Rates relief

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

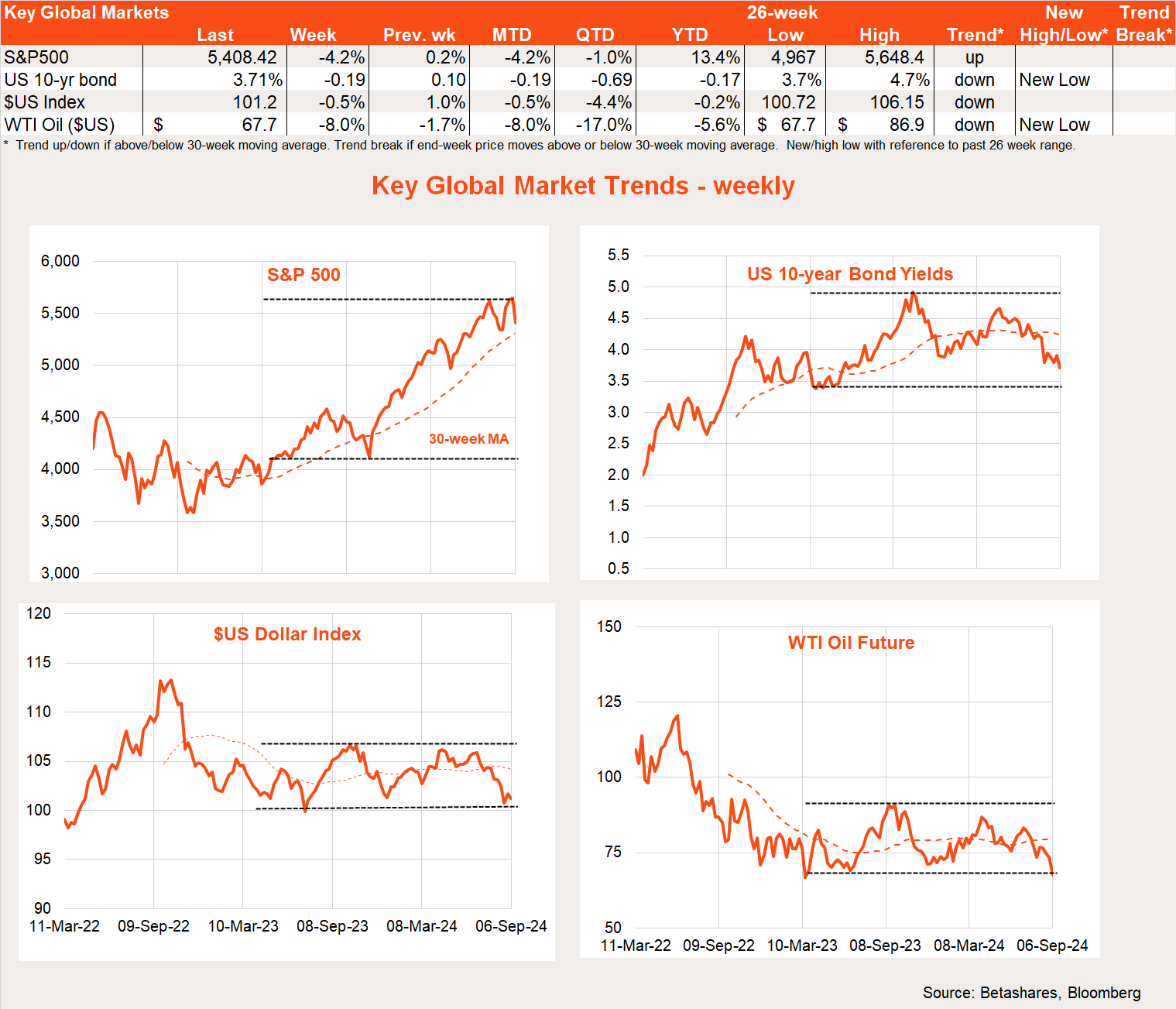

Global markets

Global equities declined sharply last week, reflecting further weaker than expected US economic data and anti-trust concerns around tech darling Nvidia.

As the saying goes, the faster they rise, the harder they fall – and Nvidia is no exception. The sharp sell-off in this AI glamour stock over recent months has reflected a combination of factors: high valuations, an apparent peaking in sales growth and, most recently, reports that the US Department of Justice (DOJ) is looking into anti-competitive practices, such as limiting the ability of customers to use alternative chips. Also noteworthy in this regard are reports that the use of AI tools such as ChatGPT is waning – has the novelty already worn off?

The stock dropped a lazy 13% last week following new reports of the DOJ investigation – taking its decline since its mid-June peak to 24%. That said, the stock is still up 4% from its early-August low, though there’s every chance that low could be taken out in coming weeks.

Of course, the falling back to earth of one high-flying stock need not cause an overall market meltdown, unless it becomes reflective of a broader re-appraisal of the whole AI frenzy that, along with the US soft landing scenario, has helped propel equity markets higher since late 2022.

The other factor hurting stocks last week was further signs of softness in the US economy, with weaker then expected reports for manufacturing, job openings and employment growth. That said, the ISM services sector survey remained solid and weekly jobless claims also held at a reassuringly low level. All up, to my mind US economic data remains sufficiently mixed that the Fed is still likely to only cut rates by 0.25% at next week’s meeting.

Note the Bank of Canada cut rates last week as widely expected, though only by a further 0.25%.

Global week ahead

A highlight this week will be the debate between US Presidential contenders Harris and Trump. With polls still apparently tight, the debate could be pivotal in determining November’s outcome and the course of US economic policy. At this stage, however, it’s not clear which of the contenders the market prefers – as Harris seems to offer steadier economic policy and no new tariffs, while Trump offers less regulation and lower taxes.

The key piece of economic data will be the August consumer price index report, with another benign 0.2% gain expected. Markets these days are less concerned over upside inflation risks and more concerned with downside economic risks.

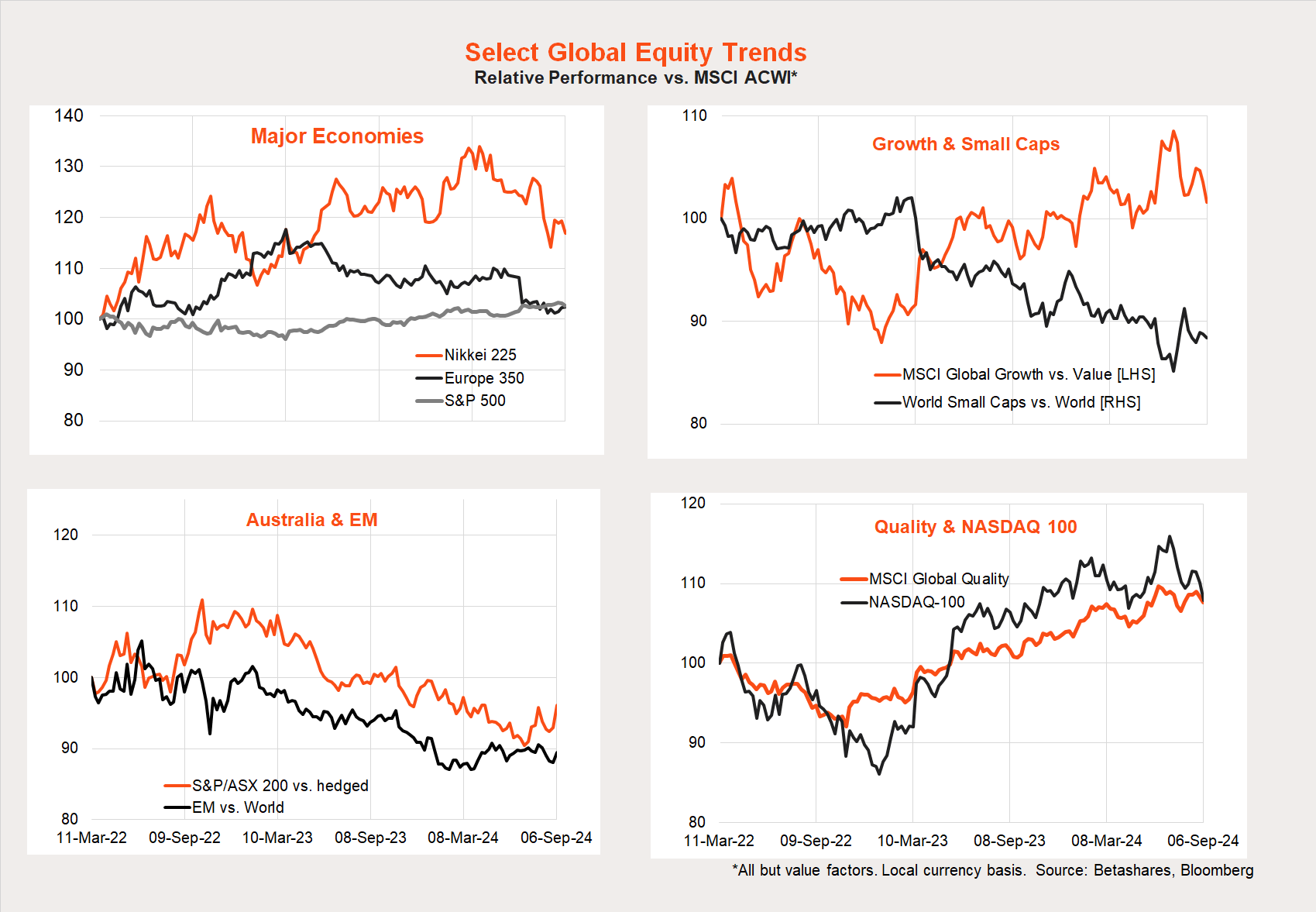

Market trends

The sell-off in stocks last week again hit the large-cap US technology sector – especially reflecting the pressures on Nvidia. As a result, the ‘great rotation’ towards cheaper parts of the global market remains directional (i.e. tends mainly to happen in market sell-offs) at this stage.

All up, we’ll need the dust to settle from recent market volatility to discern whether the much-debated broadening in the global equity rally will gather steam. Can cheaper value stocks outperform as equity markets continue to trend up? I suspect that they can, but the evidence to date remains patchy.

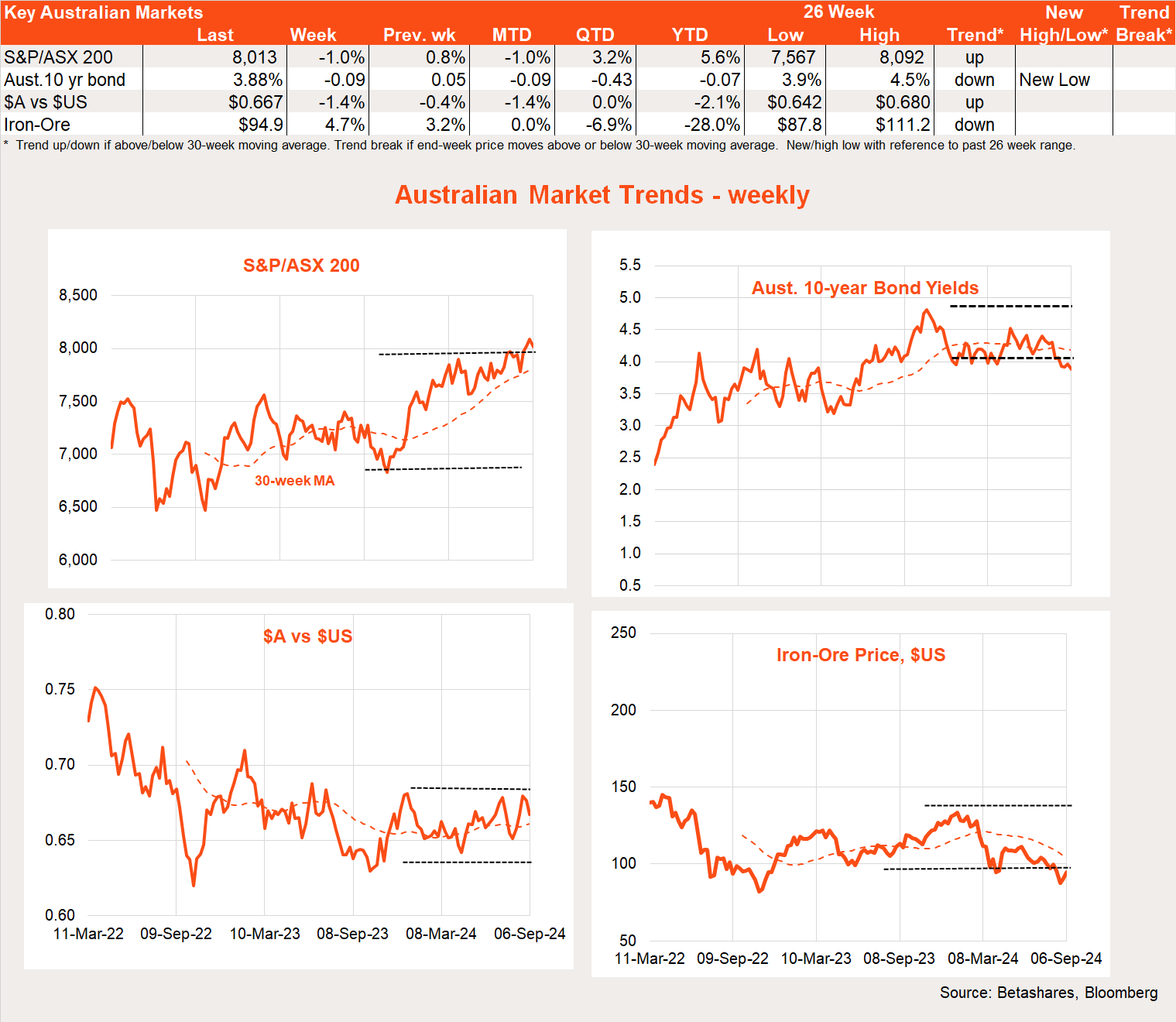

Australian market

Local stocks slipped only 1% last week, but will weaken further this morning as they catch-up with Wall Street’s sell-off on Friday.

Two major highlights last week were the soft Q2 GDP report and RBA Governor Bullock’s continued defiant stand against the idea of rate cuts any time soon. With inflation still around 4% and part of the weakness in the economy reflecting capacity constraints (in the RBA’s mind at least), the Governor’s view should really be no surprise.

What is surprising, however, is the Federal Government’s decision to start attacking the RBA’s steadfastness. Even if the RBA was thinking about cutting rates, Government criticism would make it all the more difficult – as the RBA would not want to be seen as being politically compromised.

In an otherwise data-light week, we’ll learn more on the health of the economy this week with surveys of consumer and business confidence tomorrow.

Have a great week!

Explore

Bassanese Bites

3 comments on this

What conclusion does one make with US 2 year and 10 year bond rates being almost the same?

What a mess our world economic position is.

Each week I read what news David delivers while reading daily economic views based on evidence from those analysts in the USA.

For months it has been widely reported that all stocks will plumet in their value.

Trusting our Economist is now not relevant as they appear to be just news reader like those on Channel 7.

Mum’s and Dad’s have been struggling, our young families are bearing the brunt of economic failures by those in charge. The Blame game is always at play, but daily people struggle to pay their bills and have ongoing employment. Geopolitical landscape is a mind field. Volatility is at four corners of the world.

A complete failure of the share market is just a matter of time.

‘Harris seems to offer steadier economic policy’. Anyone who saw her comments on inflation which went viral can see she is clueless. Her handlers are not. Communism is a steady economic policy, with the predictable outcome of poverty for the majority. I think the USA has no way out, and will soon collapse under its debt loads, but prefer a president with values which will allow the country to rebuild. In addition, I prefer a president who will make efforts to end wars and negotiate rather than start them (a business person say) as they are very expensive on so many levels.