Cameron Gleeson

6 minutes reading time

A new wave of interest in nuclear power has sparked optimism among uranium producers, with headlines focused on a US “AI-powered” nuclear renaissance. Amazon, Meta and Microsoft are already paying premiums of $15-$25 a megawatt-hour for nuclear energy’s reliable 24×7 output and emission-free attributes to support their data centres.

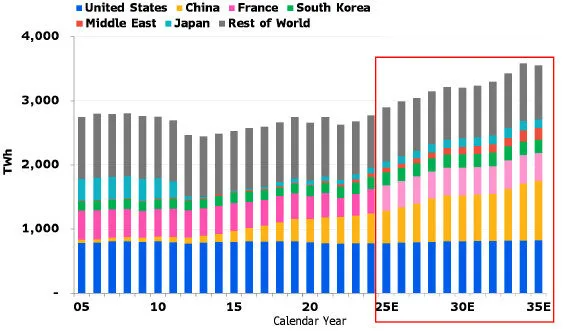

Yet, despite enthusiasm from Washington and Silicon Valley, most of the growth in uranium demand over the next decade will come not from Small Modular Reactors in the US. Instead, it will be driven by existing reactor technology that is being deployed at scale in Asia; led by China, Japan and South Korea.

Bloomberg Intelligence nuclear generation outlook

Source: BloombergNEF. As at September 2025. Bars represent low and high levelised cost of energy (US dollar / megawatt hour). Solar estimates include the cost of 4 hours of battery storage capacity.

US outlook: Ambitious targets, slow realisation

Despite Trump’s aggressive 2050 nuclear capacity target of 400 GW and growing adoption by hyperscalers, it’s unlikely any new major nuclear power plants will be built in the US until at least 2030. Instead incremental additional capacity will come from plant upgrades and limited opportunities to restart idled reactors.

In the US, high construction costs and long build times remain a fundamental obstacle. The two new units at Georgia’s Vogtle plant took twice as long and cost more than double initial estimates — roughly US$31 billion.

To reduce the cost and construction time frames, several US companies are trying to develop Small Modular Reactors (SMRs). Typical nuclear power plants are gigantic and generate 1000 MW or more, SMRs are generally 300 MW or less. Conceptually SMRs allow for standardised designs and modular components that can be build offsite and shipped in, which in theory will lead to lower costs over time.

But SMR leader, NuScale, terminated their Idaho pilot project in 2023 after indicative cost projections more than tripled to $9.3 billion. This setback has not dampened investor interest, SMR start up Oklo’s share price is up more than 1,000% in less than 2 years. Oklo is hoping to deploy its US pilot reactor program by 2027-28. But unproven SMR technology, regulatory complexity and supply-chain limitations may delay broader commercialisation until after 2035. A lot must go right between now and then to justify Oklo’s share price rally.

China: Strategic alignment, cost advantage

By contrast, China already accounts for over 40% of global planned and in-construction nuclear capacity.1 Nuclear’s near zero lifecycle carbon emissions, make it central to Beijing’s decarbonisation strategy and its goal of energy independence.

China approved 10 new reactors in April 2025 alone, the largest single batch since 2011. Its typical construction timeline is just 5.7 years, roughly one-quarter that of the United States, thanks to standardised domestic designs such as the “Hualong One”. China has the domestic industrial base, experienced workforce and state support to build nuclear at scale, and nuclear is now lower cost than other forms of generation in that country.

Source: BloombergNEF. As at June 2024. Bars represent low and high levelised cost of energy (US dollar / megawatt hour). Solar estimates include the cost of 4 hours of battery storage capacity.

With data-centre electricity consumption projected to grow 13% annually through 2035, nuclear energy’s role in powering China’s AI infrastructure will only deepen.

Japan and South Korea: Restarts and exports

After the Fukushima disaster, Japan shutdown most of its nuclear power plants. Today it is aiming to boost nuclear’s share of the energy mix from below 9% of total generation to 20% by 2040. Much of this extra capacity will come from restarting dormant reactors, rather than building new plants. Mitsubishi Heavy Industries and Kansai Electric Power are leading the rebuild of the domestic industry, from maintenance to component supply.

South Korea is a world leader in building nuclear power plants, and has exported its technology globally. Through government partnerships and national champions like Samsung C&T, South Korea has signed US$38 billion in export deals with UAE and Czechia, with a goal of exporting 10 reactors by 2030. South Korea is an attractive partner, it is Western aligned and can build nuclear power plants faster than any other country, with a median construction time of only 4.7 years.

Implications for uranium markets and investors

While US utilities focus on life-extension programs and AI-linked power-purchase deals, Asia’s construction-led expansion will dominate uranium consumption growth through the 2030s. Bloomberg forecasts global uranium supply to rise 23% by 2031, but warns of potential deficits beyond 2032 as Asian reactors ramp up.2

Uranium miners with exposure to Chinese, Japanese and Korean buyers, such as Kazatomprom, Cameco, Paladin Energy and Boss Energy, are well positioned to benefit.

You can tap into the potential growth of these mining companies, as well as other companies in the global uranium industry, by investing in URNM Global Uranium ETF .3 URNM is designed to provide exposure to a portfolio of global companies involved in the mining, exploration, development and production of uranium, or companies that hold physical uranium or uranium royalties.

URNM does not hold utilities companies or companies involved in the construction of nuclear power plants. Building a nuclear power plant is an incredibly complex and costly exercise, which is often reliant on government support. Once that plant is operational however, it will require 60-80 years’ worth of uranium fuel.

In our view, investing in a global diversified basket of the suppliers of that fuel, the uranium miners, is the most compelling way to play the so-called nuclear renaissance.

It’s worth noting that, while there are uranium mining companies listed on the ASX, trying to pick individual stocks in this sector can come with added volatility. Most of these companies sit outside the S&P/ASX 100 Index and some are pre-production which introduces project execution risk to a portfolio. Rather, investors should take a global view when considering emerging sectors, like uranium, diversifying their exposure across individual names and even countries, particularly where operations are located in countries where sovereign risk is elevated. Furthermore investors might want to consider an allocation to the global uranium sector as a satellite allocation, rather a core exposure, within a highly diversified basket of Australian and International equities, bonds and commodities.

Sources:

1. World Nuclear Association, Nuclear Power in China, 25 October 2025 ↑

2. Bloomberg Intelligence, Nuclear Power 2026 Outlook, 29 September 2025. ↑

3. Note, that while Kazatomprom, Cameco, Paladin Energy and Boss Energy were held in URNM as at 25 October 2025, no assurance is given that these companies will remain in the portfolio or will be a profitable investment. ↑