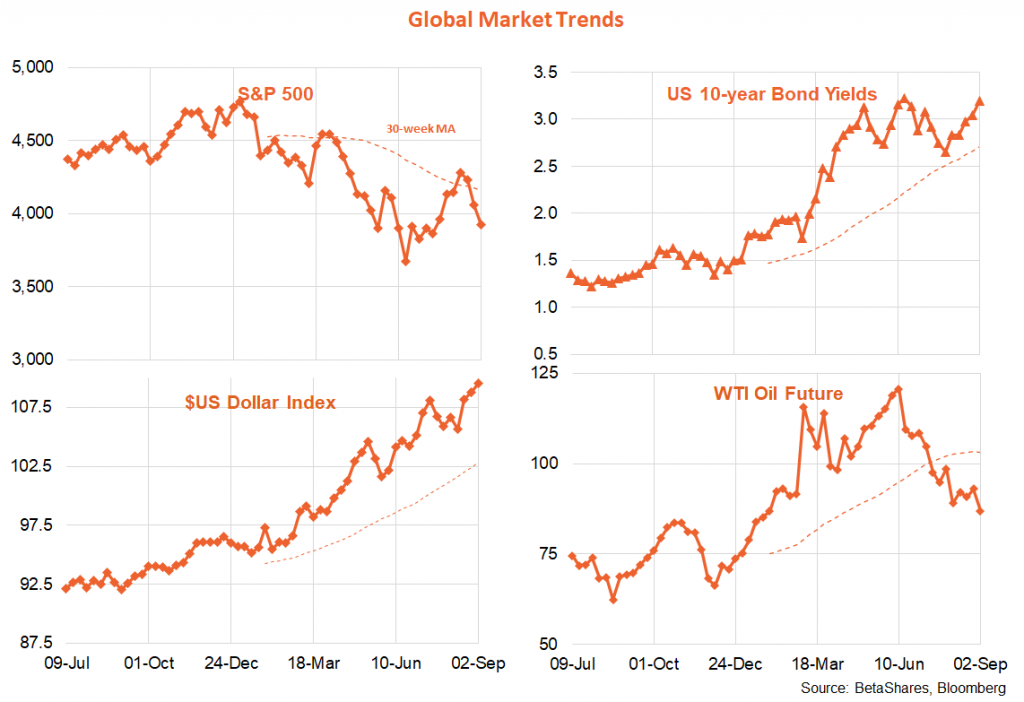

As evident in the chart set below, US 10-year bond yields and the US dollar have re-touched their highs for the year even as oil prices head lower. US stocks have given back roughly half their rally since mid-June.

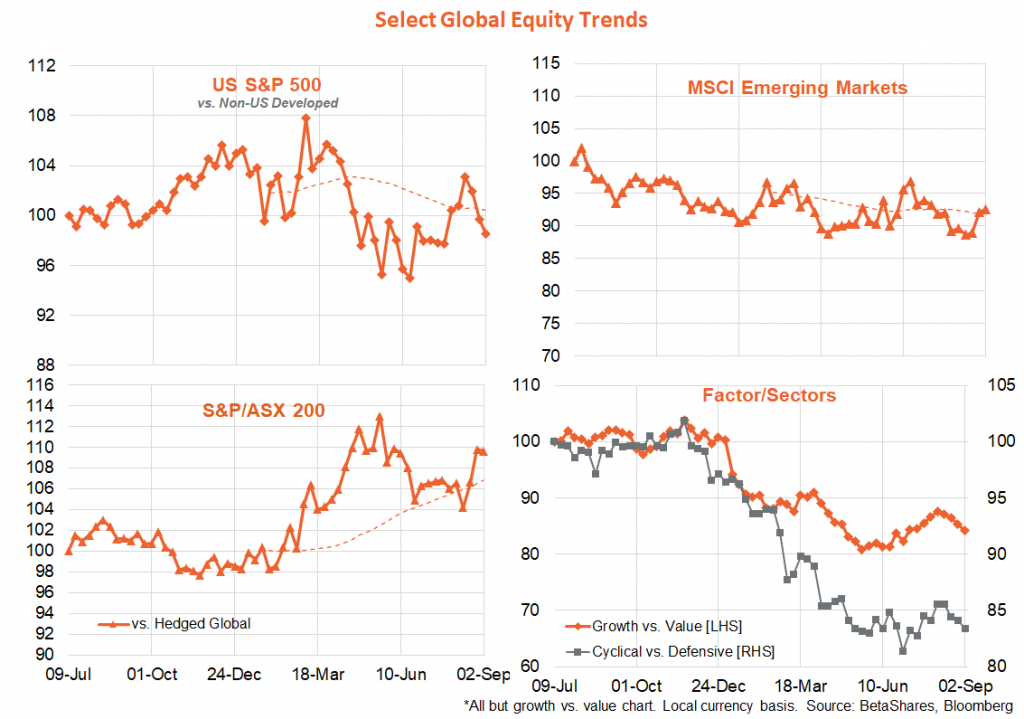

Looking at equity trends, the pullback in risk in recent weeks has seen growth underperform value again (despite rising bond yields) while cyclicals have also ceded ground to defensives.

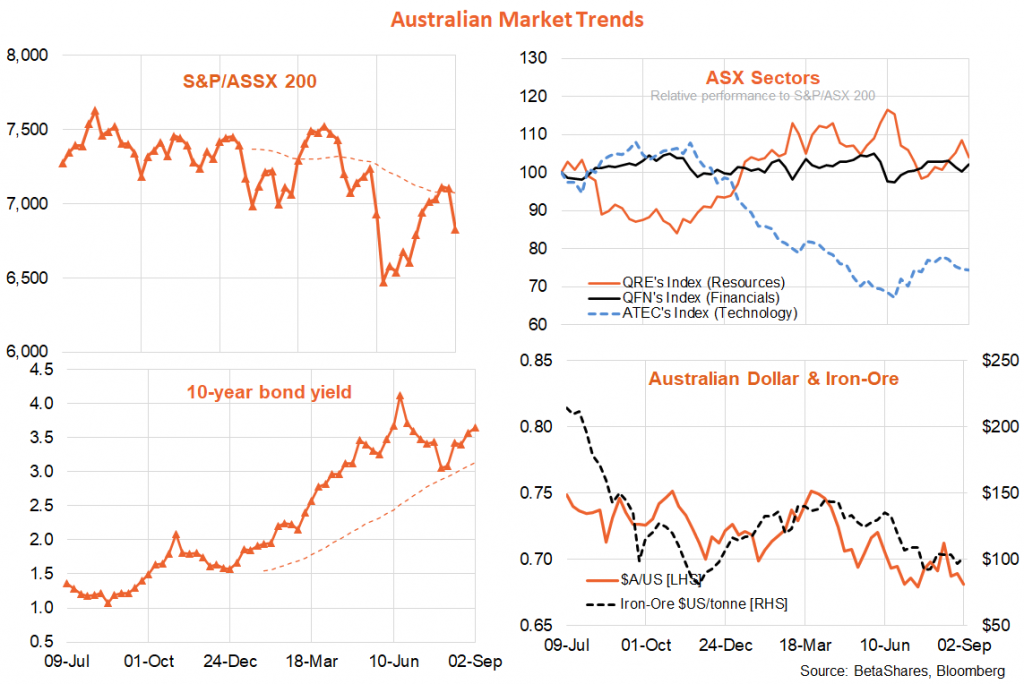

In Australia, as expected we got mixed economic data last week – with resilient retail spending and still firm business investment but accelerating weakness in housing construction and house prices. As in the US, the resilience in local employment demand and retail spending remains impressive despite the aggressive interest rates hikes so far – though there remains an element of post-COVID recovery still benefitting both.

That said, local 10-year bond yields remains below their highs for the year, with the interest-rate differential versus the US narrowing since mid-June. At this stage at least, markets no longer expect the RBA to raise the policy rate to more than 4% – a rate which was even higher than that expected in the US. Together with global risk-off sentiment, that has seen the $A drop toward its lows for the year, with a drop toward US62-63c quite possible in coming months.

Week ahead

It is a data light week in the US with another speech by Powell on Thursday of most interest (though he’s hardly likely to change his hawkish tone anytime soon).

US service sector reports will also play into the debate over whether the Fed hikes by 50 or 75 bps later this month. High European inflation caused predominantly by surging energy costs means the European Central Bank will likely hike rates by at least another 0.5% on Thursday, with some risk of a larger 0.75% move.

OPEC also meets early this week with interest in whether the group maintains or actually cuts production (as some members want) given the recent easing in oil prices.

In Australia, despite falling house prices it seems likely the RBA will hike by a further 0.5% at Tuesday’s policy meeting, in view of the ongoing strength in employment and consumer spending. This decision will be supported by a likely firm Q2 GDP report on Wednesday, with quarterly economic growth of at least around 1% expected – underpinned by solid consumer spending.

Have a great week!

1 comment on this

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.