All in on AI? 3 ways to reduce concentration risk

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

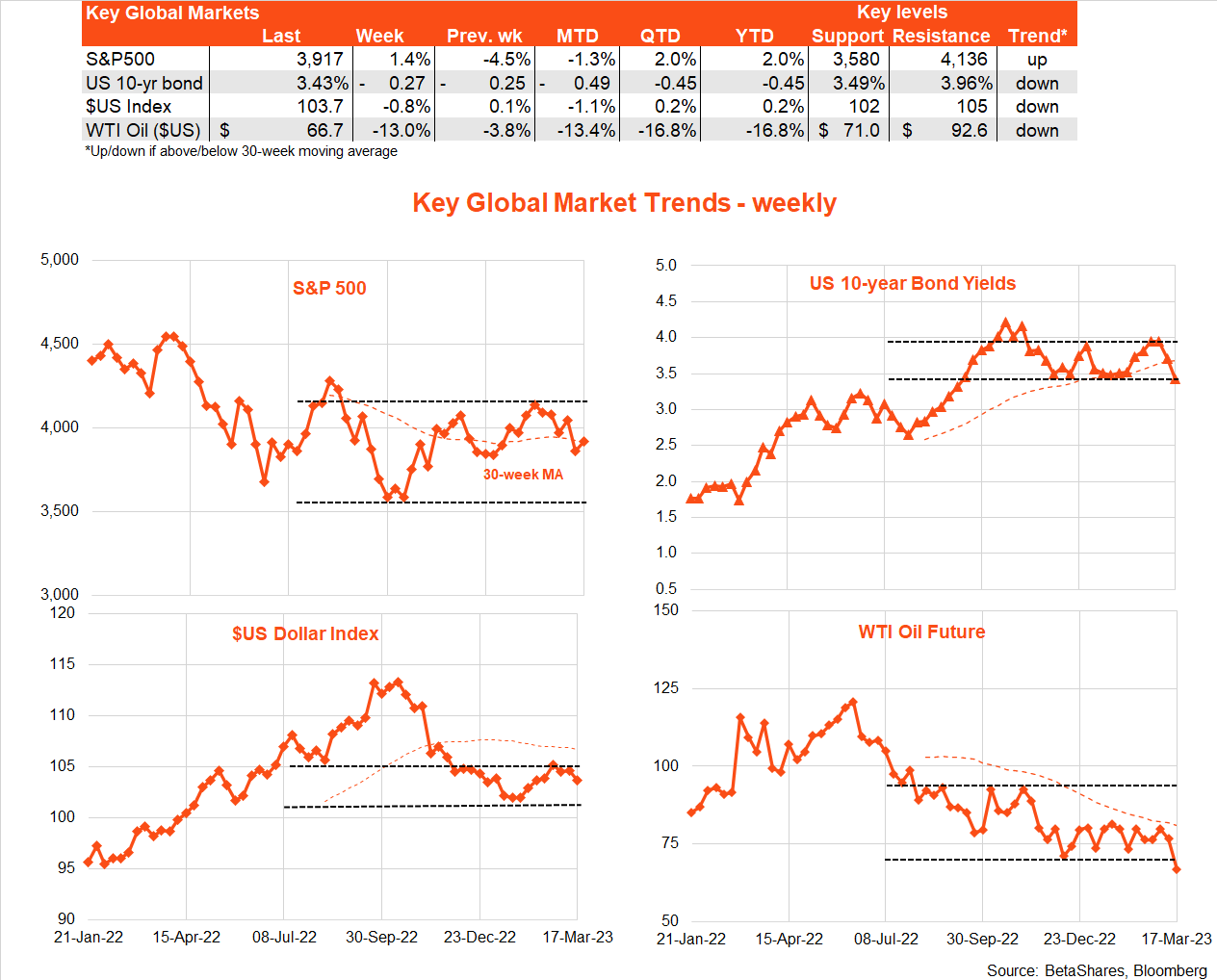

Global markets

Global equities enjoyed something of a relief rally over the past week as the world’s financial regulators played ‘whack a mole’ as each new banking problem raised its head. The US S&P 500 bounced back 1.4% after a 4.5% decline the previous week.

The past two weeks have seen bond yields plummet, which has helped partly insulate equities from concerns about financial instability and a severe tightening in credit. As would be expected perhaps, yield-sensitive areas such as technology have fared best, while banking stocks have been pummelled. The NASDAQ-100 index, for example, rebounded 5.8% last week. Gold has benefited from the drop in bond yields and initial weakness in the US dollar when financial instability was confined to US regional banks.

Two key financial developments last week were 1) evidence of substantial borrowing ($US165b) from the Fed by regional banks to shore up their funding in the face of flighty depositors and questionable asset valuations, and 2) the shotgun sale of Credit Suisse to UBS aided and abetted by regulators.

Somewhat lost amid the market mayhem, US economic data has remained reasonably firm. US core consumer prices rose slightly more than expected, by 0.5% in February. After bouncing higher the previous week, weekly jobless claims dropped back 20k to remain at a very low 192k. There are also signs from housing starts and home builder confidence that the recent easing in bond yields has helped stabilise the US housing market somewhat, which is perhaps a little premature for the Fed’s liking.

In other key news, the European Central Bank wanted to demonstrate it was so unworried about potential financial instability that it ploughed ahead with a long-telegraphed decision to raise rates a further 0.5%.

While markets and regulators will keep a careful watch for further instances of financial fragility, the week ahead will otherwise be dominated by the Fed’s policy meeting, due to conclude early Thursday morning Australia time. While recent financial instability has not become bad enough to likely stop the Fed from raising rates by 0.25%, it has probably killed off the risk of a 0.5% hike – which recent firm inflation and activity data would have otherwise likely triggered.

Also important following the Fed meeting will be an update on the Fed’s ‘dot plot’, or expected path for interest rates over the next year or so. Prior to the recent bout of financial instability, Fed chair Powell had signalled a likely increase in the expected peak Fed funds rate range from the 5-5.25% indicated back in December. Will the Fed still increase this expected peak, and if so, by how much?

My inclination is that it will – but likely less than would have been the case if SVB had not blown up a fortnight ago. I suspect we’ll see an expected end-23 Fed fund target range of 0.25% more at 5.5-5.75%.

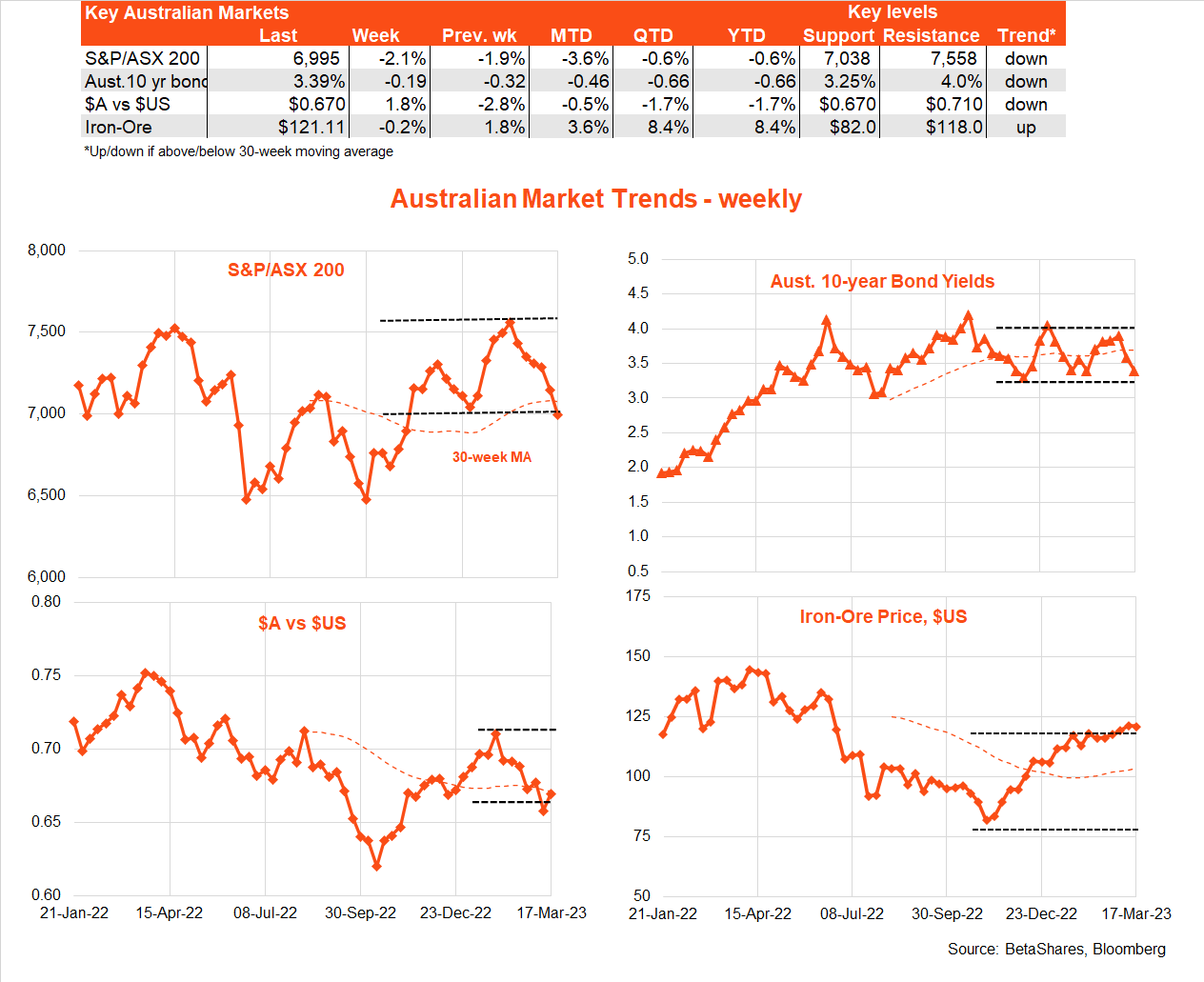

Australian market

Local stocks and bond yields fell last week, with the Australian sharemarket underperforming of late given its high exposure to financials and low exposure to technology. Helped by China’s re-opening hopes, iron-ore prices remained firm.

Local economic data was mixed to firm last week, with consumer confidence steady at still very depressed levels and business confidence dropping back somewhat. Offsetting this were still overall firm business conditions according to the NAB survey and, of course, the blockbuster 64k gain in employment during February.

The labour market report effectively repudiated early thoughts that employment growth was weakening, given job losses over December and January. It now seems more likely that year-end weakness did in fact reflect seasonal adjustment quirks after all.

All up, recent economic reports still seemingly have the RBA on track to raise rates a further 0.25% in April, subject to remaining local data such as retail sales and the monthly CPI report to come. The RBA will also take note of what the Fed does this week – if the Fed deems conditions sufficiently calm to raise rates, the RBA will be more inclined to follow, subject of course to the run of local remaining data.

My base case remains ‘one and done’, namely the RBA will raise rates next month but then signal a pause for at least a few months. I also suspect a slowing in local and global economic growth will then become sufficiently evident in the month ahead that the RBA won’t see the need to raise rates again this cycle – but instead may well cut interest rates later this year.

With little key local economic data this week, the main focus will be any insights gleaned from minutes of last month’s RBA meeting released tomorrow. These minutes will be more dated than usual, however, given the meeting took place before the recent upsurge in global financial instability.

Have a great week!

Explore

Markets

2 comments on this

The Regulators action re UBS v CS by favouring equity-holders over lenders is a huge mistake that will have negative consequences. Entities that hold debt will find it less available. Entities needing finance will need to raise capital. All at the wrong time.

Concise and informative.