RBA reprieve

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets

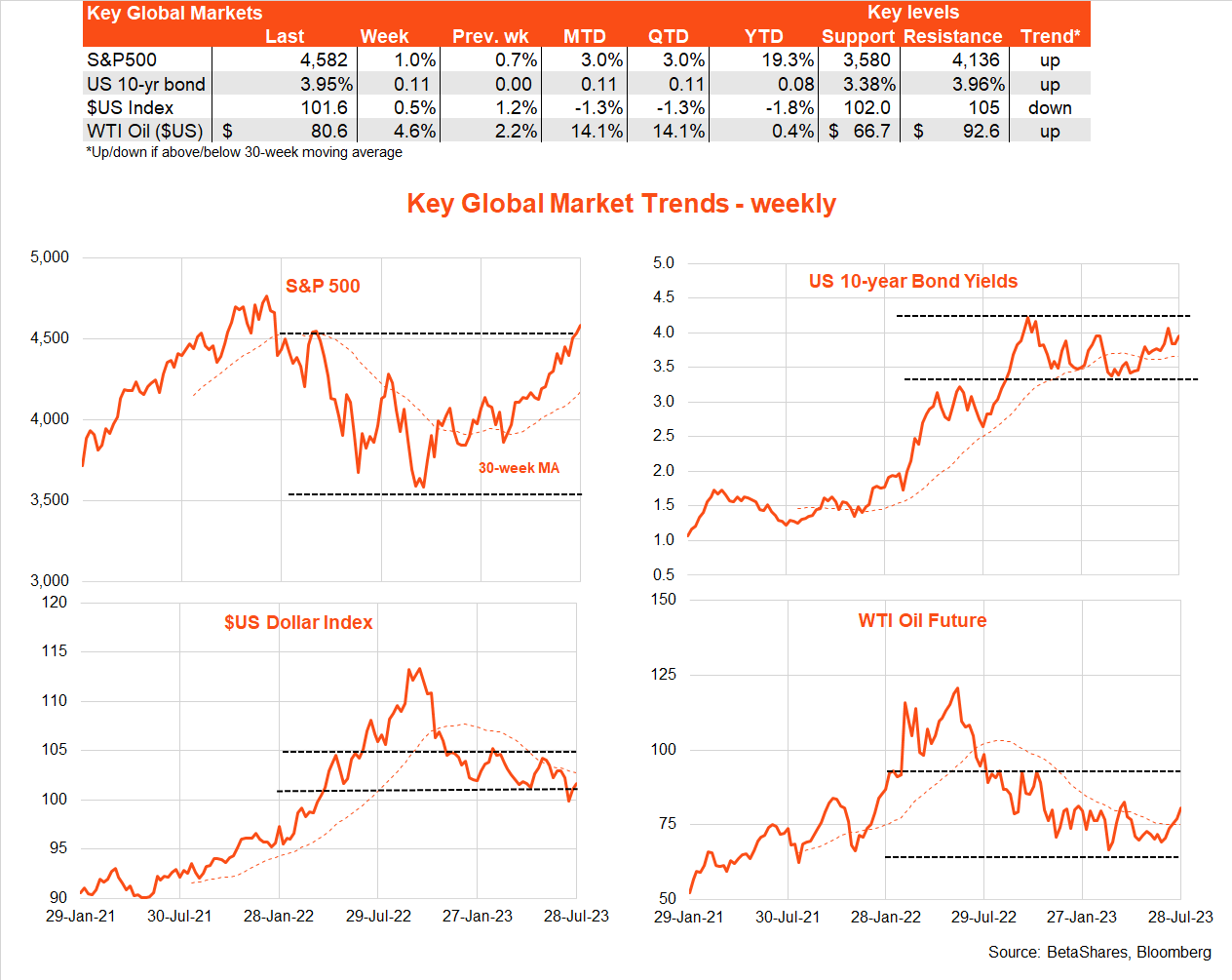

The ‘melt-up’ in US stocks continued last week, with the S&P 500 adding another 1.0%. There were various reasons for investors to remain upbeat: the Fed hiked rates but displayed a more neutral outlook, the Q2 US earnings reporting season remained encouraging (thanks to Meta and Alphabet), while US wage and price inflation surprised on the downside even as GDP growth surprised on the upside.

In short, what once seemed a far-fetched fairy tale story of a US soft landing or “immaculate disinflation” appears to be becoming all the more plausible by the day. Even the Fed is no longer officially forecasting a recession.

Of course, one sticking point remains – uncomfortably high US wage growth against the backdrop of a still tight US labour market. But service sector inflation is nonetheless easing. And with the degree of excess labour demand easing (in part due to increasing labour supply) and declining inflation, there’s a chance wage inflation could continue to decline back to pre-COVID levels without much loss in current employment.

Can we dare to dream?

In other key global news, the ECB hiked rates as expected but, like the Fed, adopted a more neutral outlook over whether rates would need to be lifted again. The Bank of Japan ruffled a few feathers, at least momentarily, by signalling it would allow 10-year bond yields to drift somewhat higher than 0.5%. It remains to be seen exactly how hawkish the BOJ will become but I doubt it will do much to relax its still ultra-easy monetary policy and disrupt global markets – lest it allow the Yen to unduly strengthen.

The key highlight this week will be the July US payrolls report on Friday, which is expected to reveal another solid employment gain of 184,000 with the unemployment rate holding steady at 3.6%. As important, however, will be the degree to which annual growth in average hourly earnings continues to slow, having reached 4.4% in June.

An update on the health, or otherwise, of the Chinese economy will come with key manufacturing and service sector indices this morning. Back in the US, Apple and Amazon are reporting earnings on Thursday.

As evident in the chart set below, hopes of a soft landing are leading to some broadening in the equity recovery to more value-orientated exposures in recent such as the US S&P 500 equal-weight index, with an offsetting pullback in recent Japanese outperformance. Australia’s relative performance continues to languish.

Australian market

The lower-than-expected Q2 CPI helped give local stocks a lift last week as it reduced the risks of the RBA hiking interest rates this week. All up, the broad disinflationary trend becoming evident globally continues to flow through into Australia – albeit with a lag. At the same time, the 0.8% slump back in June retail sales (after a 0.8% gain in May boosted by early mid-year discounting) confirmed that although Aussie shoppers love a bargain, an underlying slowdown in consumer spending is still underway.

Of course, the highlight this week will be Tuesday’s RBA meeting. Although, like many, I’ve found it difficult to pick the RBA’s zigs and zags in recent months, I reckon the good CPI and soft retail sales last week more than offset the earlier stronger labour market report – and give the RBA breathing space to leave rates on hold for at least another month. The RBA should also be heartened by further signs of easing global service sector inflation – given it pointed to stickiness in this area earlier this year to justify rate hikes.

We’ll learn more about RBA thinking in its August Statement on Monetary Policy on Friday. With long-term inflation expectations still well anchored, what seems critical – especially about this week’s rates decision – is whether the RBA can credibly retain its forecast of inflation falling back to within the 2-3% target band by mid-2025. If it can, and I think it will, it could justify leaving rates on hold this week, allowing the economy the chance to continue to warily tread down the “narrow path” of getting inflation down without a recession.

That said, the RBA won’t be overly joyed to see another likely gain in national house prices in CoreLogic data also released this week, along with a likely further lift in home lending. Against this, Thursday’s more detailed June retail sales report will likely confirm sales volumes fell further in the June quarter.

Have a great week!

| Top events of the past week | Comment |

| Good US inflation and activity data | Annual growth in both the headline and core private consumption deflator eased a little more than expected in June. The Q2 employment cost index was also a touch softer than expected. At the same time, Q2 US GDP surprised on the upside, confirming the economy retains healthy underlying momentum. |

| Fed rate hike | The Fed hiked rates as widely expected and remained non-committal over whether rates would need to rise again. |

| Good Australian CPI | The Q2 CPI was lower than expected, easing fears the RBA will hike rates this week. Annual trimmed mean inflation eased to 5.9%. |

| Key events to watch this week | Comment |

| US payrolls | Another solid employment result is expected on Friday (US time), with a focus on the degree of any further easing in wage inflation. |

| RBA meeting and Statement on Monetary Policy | RBA will likely leave rates on hold on Tuesday with updated economic forecasts provided on Friday. |

| Chinese manufacturing and service sector data | Key indices on Monday are likely to show that Chinese economic recovery remains relatively muted. |

Explore

Bassanese Bites