Charts of the month – June 2026

Annabelle Dickson

6 minutes reading time

- Fixed income, cash & hybrids

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Markets went into freefall on Friday following a speech from US Federal Reserve Chair, Jerome Powell. The S&P 500 fell 3.37%, its biggest one-day fall since the extreme volatility in mid-June. Australian markets followed on Monday, falling over 2% by midday.

Should investors be concerned? What does this mean for markets and the economy? And what is Jackson Hole anyway?

Jackson Hole

Let’s address the easy question first. Jackson Hole Economic Symposium is an annual meeting of central bankers, academics, economists, and policymakers from around the world.1 The highlight each year is an address from the Chair of the US Federal Reserve (Fed), which provides insight into the Fed’s thinking on the economy, and importantly, interest rates.

This year’s speech was particularly important, as there’s been significant speculation in markets recently about whether the Fed would pause rate hikes, change course, or continue unabated.

As Chamath De Silva CFA, Senior Portfolio Manager at BetaShares explained, the speech “will likely define the macro narrative over the remainder of the year”.

The speech

The speech itself was rather brief – just eight minutes long. But the message was clear.

“Powell came in with the singular focus of dispelling notions of an upcoming Fed pivot,” said De Silva.

Following the speech, he summarised the key points:

- Estimates of neutral “are no place to pause or stop hiking” amid the current inflationary pressures, and the Fed intends to take policy well into restrictive territory.

- We should expect a sustained period of below-trend growth in the US economy, which will bring “some pain to household and businesses” (i.e. a recession is a feature, not a bug).

- If history is a guide, there are negative consequences of easing up on the hiking cycle too early, and the Fed’s commitment to price stability is “unconditional”.

The consequences

The most obvious and direct consequences will be felt in interest rates. BetaShares Chief Economist David Bassanese commented that it “seems likely the Fed will hike by a further 0.75% at the September meeting”. This would bring the US Fed Funds Rate Target range to 3-3.25%, the highest level since 2008.2

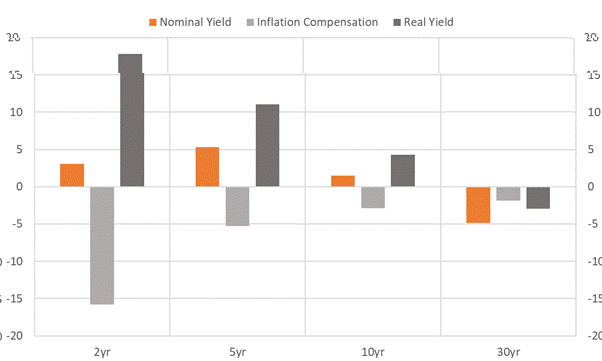

Higher rates affect bonds too. The chart below depicts Friday’s moves in bond yields and inflation expectations.

Chart 1: US Treasury curve change on 26 August 2022 (in basis points)

The chart shows that over two-, five-, and 10-year periods, inflation expectations in the US fell, while nominal yields rose slightly. The result was significantly higher real yields (i.e., inflation-adjusted) across those periods. Essentially, markets expect higher rates and lower inflation, making bonds more attractive on an inflation-adjusted basis.

What’s happening with 30-year yields though? De Silva explained: “Real and nominal yields fell in the 30-year sector, reflecting the negative long-term growth implications of the Fed taking policy to restrictive levels.”

The effect goes beyond fixed income. Interest rates are a critical input into company valuations as they represent the ‘risk-free rate’. A higher risk-free rate means that all assets need to produce a higher rate of return, which lowers their current valuation.

De Silva also pointed out that “the potential negative impact on equities is also from lower corporate earnings growth expectations from the Fed deliberately trying to slow down the economy and higher debt servicing costs.”

Why it matters for fixed income

For fixed income investors, the news of higher rates may seem unequivocally positive. Higher yields = higher returns, right?

Over the longer term, this is true.

However, because bond yields and prices are inversely related, higher yields generally result in lower bond prices. If yields were to fall again though, this would generally result in higher bond prices.

| Fund name | ASX code | Exposure | Yield |

| BetaShares Australian Composite Bond ETF | OZBD | A diversified portfolio of high-quality Australian corporate and government bonds selected on the basis of risk-adjusted income potential, while controlling for overall interest rate and credit risk. | 4.44%* |

| BetaShares Australian Investment Grade Corporate Bond ETF | CRED | A portfolio of senior, fixed-rate, investment grade Australian corporate bonds. | 5.92%* |

| BetaShares Australian Government Bond ETF | AGVT | A portfolio of high-quality bonds issued by Australian federal and state governments, and with a component issued by supranationals and sovereign agencies. | 4.01%** |

| BetaShares U.S. Treasury Bond 20+ Year ETF – Currency Hedged | GGOV | A portfolio of high-quality, long-dated, income-producing US Treasury bonds, hedged into AUD. | 2.77%** |

Note: Yields as at 30 August 2022. Yields will vary and may be lower at the time of investment. *Yield to worst. **Yield to maturity. See footnotes for explanation of Yield to Worst and Yield to Maturity.

The situation for floating-rate securities is quite different. As coupon payments are tied to interest rates, their coupon payments rise as interest rates rise. This means that their capital value is unaffected by rising interest rates.

However, unlike fixed-rate securities, these do not benefit from falling rates.

These are some of the BetaShares funds offering exposure to floating-rate securities:

| Fund name | ASX code | Exposure | All-in yield^ |

| BetaShares Australian Bank Senior Floating Rate Bond ETF | QPON | A portfolio of some of the largest and most liquid senior floating rate bonds issued by Australian banks. | 3.32% |

| BetaShares Australian Major Bank Hybrids Index ETF | BHYB | A portfolio of listed hybrid securities issued by Australia’s ‘Big 4’ banks. | 5.20% |

| BetaShares Active Australian Hybrids Fund (managed fund) | HBRD | An actively managed, diversified portfolio of primarily hybrid securities. | 4.96% |

Note: Yields as at 30 August 2022. Yields will vary and may be lower at the time of investment. ^See footnotes for explanation of All-in yield.

| There are risks associated with an investment in each of the above funds. For more information on the risks and other features of each fund, please see the fund’s Product Disclosure Statement and Target Market Determination which are available at www.betashares.com.au. |

* Yield to Worst (YTW) refers to the annualised total expected return of a bond if it is held to maturity or is called, the bond does not default, and the coupons are reinvested [at the Yield To Worst (YTW)]. The YTW is the lower of either YTM or Yield to Call (YTC), where YTC is calculated in the same way as YTM but replacing the maturity date with the call date. The fund’s YTW is the weighted average of its underlying bonds’ YTWs. The YTW for FX-hedged exposures reflects the annualised costs and benefits of FX hedging for relevant funds.

** Yield to Maturity (YTM) refers to the annualised total expected return of a bond if it is held to maturity, the bond does not default, and the coupons are reinvested [at the Yield to Maturity (YTM)]. The fund’s YTM is the weighted average of its underlying bonds’ YTMs. The YTM for FX-hedged exposures reflects the annualised costs and benefits of FX hedging for relevant funds.

^ All-in yield refers to the sum of a floating-rate security’s Discount Margin and its reference benchmark rate. The fund’s all-in yield is the weighted average of its underlying securities’ all-in yields. Discount Margin (DM) refers to the difference or spread between the expected return of a floating-rate security and that of its underlying index, expressed as a margin above the underlying reference benchmark rate. The fund’s DM is the weighted average of its underlying securities’ DMs. For AUD floating-rate securities, the reference benchmark rate is typically the Bank Bill Swap Rate (BBSW). For securities with optionality, this is the DM to first call, where the calculation replaces the security maturity date with its first call date.

1. https://www.kansascityfed.org/research/jackson-hole-economic-symposium/

2. https://tradingeconomics.com/united-states/interest-rate

Explore

Macro & markets